DXY was smashed Friday night:

That prevented a rout in the AUD:

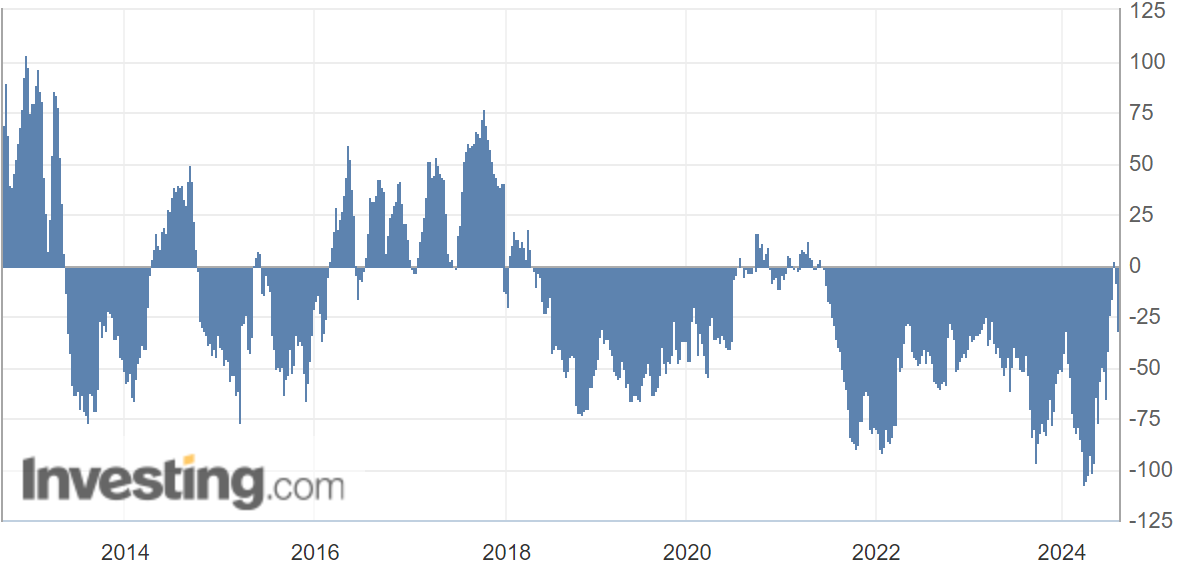

Specs have moved short AUD again but there is plenty of room to fall:

North Asia is wild:

Oil is at breaking point:

Dirt is in free fall:

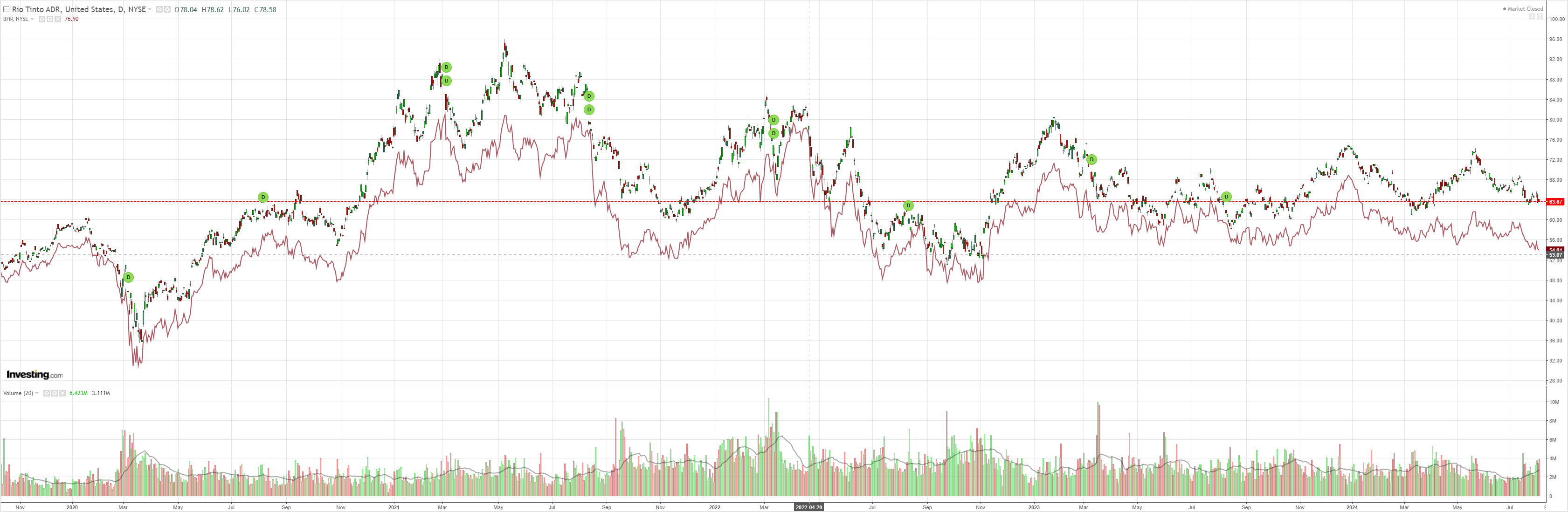

Miners are deluded:

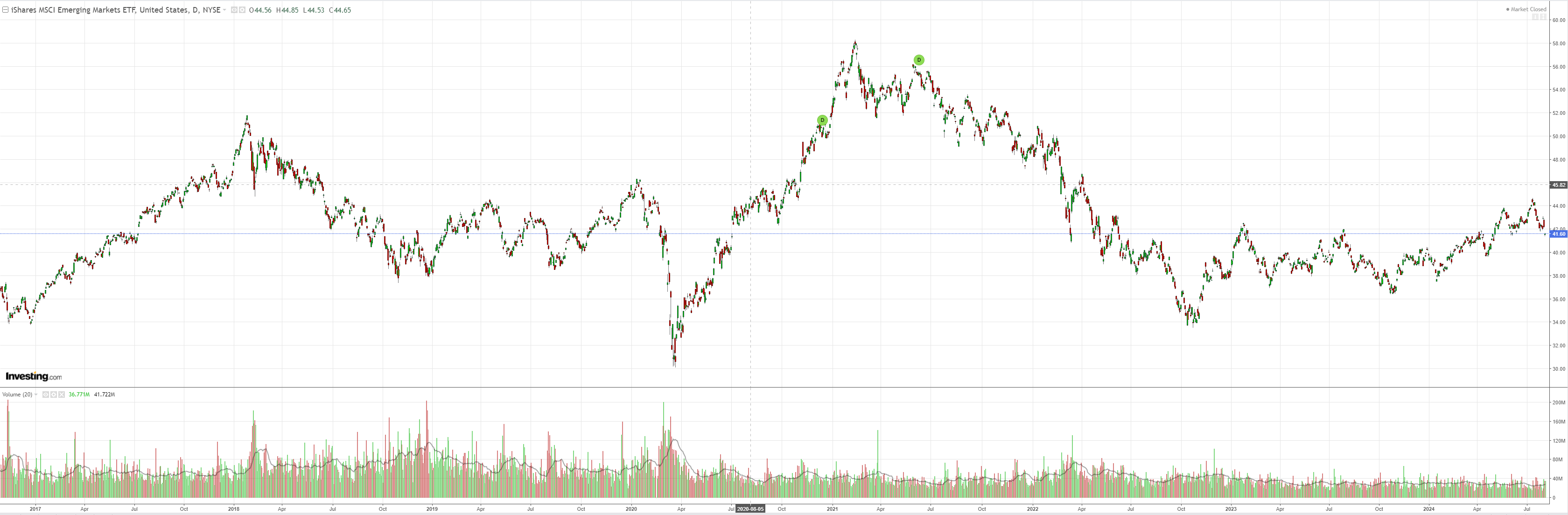

EM is breaking down:

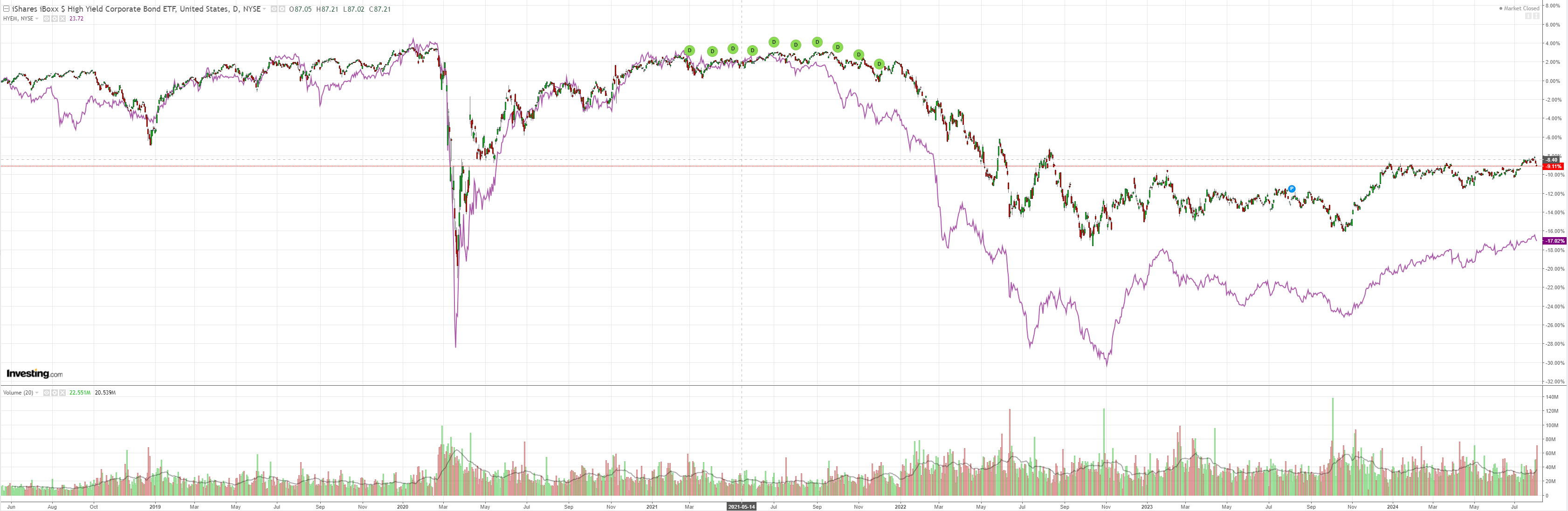

Junk spreads finally joined the pessimism:

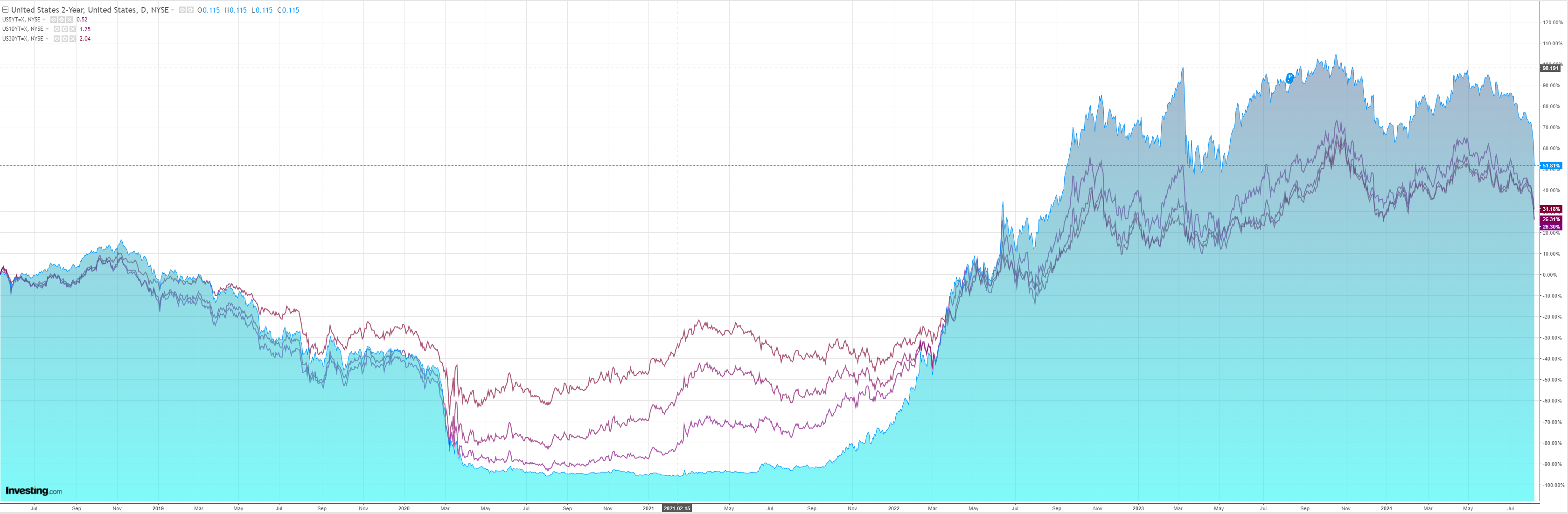

Even as US yields capitulate:

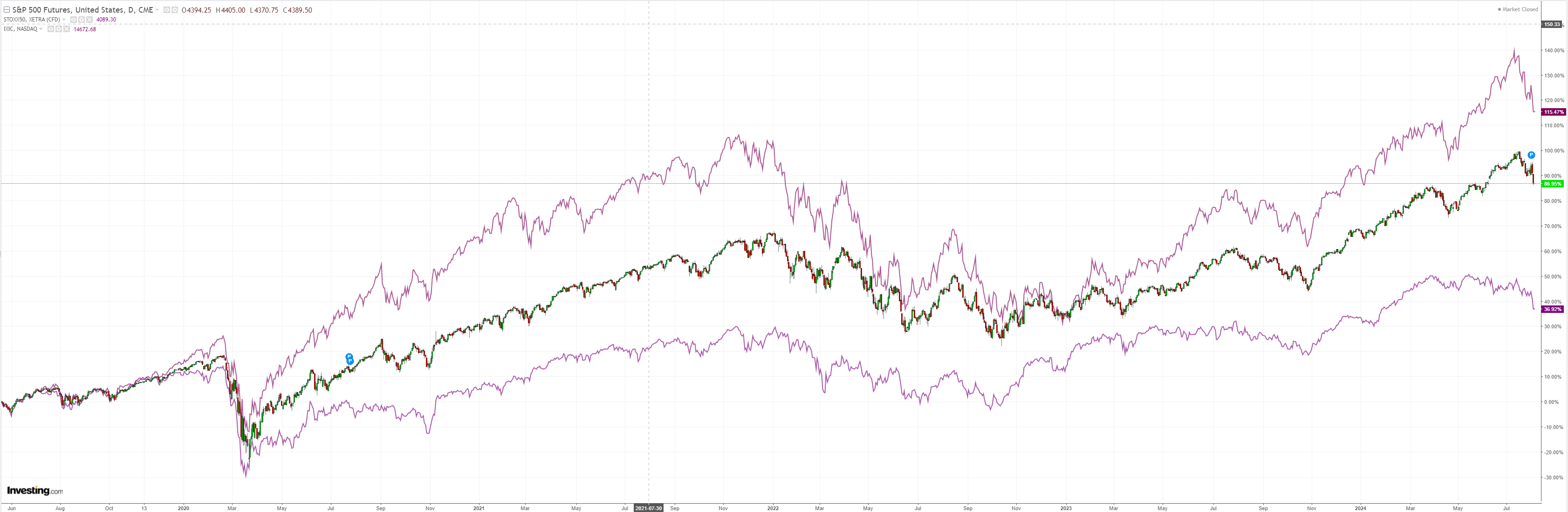

Stocks broke:

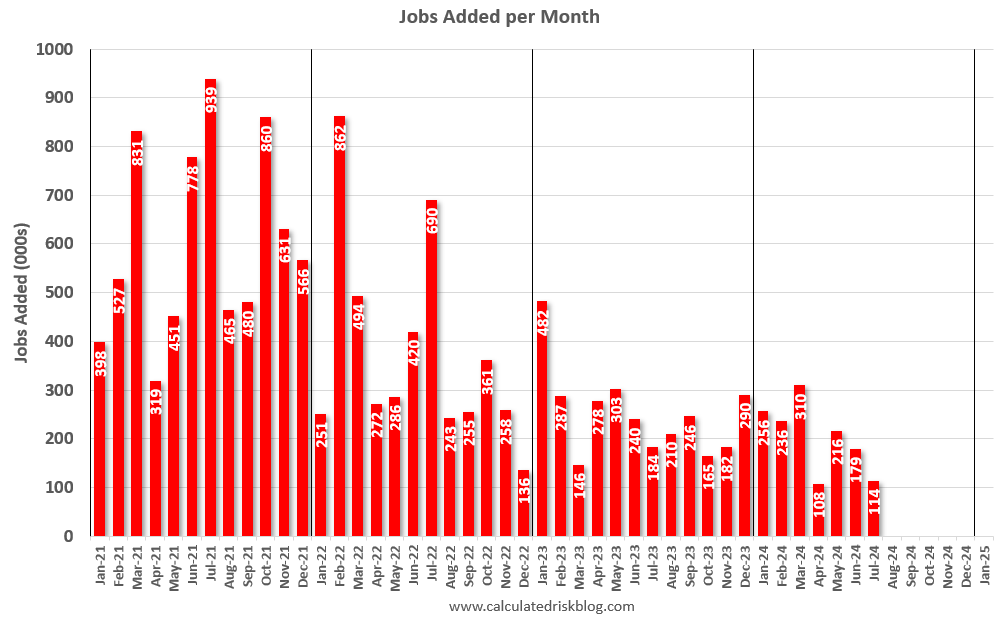

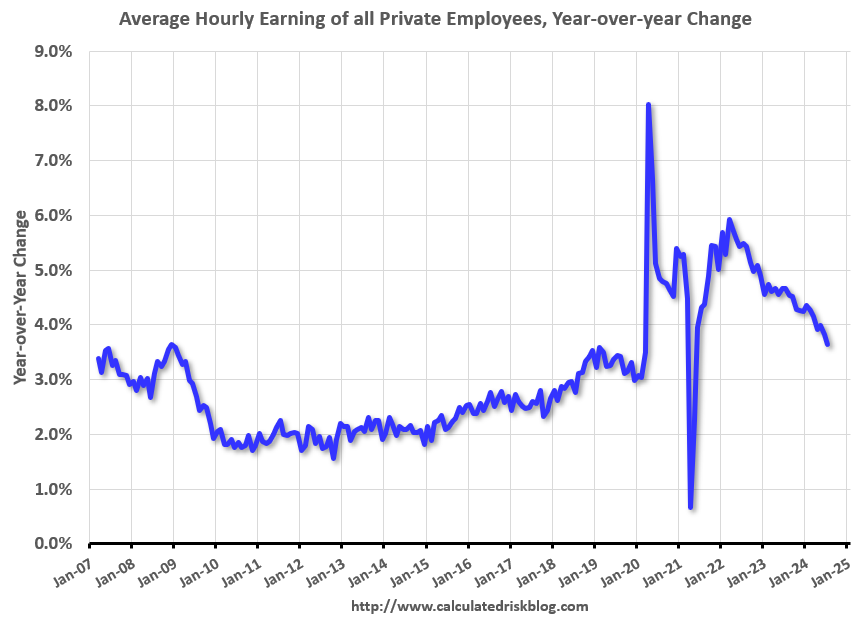

US jobs softened materially:

The unemployment rate rose to 4.3 percent in July, and nonfarm payroll employment edged up by 114,000, the U.S. Bureau of Labor Statistics reported today. Employment continued to trend up in health care, in construction, and in transportation and warehousing, while information lost jobs.

…The change in total nonfarm payroll employment for May was revised down by 2,000, from +218,000 to +216,000, and the change for June was revised down by 27,000, from +206,000 to +179,000. With these revisions, employment in May and June combined is 29,000 lower than previously reported.

The Fed has overtightened, as it always does by definition, and the US jobs market is breaking down. It is not yet dire and I still think the soft landing is the base case.

But it is going to be softer, not softish.

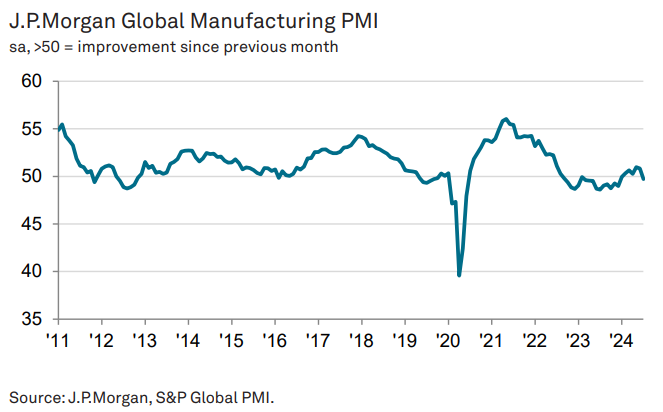

Especially for everywhere outside of the US. Europe and China are sailing hand in hand into worse, leading the global PMI down:

The global manufacturing sector experienced a growth setback at the start of the second half of 2024, with July seeing output expand at the weakest rate in the current seven-month sequence of increases.

The slowdown reflected weaker expansions in the US and China, an ongoing downturn in the euro area and a fall back into contraction in Japan.

Declining new order intakes were also a major factor underlying the weaker expansion, as new business fell for the first time since January.

The AUD held up Friday night but I can’t see it holding as markets reprice for a slower growth world, recession or not.