CBA senior economist Belinda Allen has written up an interesting analysis of spending habits by CBA customers over the 2023-24 financial year.

The analysis shows that lower-income renting households have been the most negatively impacted by the rising cost of living and have slowed spending the most.

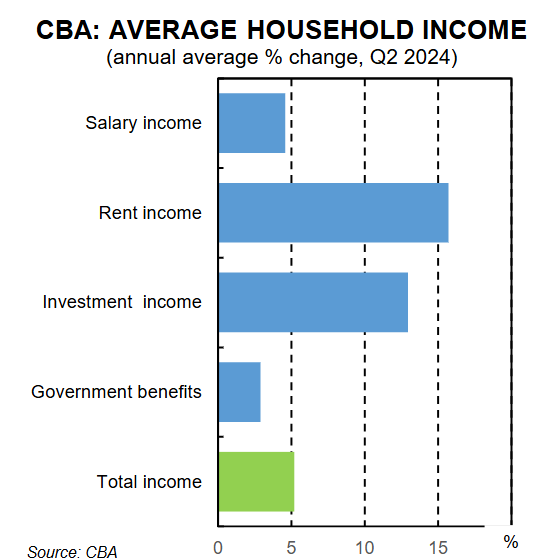

On the income side, the average CBA household’s salary income has risen by 4.6% over the past year, the slowest rate of growth since the middle of the pandemic.

Income from rent and investments has also risen strongly, lifting total average household income to around 5%.

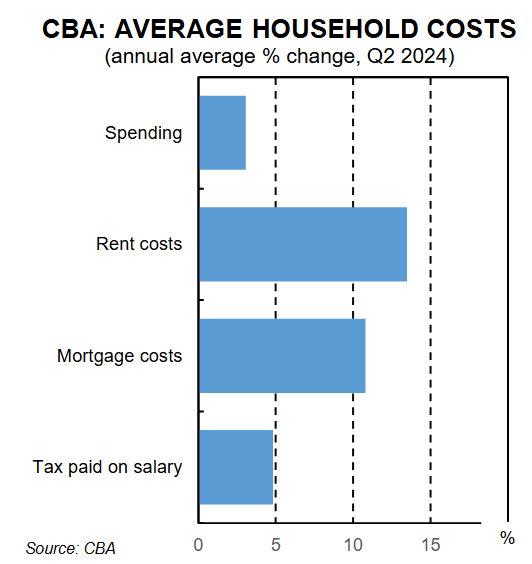

On the cost side, rental costs have risen by around 13% and mortgage costs by just over 10% in the 2023-24 financial year. Taxes paid on salaries also rose by nearly 5%.

Outside of rent and mortgage costs, CBA households increased their spending by only 3.1% in 2023-24 – i.e., by less than inflation.

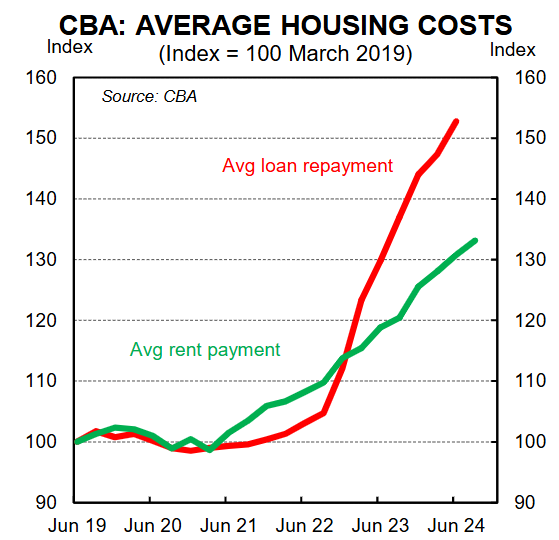

The next chart from CBA shows that rent and mortgage payments have soared in recent years:

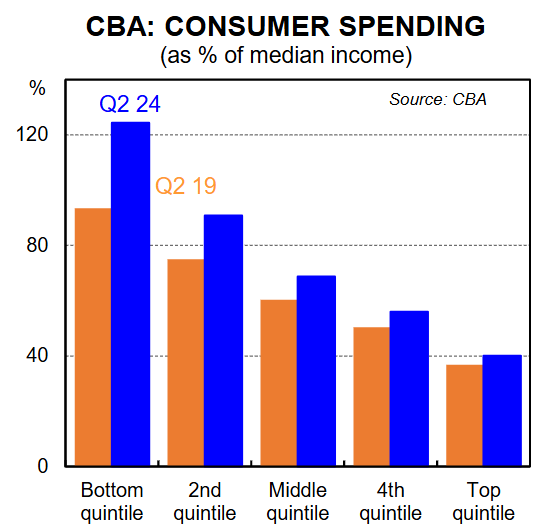

The growing spending on essentials has lifted the marginal propensity to consume (MPC), especially for lower income quintiles:

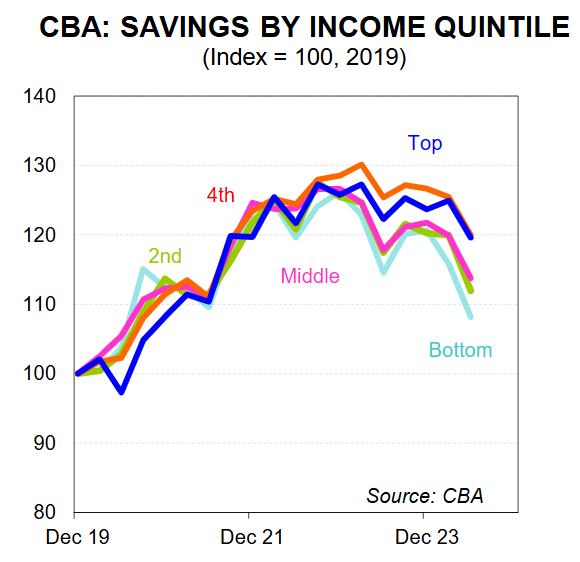

While overall average household savings remain higher than 2019 levels, lower income quintiles have drawn down their savings to a much larger degree than higher income earners:

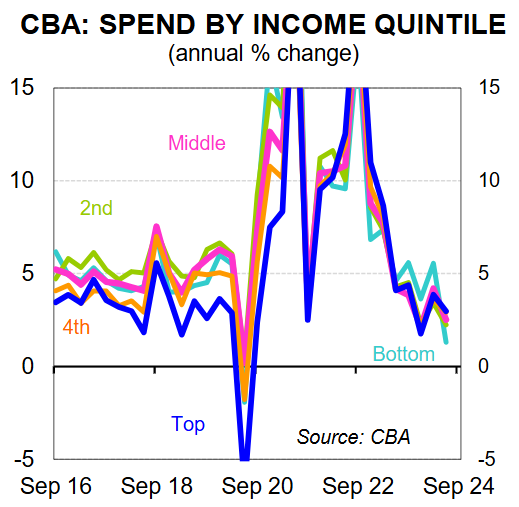

Finally, spending growth has slowed the most for the lowest income quintile and the least for the highest income quintile:

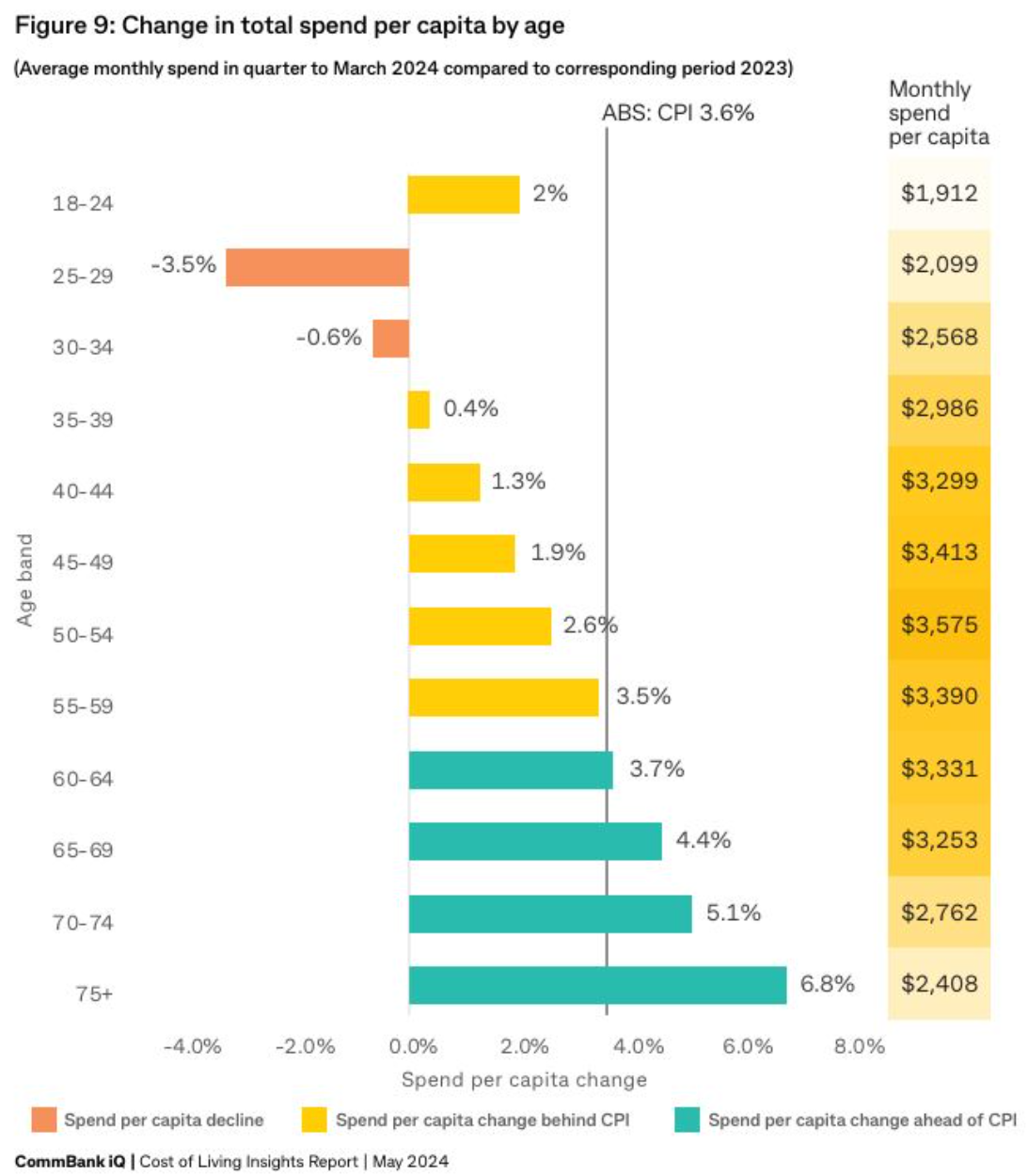

Data released earlier this year by CBA likewise showed that households aged between 25 and 34 have cut back on spending the most, reflecting the greater impact of rising rents and mortgage repayments: