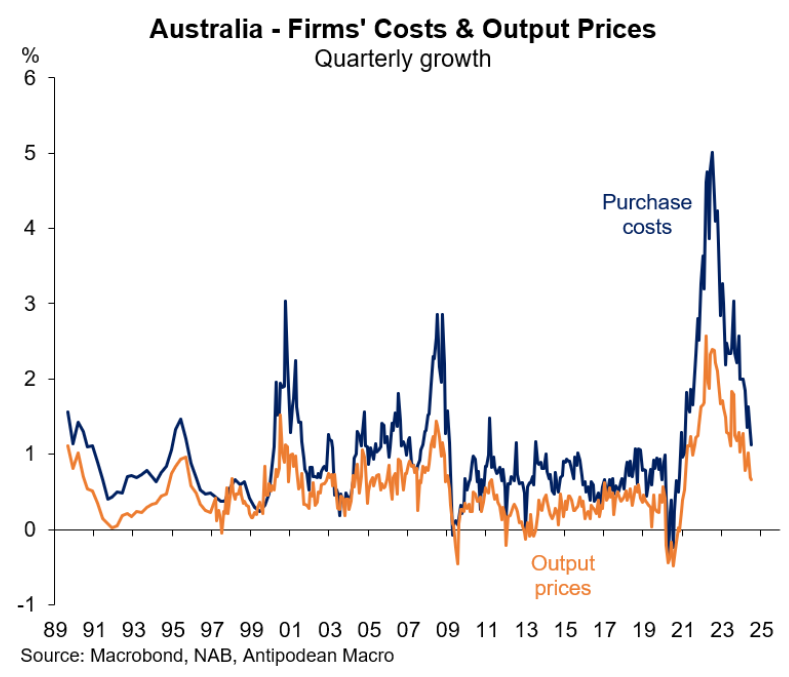

The Reserve Bank of Australia (RBA) should be encouraged by Tuesday’s NAB Business Survey, which reported lower cost pressures.

As illustrated below by Justin Fabo at Antipodean Macro, “Aussie firms reported lower inflation in both output prices and purchase costs in July and the trends have been firmly down”:

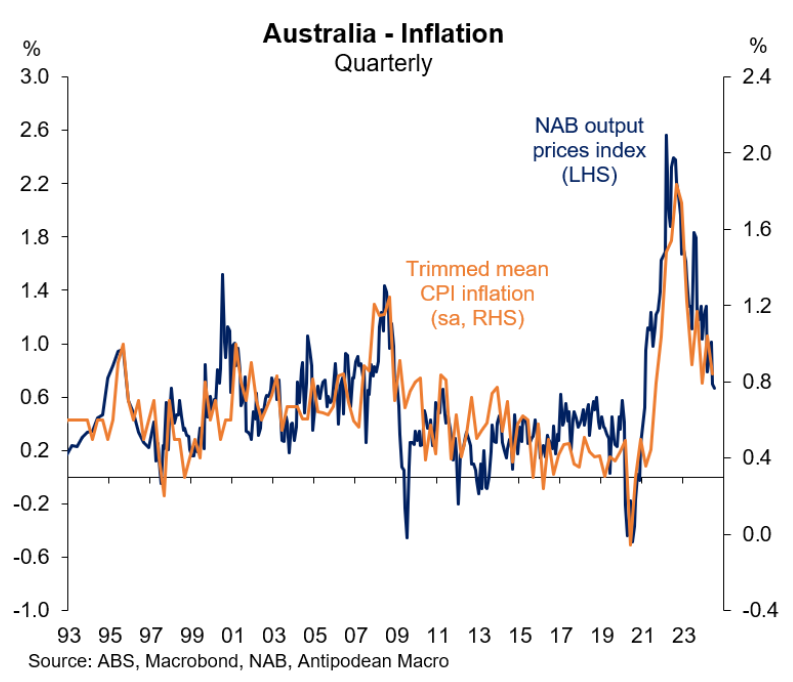

Fabo also noted that “the RBA will be broadly happy with signs of further easing in output price inflation”:

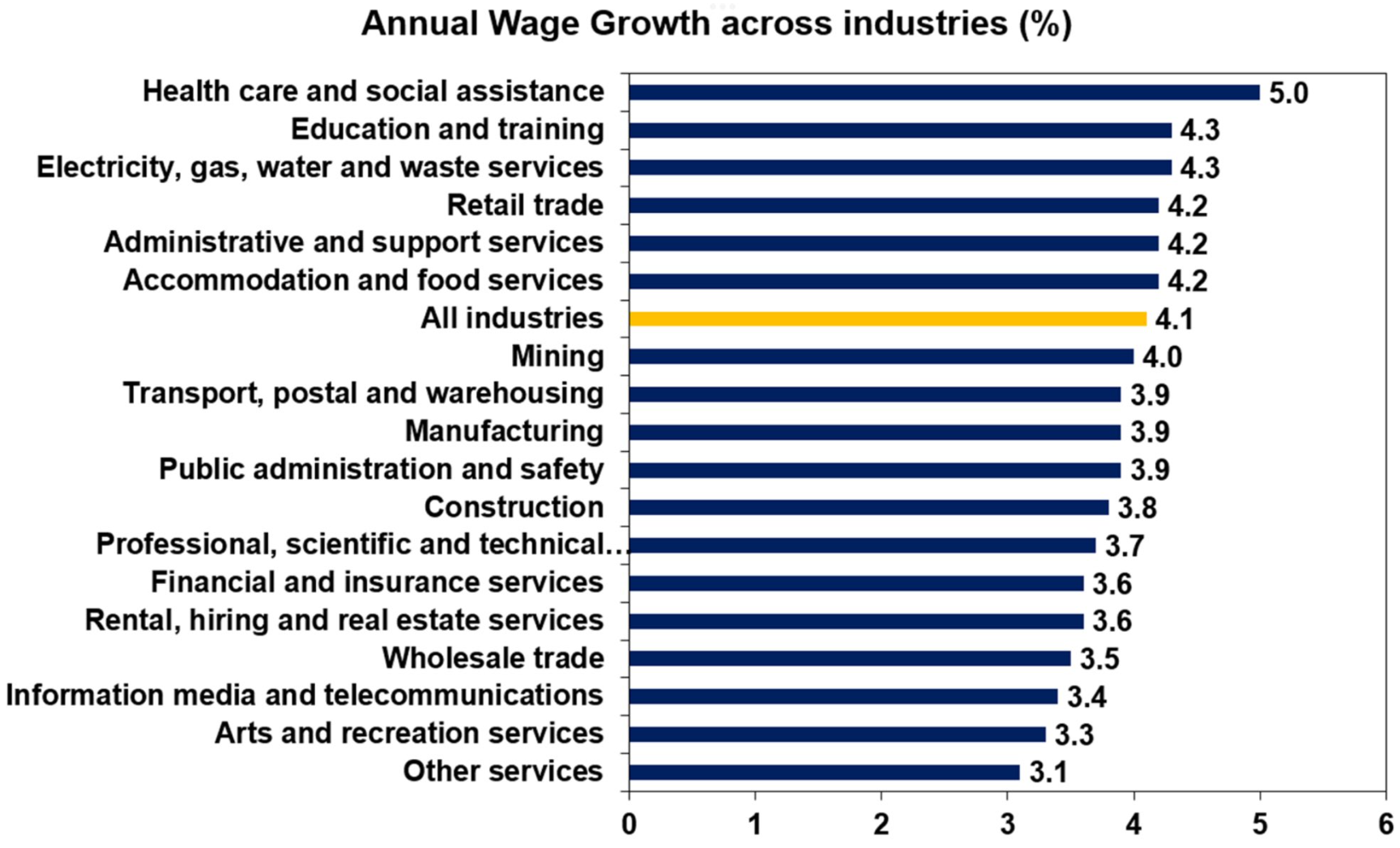

The RBA should also be relieved by Tuesday’s wage growth data from the Australian Bureau of Statistics (ABS).

The wage price index rose by 0.8% in the June quarter, weaker than market consensus of 0.9%.

Wage inflation has moderated in the first half of the year, with the six-month annualised pace easing from 4.7% in December to 3.4% in June.

Importantly, the easing of wage growth has been driven by the private sector.

As noted by Westpac, “private sector wages rose 0.7% in June 2024, representing an ongoing moderation in quarterly gains from September 2023 (1.4%), December 2023 (1.0%) and March 2024 (0.9%)”.

By contrast, NDIS-related spending continues to drive up wages across the healthcare & social assistance industry:

Source: AMP

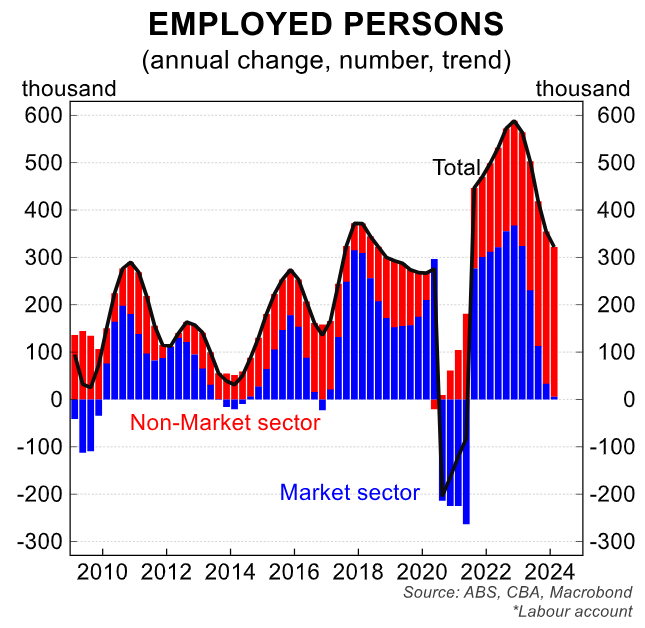

The same applies in relation to employment, with nearly all of Australia’s jobs growth coming from government-aligned industries, most notably healthcare & social assistance: