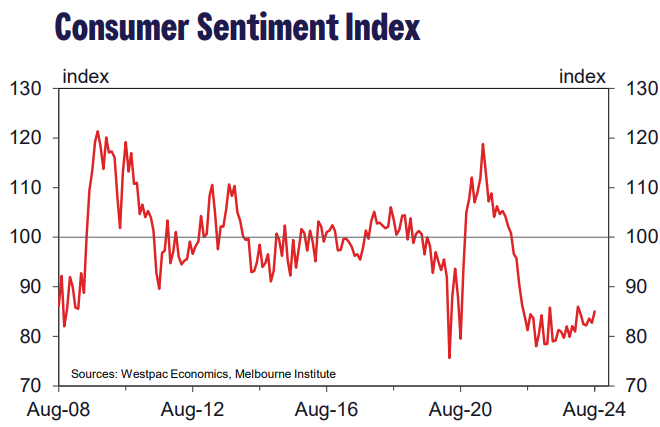

Westpac’s consumer sentiment index is finally showing some signs of life, although overall conditions remain recessionary.

Key Points:

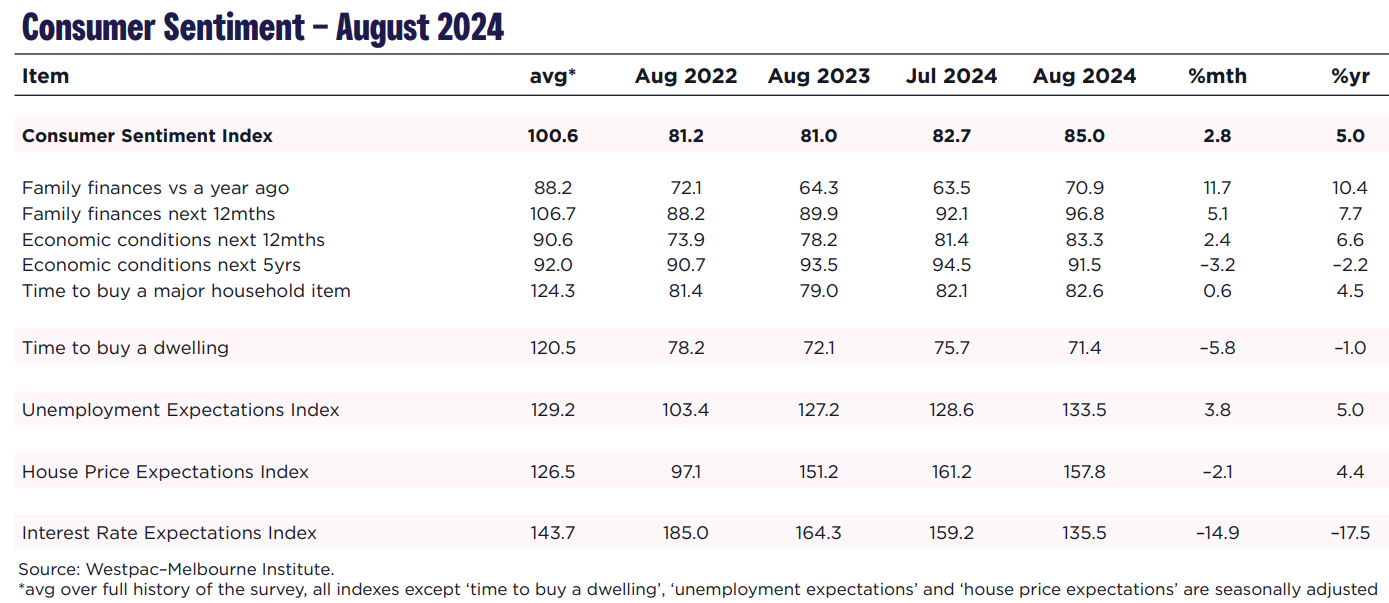

- The Westpac–Melbourne Institute Consumer Sentiment Index rose 2.8% to 85 in August from 82.7 in July.

- Westpac Consumer Sentiment up 2.8% to 85.

- Views on family finances bounce back from last month but remain weak.

- Some clearer signs of support from tax cuts and fiscal measures.

- Consumers less worried about further interest rate increases than last month.

- Australians still untroubled by jobs outlook.

- Home-buyer sentiment sinks to new lows as price expectations cool.

Consumer sentiment ticks up but pessimism still dominates:

Consumers breathed a small sigh of relief in August as the RBA Board left interest rates unchanged and the support coming from tax cuts and other fiscal measures became more apparent.

That said, the Index remains at weak levels by historical standards, stuck in the 78–86 range that has prevailed for over two years now.

The survey detail shows that cost of living and rate rise concerns are still weighing heavily.

Views on finances bounce back but remain weak

The component indexes show a clear improvement in the latest sentiment data, centred around family finances.

The ‘family finances vs a year ago’ sub-index surged 11.7% in August, the biggest monthly gain in nine years (excluding the COVID period) lifting the sub-index to 70.9 – a two year high, albeit still a very weak level overall.

The monthly rise was particularly strong amongst low-income earners; 18–34 year olds and those aged over 65; and in South Australia, Queensland and Victoria.

Consumer expectations for their finances also improved, with the ‘family finances, next 12 months’ sub-index rising 5.1% to 96.8. This is the highest level since the interest rate tightening cycle began in May 2022.

While these monthly moves are impressive, both ‘family finances’ sub-indexes were coming off sizeable declines and extremely weak levels in July.

Even with these gains, the August reads on both sub-indexes were still in the bottom 15% of monthly readings since the series began in the mid-1970s.

Other components were showed much smaller, mixed shifts. Consumers are a little less pessimistic about the near term economic outlook but a little more downbeat on the medium term view, with buyer sentiment largely unchanged at very weak levels.

The sub-index tracking assessments of the ‘economic outlook, next 12 months’ rose 2.4% to 83.3, up slightly on the month but essentially unchanged since May.

The ‘economic outlook, next 5 years’ sub-index declined 3.2% to 91.5.

The ‘time to buy a major item’ sub-index edged up 0.6% to 82.6 but is still well below its long-run average of 124, continuing to track in the bottom 4% of reads historically.

Consumers less worried about rate increases

Rate rise fears subsided noticeably in the month.

The Westpac–Melbourne Institute Mortgage Rate Expectations Index tracks consumer expectations for variable mortgage rates over the next 12 months. It fell 14.9% in August, unwinding about two thirds of the 36% surge seen over the previous three months.

Notably, about 10% of that move came before the RBA announced its decision to leave interest rates on hold in August, suggesting rate rise fears had already eased significantly following the June quarter inflation update, and perhaps in response to a clearer signs of a monetary easing cycle emerging abroad.

At 135.5, the Westpac–Melbourne Institute Mortgage Rate Expectations Index is now back below its historical average of 143.7. Just 45% of consumers surveyed after the RBA decision expect mortgage rates to rise over the next year, the fi rst ‘sub-50%’ read since May.

Consumers remain relatively untroubled about the outlook for jobs. The Westpac–Melbourne Institute Unemployment Expectations Index deteriorated slightly, rising 3.8% to 133.5 in August (recall that higher index reads mean more consumers expect unemployment to rise over the year ahead).

Overall, sentiment around jobs is a touch worse than long run averages but still consistent with gradual slowing in labour market conditions.

That said, the detail suggests there is more unease amongst those employed in professional services, the public sector and in hospitality and recreational services while job-loss fears have eased materially amongst those employed in construction.

Home-buyer sentiment sinks to new lows

Around housing, home buyer sentiment sank back to new lows but consumers’ price expectations cooled a touch.

The ‘time to buy a dwelling’ index fell 5.8% to 71.4, a new low for the year. Buyer sentiment dropped to exceptionally weak levels in NSW (66.1) but is a little less bleak in Victoria (76.9) and South Australia (76.0).

Nationally, the index has been at extremely weak levels, at or below the 80 mark, for two and a half years now, easily the most sustained period of depressed homebuyer sentiment over the history of the survey. The average index read over the last fifty years is 120.

The Westpac Melbourne Institute Index of House Price Expectations declined 2.1% to 157.8, taking the index back to around the levels seen late last year.

Consumers in Western Australia and South Australia remain much more bullish on the price outlook than consumers across the eastern seaboard. The average gap between index reads in these two groups is now close to 20pts.

Price expectations are particularly subdued in Victoria where the state index read of 143.5 is close to the long run average seen historically.

Conclusion

The Reserve Bank Board next meets on September 23–24. The Governor has all but ruled out rate cuts in the short term, and the flow of data between now and the meeting will not add much new information about the inflation pulse.

Given this, it seems likely that the Board will hold the cash rate unchanged at its next meeting.