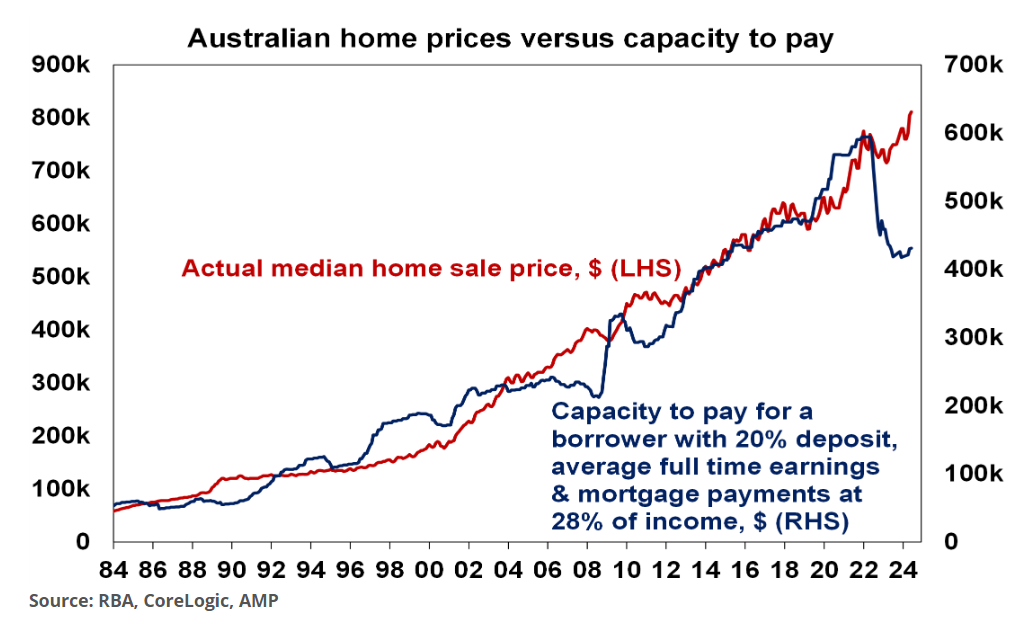

In the past two years, we have seen the gap between home values and the capacity to pay widen to historic proportions:

The deterioration in affordability reflects the circa 50% rise in mortgage repayments following the RBA’s monetary tightening cycle, combined with the ongoing appreciation in home values.

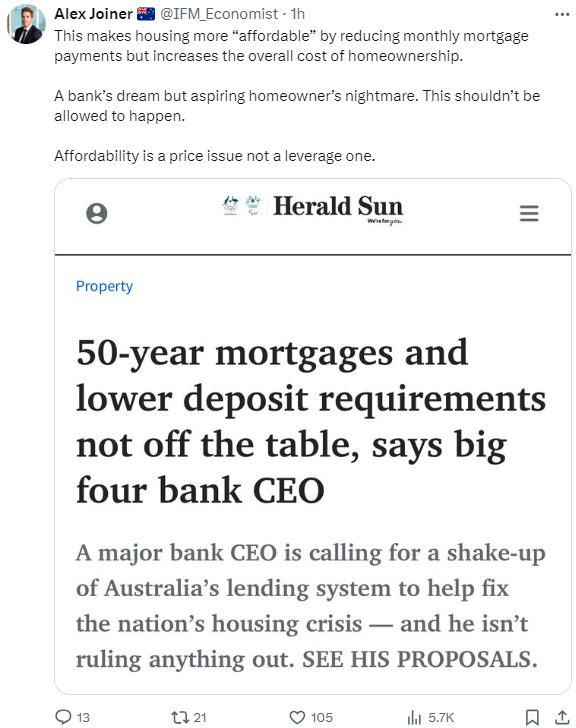

With most borrowers hitting an affordability ceiling, ANZ chief executive Shayne Elliott is calling for a shake-up of home lending to sucker more borrowers into the market. And this could involve measures like 50-year mortgages to lower monthly repayments.

[Elliott] said “little things” like the 3% buffer the Australian Prudential Regulation Authority (APRA) imposes on mortgagees through lenders to ensure they could service their loans if interest rates increased was perhaps “too high”.

Mr Elliott added that reducing the typical deposit requirement on a home to avoid paying lender’s mortgage insurance (LMI) from 20% to 15% “should also be on the table”…

“All those things should be thought about; how long mortgages are, what’s the actual deposit we do, what buffers we put in place, what exclusions we apply. I think all of that is absolutely fair to review and decide whether we’ve got our settings right.”

He noted that there was no law that said that a bank couldn’t offer 40-year loans or even 50-year loans, but it needed to be appropriate for the homebuyer.

Let’s put to one side the fact that these types of moves by mortgage lenders would contradict the RBA’s efforts to temper demand and inflation, and would put upward pressure on interest rates (other things equal).

They are another blatant attempt to boost housing demand and push prices even higher.

Allowing people to borrow more for housing would do what it always does: raise debt levels and lead to increased long-term housing costs.

As Alex Joiner notes above, “affordability is a price issue, not a leverage one”.

These types of measures would be a great deal for banks who would make fatter profits from indebted mortgage slaves.

But they would be a dud deal for aspiring home owners and the broader economy.

The last 20 years have provided living proof of how the story will conclude: mortgage debt will balloon and home values will rise further out of reach.