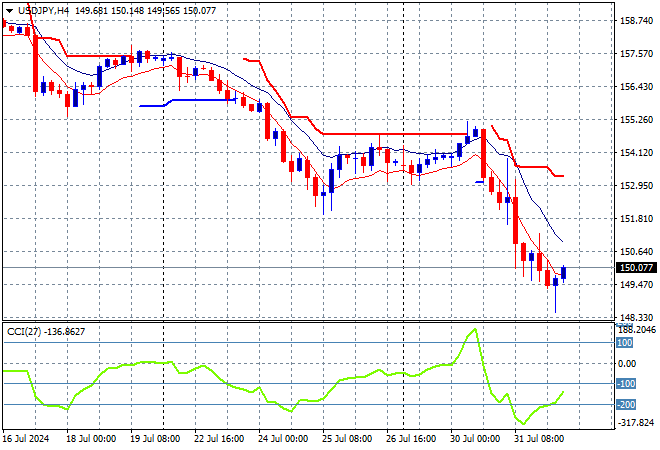

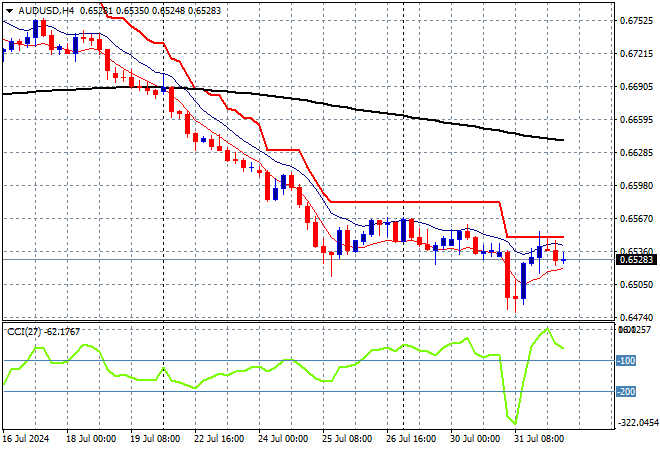

Asian share markets are struggling to push through the volatility of the last 24 hours with the latest Fed meeting overnight following the BOJ rate hike amid macro events in the Middle East and elsewhere stirring up the risk market matrix. The USD is mixed against the majors as Yen appreciates appreciably (more than 500 pips in the last couple of days) while Euro is starting to weaken. The Australian dollar doesn’t look too good either with recent inflation figures pointing to possibility of rate cuts sooner than expected as it barely maintains above the 65 cent level.

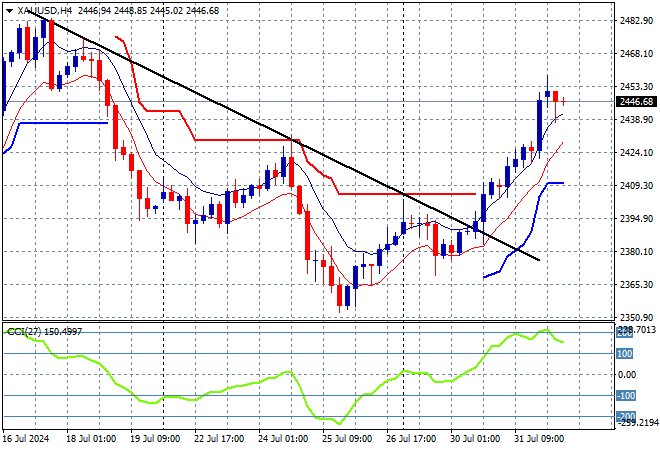

Oil prices are climbing higher on the growing Middle East conflicts with Brent crude above the $81USD per barrel level while gold has paused its bounceback above the $2400USD per ounce level:

Mainland Chinese share markets are still struggling with the Shanghai Composite losing a little more than 0.2% to remain under 3000 points while the Hang Seng Index is dead flat at 17338 points. Meanwhile Japanese stock markets are reacting poorly to the big moves in Yen with the Nikkei 225 down nearly 2.5% to close at 38126 points as the USDJPY pair extended further below the 149 handle before just getting back to the 150 level in what has been a wild ride so far this week:

Australian stocks were the best in the region, relatively speaking with the ASX200 closing just 0.2% higher to 8114 points while the Australian dollar slid slightly from its overnight rebound and is just off the floor at the 65 cent level:

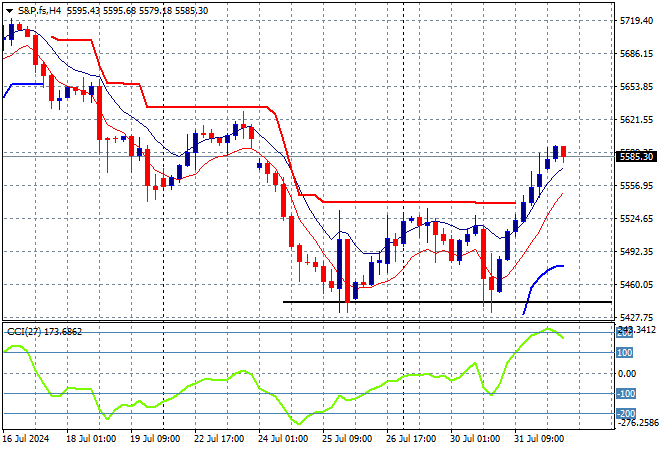

S&P and Eurostoxx futures are up slightly as we head into the London session with the S&P500 four hourly chart showing how the bottom at the 5400 point level looks quite firm after a few solid sessions but still needs to clear resistance around the 5600 point level:

The economic calendar tonight includes the BOE interest rate meeting, followed by US weekly initial jobless claims, then the very closely watched ISM manufacturing PMI print.