Below is CBA Senior Economist Belinda Allen’s report on the July labour market survey from the ABS:

Key Points:

- Employment growth was strong in July, rising by 58.2k.

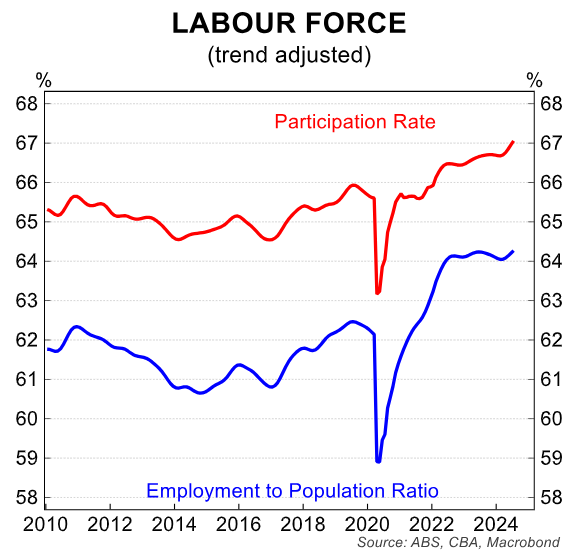

- The unemployment rate increased from 4.1% to 4.2% as the participation rate reached a record high of 67.1%.

- We believe the unemployment rate is the key metric to watch for the monetary policy outlook.

Strong gain in employment but unemployment rate lifts to 4.2%:

The July labour market data print had something for everyone. Employment rose by a large 58.2k, stronger than both consensus and our call of +20k. Full time employment was the key driver, up by 60.5k compared to a fall in part-time employment of -2.3k.

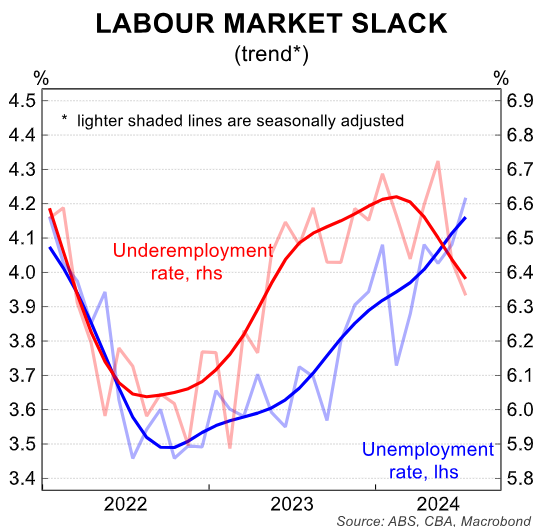

A record high participation rate of 67.1% (up from 66.9% in June) saw the unemployment rate lift to 4.2%, up from 4.1% in June. The trend unemployment rate also lifted to 4.2%.

We believe the unemployment rate is the key metric to monitor slack in the labour market and helps inform the monetary policy outlook.

While employment growth was strong, the number of unemployed people rose by 23.9k. The total number of unemployed people now sits at 637k and is the highest since October 2021.

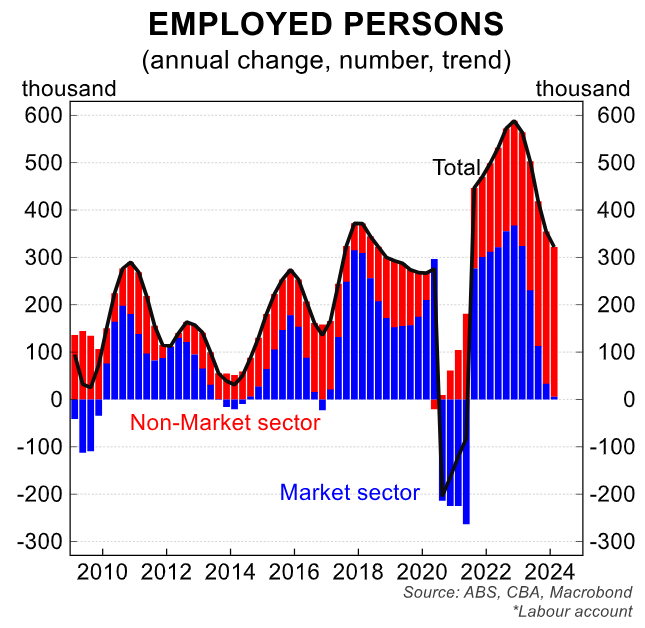

The Australian labour market is a puzzle. Employment growth for the year to July was 3.2%, compared to an economy growing closer to 1%, the slowest rate in 30 years outside the pandemic.

Part of this puzzle can be solved by strength in employment in non-market sectors.

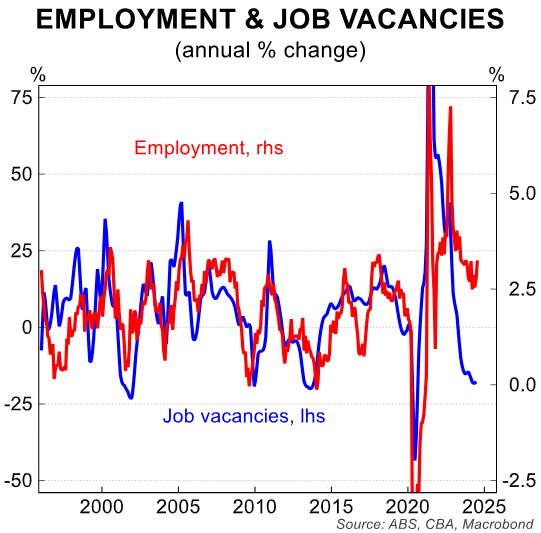

Slower growth in hours worked versus employment can also explain some of the puzzle. Employment growth over the past year has risen by 3.2% compared to hours worked at just 0.9%.

Normally we would see the underemployment rate lift as hours worked slows. But this dynamic is missing this time around. Workers could be content working less hours.

The underemployment rate sits at 6.3% in July, compared to its trough of 5.9% in February 2023. A much smaller increase when compared to the unemployment rate, the trough was 3.5%, compared to 4.2% in July.

A below trend economy appears to be manifesting itself in the labour market in different ways.

First, hours worked is slowing faster than employment growth.

Second, job vacancies are falling, but this is not translating through to slower employment. Job ads are likely getting pulled instead.

A rising participation rate is another interesting dynamic. It rose to a record high 67.1% in July, up from 66.9% in June and the 12-month average of 66.7%. The participation rate for both men and women has lifted.

Ample employment opportunities and cost of living pressures are pulling workers into the labour force.

We still expect the labour market to loosen from here. But admit this is taking longer to occur than we had expected, especially on the employment front.

We still believe the unemployment rate is the key metric to watch for the monetary policy outlook.

A lift in the unemployment rate to 4.2% suggests slack is building. Together with the wage impulse slowing, this should provide some comfort.

The RBA would be concerned about the unemployment rate lifting too quickly. Offshore evidence has indicated this can happen quickly.

We still maintain our central case scenario for a November start date for the first interest rate cut from the RBA. But we are growing uneasy, given the shortening runway to achieve the data configuration required for the RBA to feel comfortable cutting the cash rate, especially after today’s employment print.

From here, consumer spending data, the Q3 24 CPI print and upcoming labour market data all would need to move in the right direction to achieve our central case scenario.

The risk continues to build for a 2025 start date to the easing cycle.