The Reserve Bank of Australia (RBA) has published a Bulletin article entitled “Recent Drivers of Housing Loan Arrears”.

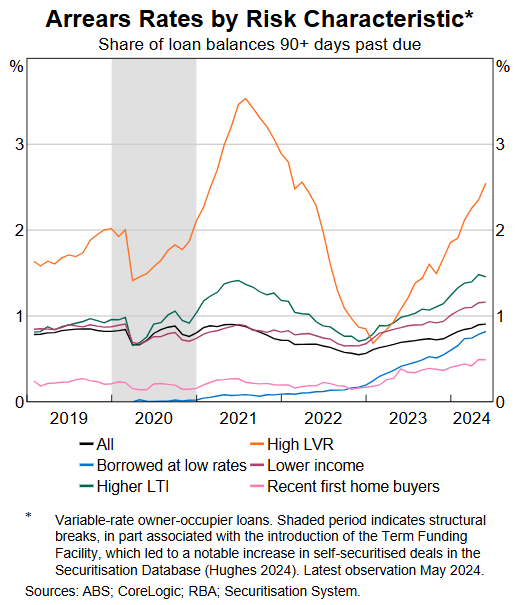

To nobody’s surprise, the RBA found that “highly leveraged borrowers have been most likely to fall into arrears since 2022, consistent with their generally higher arrears rates and greater vulnerability to challenging economic conditions”.

“This largely reflects their smaller buffers making them less resilient to changes in their mortgage payments or budgets”.

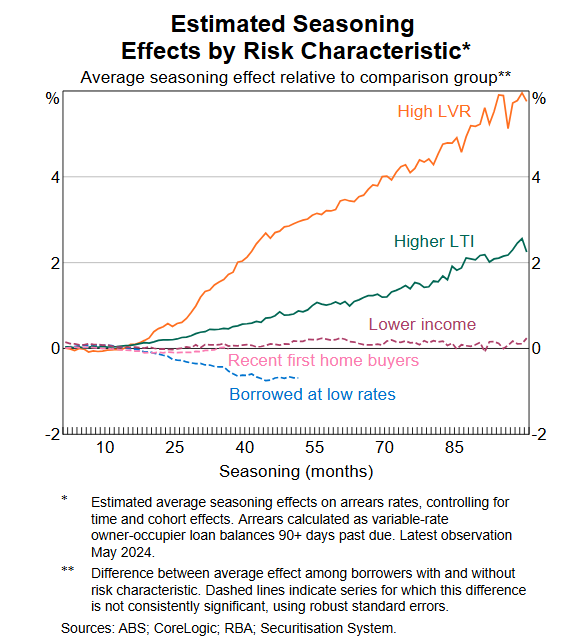

Arrears rates also tend to increase by more with loan age among highly leveraged borrowers:

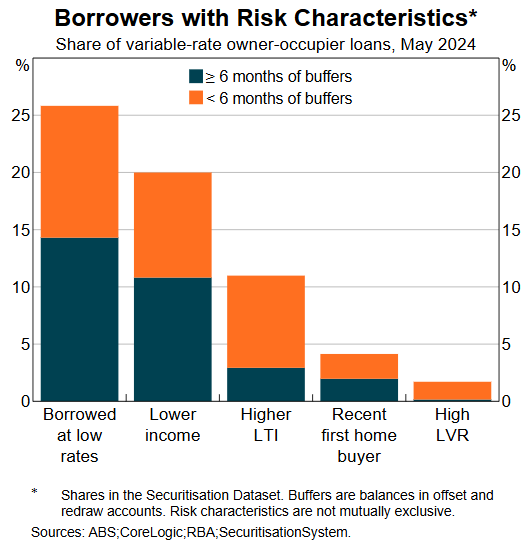

Highly leveraged borrowers have low buffers. Although, thankfully, they also comprise a relatively small share of total loans, mitigating the risk to the financial system:

The RBA concludes with the following assessment of mortgage risks:

“Looking ahead, household budget pressures are expected to remain elevated for some time but to ease a little as inflation moderates further”.

“The expected gradual further labour market easing will be challenging for households who lose work”.

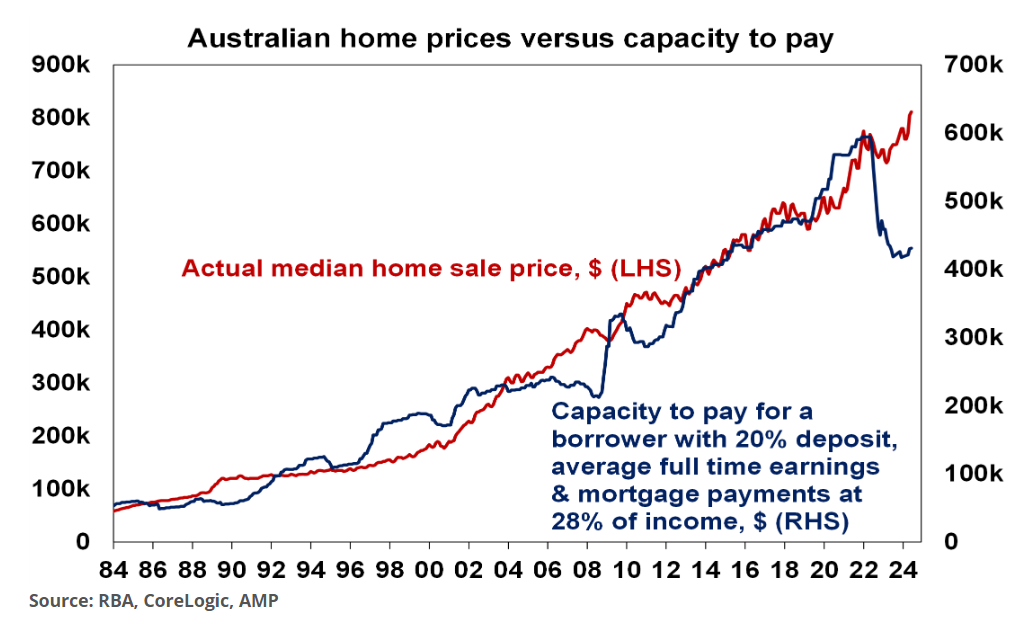

I will add that the growing gap between house prices and borrowing capacity could entice households into taking out higher LVR loans.

This could pose a material problem for the banking system if unemployment spikes and house prices fall.