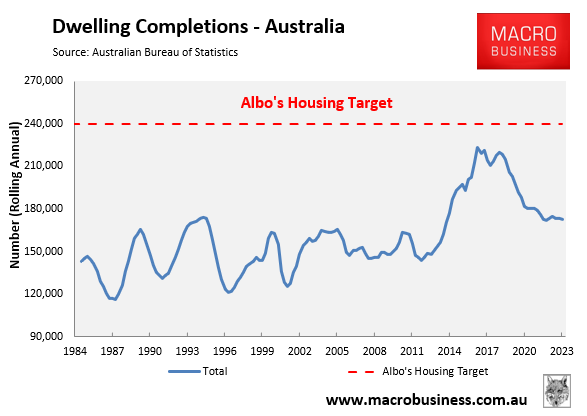

The Albanese government’s target to build 1.2 million homes over five years was always unrealistic.

The current record level for housing construction over a 12-month period was 223,600 in 2017, which was 7% below Labor’s annual target level of 240,000 homes.

The notion that Australia could magically build 240,000 homes a year for five consecutive years makes no sense when you consider the following:

- The official cash rate is currently 4.35%, versus just 1.5% in 2017.

- Construction costs are around 40% higher than they were in 2017.

- Unlike 2017, the residential building industry is competing for scarce labour and materials against government ‘big build’ infrastructure projects.

- Nearly 3000 construction companies collapsed in 2023-24, reducing capacity across the industry.

In short, macroeconomic conditions are likely to remain hostile to meeting Labor’s housing target. Accordingly, construction rates are likely to remain depressed.

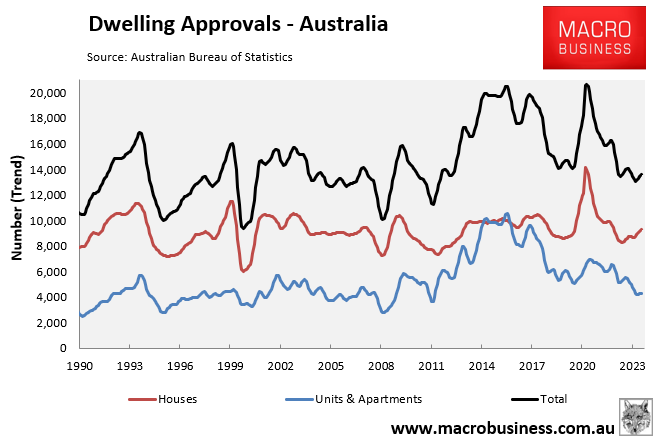

Indeed, Tuesday’s dwelling approvals data highlighted the point.

In monthly trend terms, only 13,586 dwellings were approved for construction in May, 6,414 (32%) below the run rate of 20,000 required to meet the Albanese government’s target:

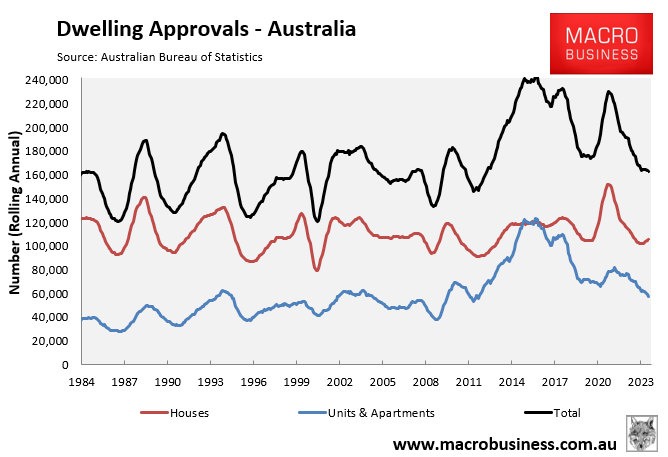

Annual dwelling approvals fell to their lowest level since March 2013, with just 163,316 dwellings approved for construction.

This was 76,684 (32%) below the 240,000 annual run rate required to meet the Albanese government’s target.

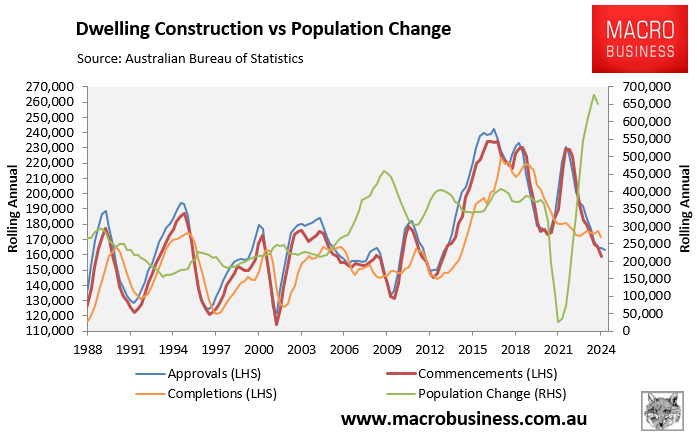

Finally, the next chart plots the various ABS measures of dwelling construction—approvals, commencements and completions—against annual population growth:

As you can see, a gargantuan gap has opened up between population demand and new housing supply.

Clearly, the only genuine solution to Australia’s housing crisis is for the federal government to dramatically reduce net overseas migration.

Otherwise, the supply situation will continue to deteriorate.