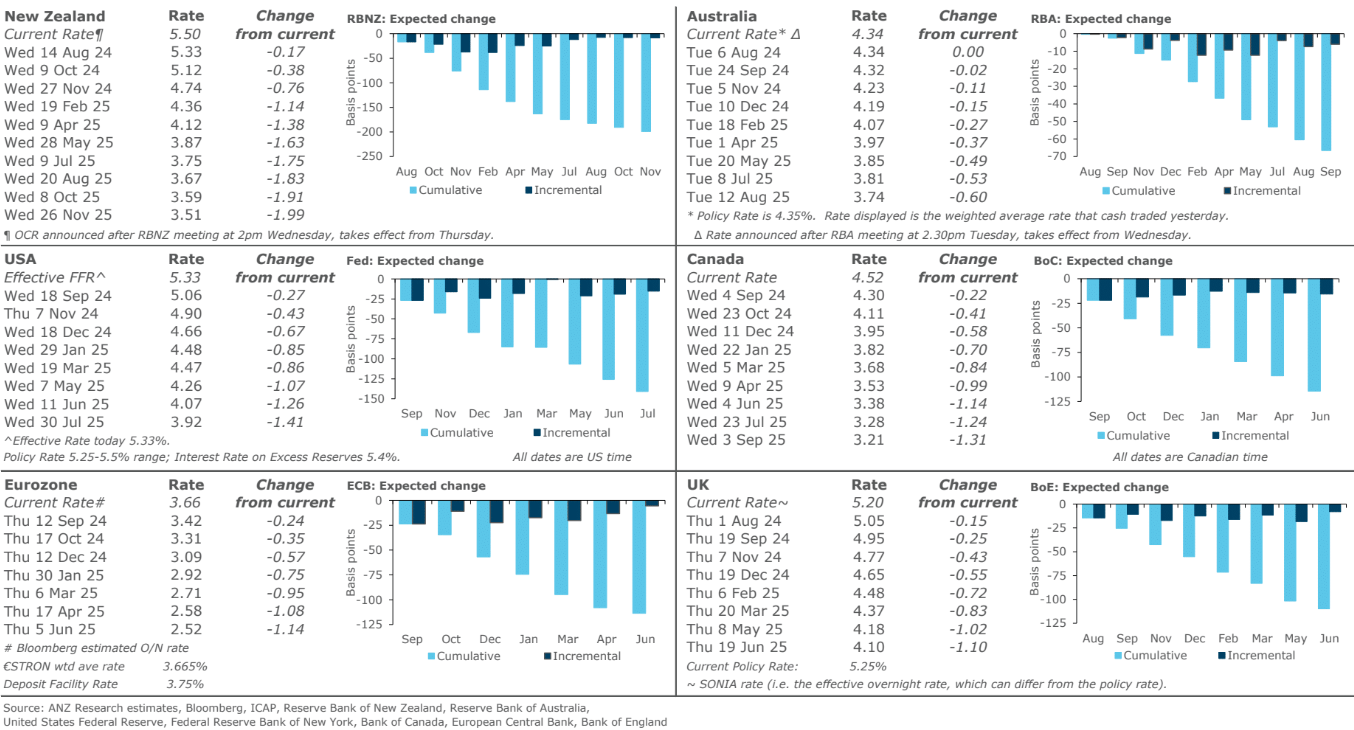

The emerging Australian monetary easing is fast catching up to the rest of the world.

This week began with cash rate futures barely pricing one cut in the next twelve months. Now it is three:

We are still meaningfully behind the rest of the world but that will pass for to reasons.

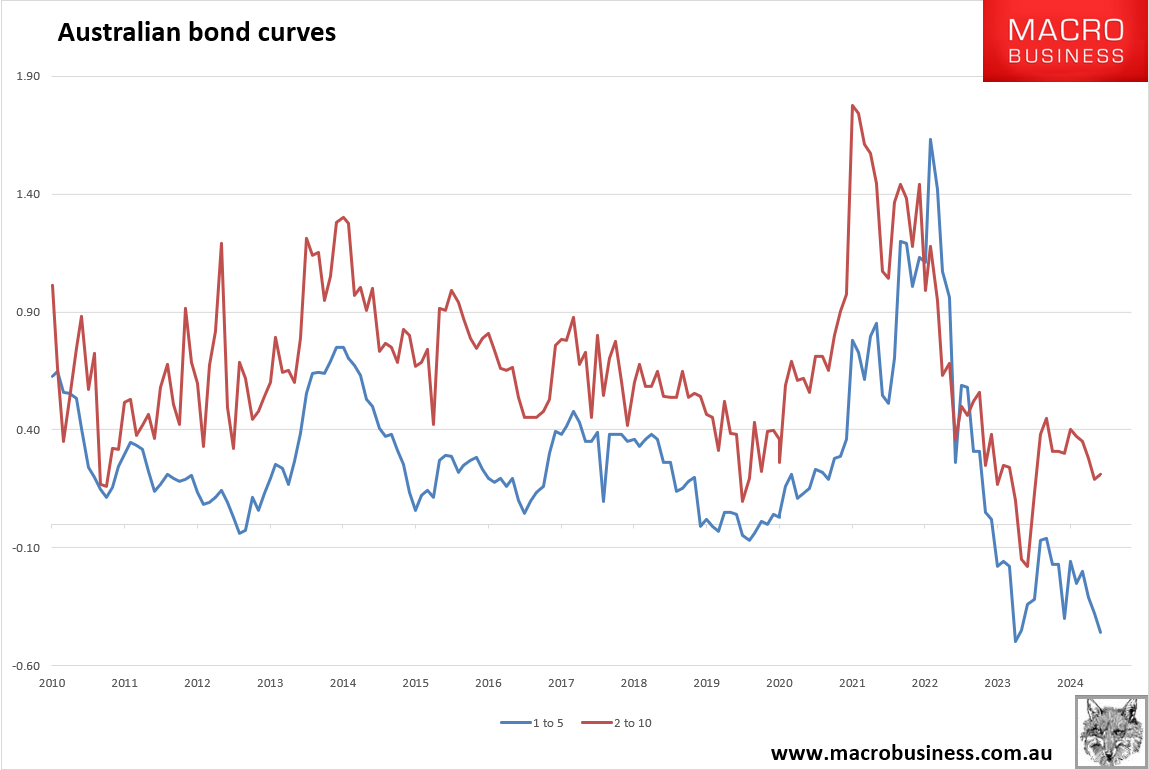

First, the endless per capita recession is intensifying in the 1-5 year bond curve and disinflation will too:

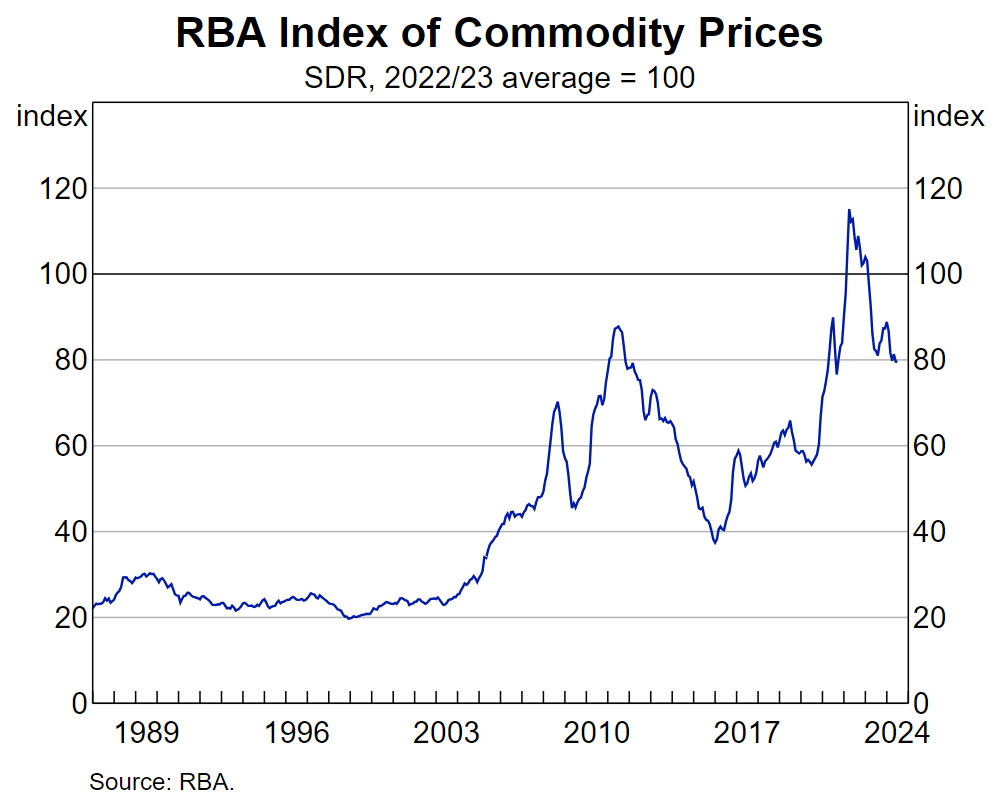

Second, Australia’s terms of trade are in free fall as iron ore coking coal capitulate. This will get much worse over 2025 and LNG plus thermal coal will join in:

I expect we will hit 60 next year and 40 over the next few years as the Pilbara killer arrives alongside the global LNG glut.

This immense income shock means interest rates will have to fall a very long way, not least because Canberra will respond with, you guessed it, increased immigration, ensuring the entire national income shock is visited upon you.