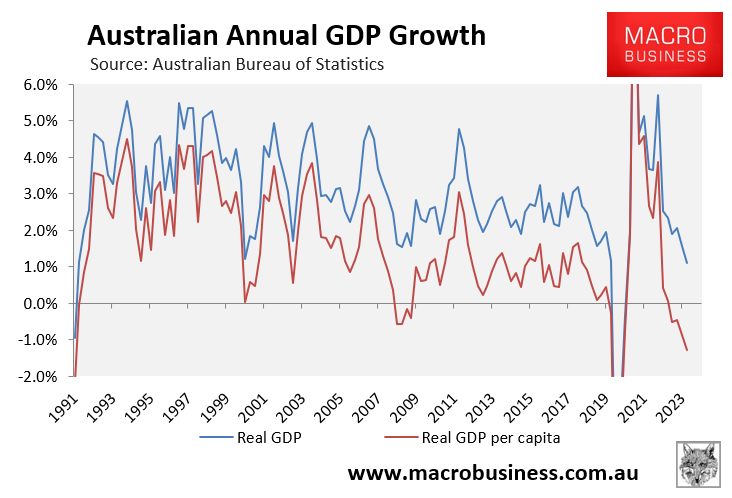

Australians are already experiencing their deepest recession since the early 1990s (outside of the pandemic lockdowns) following five consecutive declines in real per capita GDP:

Despite the highest population growth since the early 1950s, aggregate GDP has also fallen to its lowest level since the early 1990s recession (outside of the pandemic lockdowns).

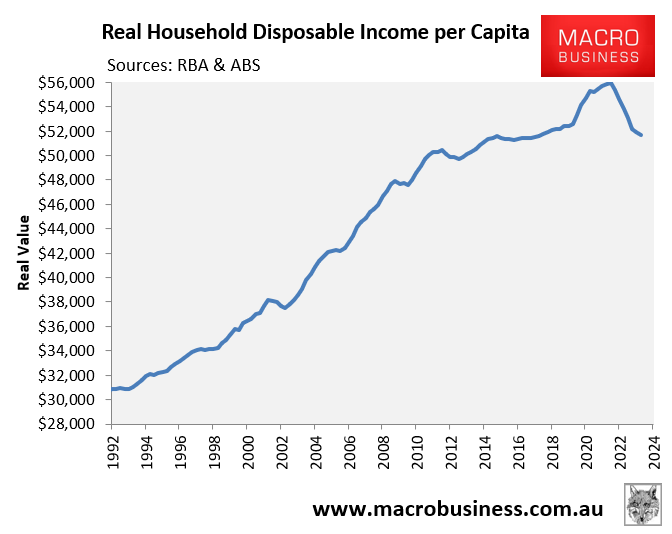

The situation for Australian households is particularly bleak, with real per capita household disposable incomes recording their biggest since records began around 60 years ago:

Australia’s most vocal interest rate hawks have warned that Australia’s economy has a high chance of plunging into a headline recession if the Reserve Bank of Australia (RBA) follows their advice and hikes interest rates at their upcoming board meetings.

“There’s likely to be a technical recession as growth stalls”, economist Warren Hogan said on Friday. “We will be struggling to keep unemployment under 5%”.

Fellow rate hawk economist, Richard Holden, put the odds of a recession at 50% to 60% if the RBA hikes rates.

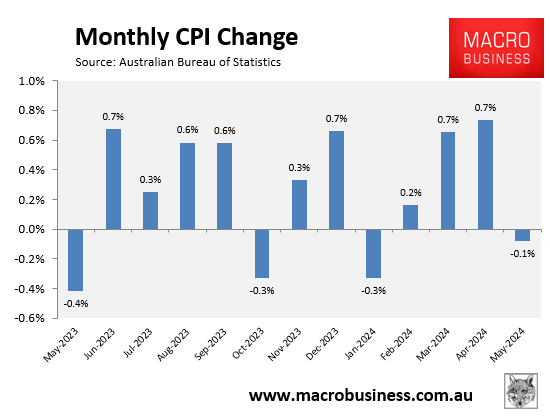

Thankfully, the RBA seems more measured in their response to last week’s ugly 4.0% CPI indicator number, which caused more by “base effects” than an actual rise in monthly inflation:

Newly imported deputy RBA governor, Andrew Hauser, threw a wet blanket over interest rate speculation with his statement that “it would be a bad mistake to set policy on the basis of one number, and we don’t intend to do that”.

Hauser is clearly referring to the spate of incoming data that will arrive ahead of the August board meeting, namely two retail sales prints, the June labour market release, and the all-important June quarter CPI number.

As argued by Ross Gittins on Monday, the CPI indicator has “proved an expensive disaster, having added at least as much “noise” as “signal” to the public debate about what’s happening to inflation. Why? Because many of the prices the index includes aren’t actually measured monthly”.

“Many are measured quarterly, and some only annually. In consequence, the monthly results can be quite misleading. Do you realise that, at a time when we’re supposedly so worried that prices are rising so strongly, every so often the monthly figures tell us prices overall have fallen during the month?”

“In an ideal world, the people managing the macroeconomy need as much statistical information as possible, as frequently as possible. But in the hugely imperfect world we live in, paying good taxpayers’ money to produce such dodgy numbers just encourages the speculators to run around fearing the sky is falling”.

“The Reserve has made it clear it’s only the less-unreliable quarterly figures it takes seriously but, as last week reminded us, that hasn’t stopped the people who make their living from speculation”.

It is also important to recognise that the RBA now has dual mandates: 1) price stability; and 2) full employment, which are supposed to carry equal weighting.

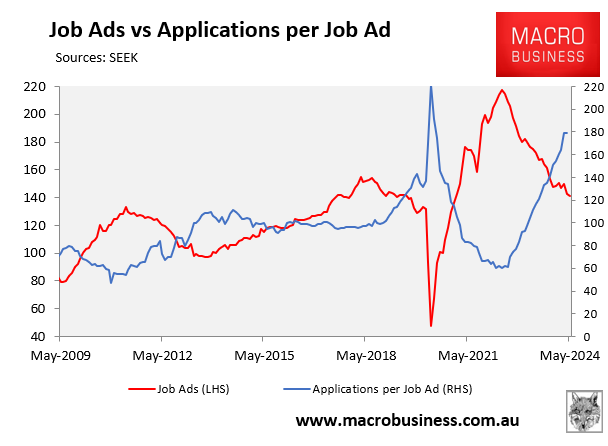

The fact that Australia’s labour market is weakening beyond that suggested by the official ABS numbers infers that the hurdle for another rate rise has increased:

This makes the upcoming June labour force release and Q2 CPI report vital to the RBA’s decision making.

The RBA will probably need to see the official labour force numbers strengthen and an ugly Q2 CPI print before deciding to lift rates.