Inflation data takes rate hikes off table

Following Thursday’s Q2 CPI inflation and retail sales data from the Australian Bureau of Statistics (ABS), I sat down with Gunnamatta to analyse the numbers and explain what they likely mean for interest rates:

The bottom line is that the 0.8% trimmed mean result for Q2 undershot expectations of a 1.0% rise and was in line with the RBA’s May Statement of Monetary Policy forecasts.

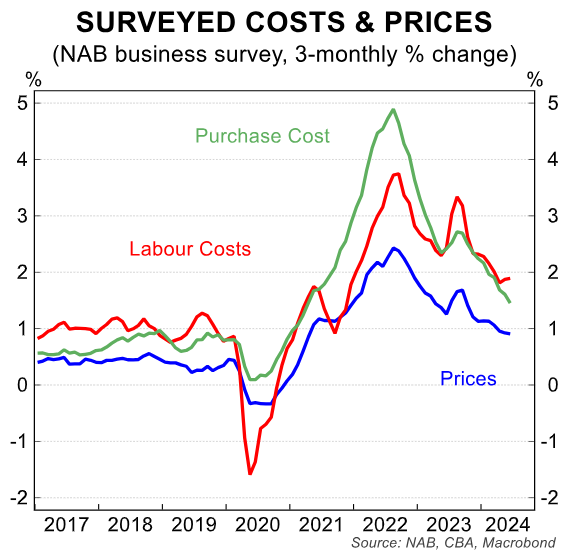

The reality is that inflationary pressures are easing across the economy, albeit more gradually than the RBA would like.

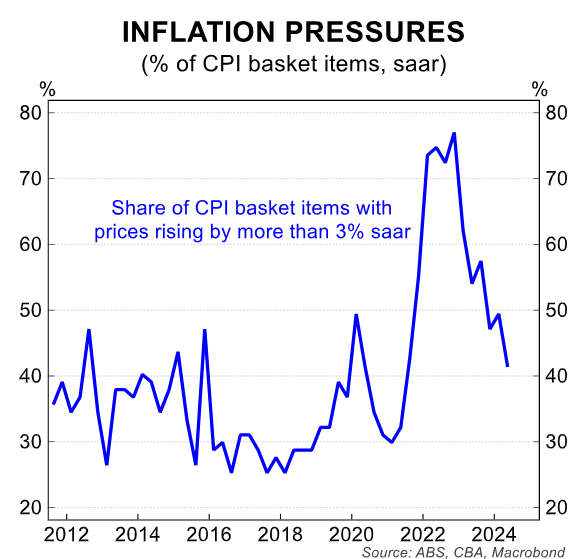

The breadth of price rises above 3% has also fallen to normal pre-pandemic levels:

As noted by CBA, “only 41% of the 87 expenditure classes that make up the CPI basket recording seasonally adjusted annualised price growth of more than 3%”.

“That’s the lowest share in two years and well down from the near 50% in Q1 24. This suggests that while the headline CPI remained elevated at 1.0%/qtr, that is being driven by a narrower share of the basket”.

As a result, the RBA is very likely to keep rates on hold at its monetary policy meeting on Tuesday.

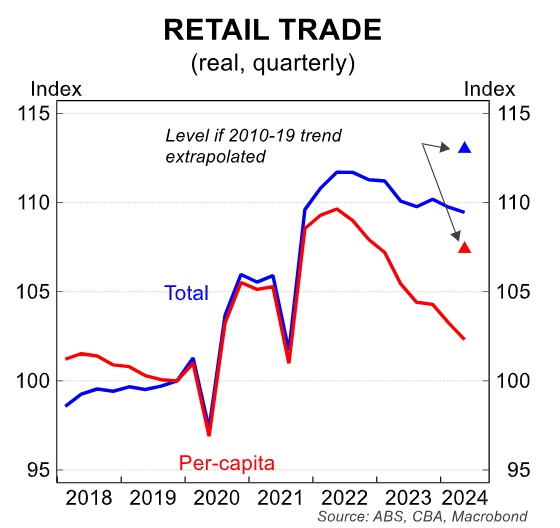

The RBA would also have taken note of Australia’s deplorable retail sales figures, which showed that aggregate retail sales volumes fell by 0.3% over the quarter to be down 0.6% year-on-year.

The annual change has now been negative for the last five quarters. Outside of the pandemic, in only four other quarters has the annual growth been negative, dating back to the 1980s.

Even worse, retail volumes on a per capita basis (-0.9%) declined for an eighth consecutive quarter, down 3.0% compared to the same time last year.

Based on the above data, the RBA will be reluctant to raise rates further.

That said, there are still inflation pressure points in the economy.

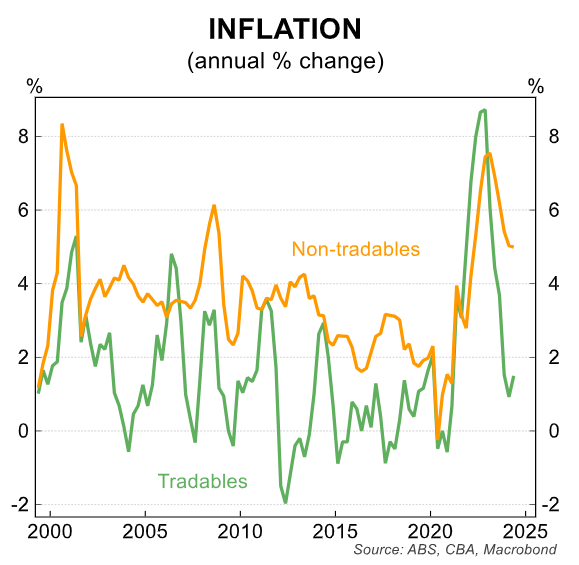

Domestic inflation is still alarmingly high, with 1.5% tradeable inflation in Q2 offsetting the 5.0% non-tradeable inflation rate.

Therefore, the RBA will be watching the incoming data flow closely with regards to future interest rate decisions.