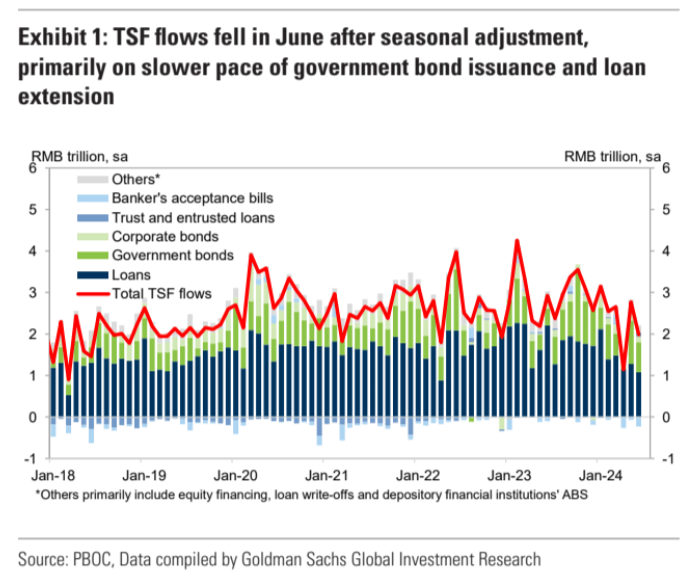

Chinese June credit was weaker than feared. The decline is fast, irreversible and Chinese authorities are making it worse.

Total social financing was RMB 32989bn in June versus a consensus of RMB 3400bn.

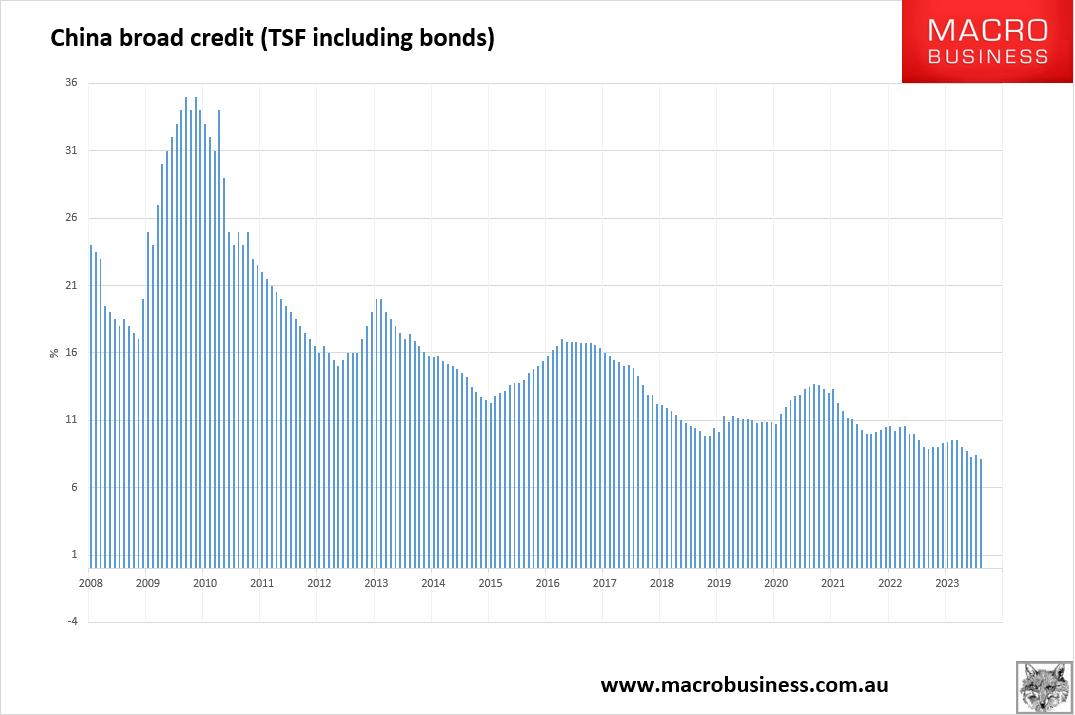

The monetary aggregates are plunging, with the stock of loans, or broad credit, at a record low of 8.1%:

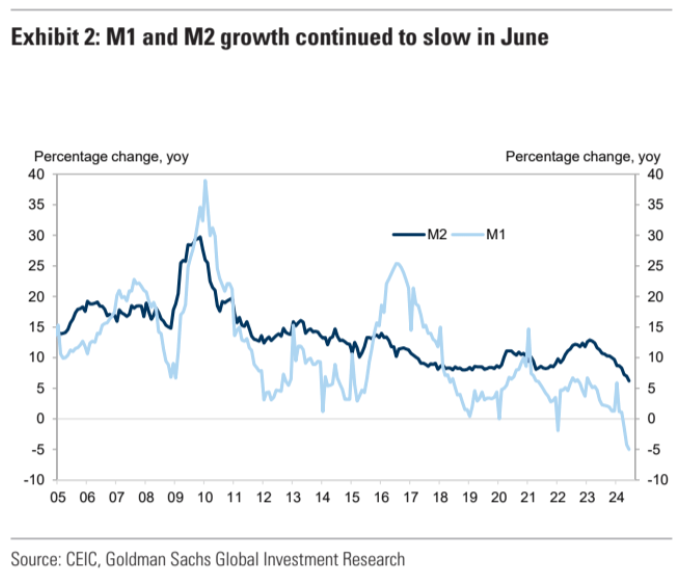

M2 and M1 are in freefall and the spread between them strongly suggests that monetary liquidity is trapped in the banking system in a classic symptom of debt-deflation:

Yet the PBoC loves it! Goldman:

June money and credit data indicated credit demand remained weak.

The recent policy communication suggests that the PBOC continues to focus on enhancing monetary policy transmission and downplay the importance of aggregate credit growth.

Looking ahead, the growth of new CNY loans and M2 may gradually slow down further.

We see some downside risks to our 2024 full-year TSF growth forecast (currently 9.0%).

As highlighted by the Securities Times(证券时报, a state-owned newspaper supervised by the People’s Daily), FX stability considerations amid elevated Fed/global interest rates and falling net interest margins among commercial banks continue to be solid constraints on sizeable policy rate cuts.

We maintain our forecast for a 25bp RRR cut in Q3 to facilitate government bond issuance, and a 10bp policy rate cut in Q4 after the first Fed rate cut in September expected by our US Economics team.

China is embedding high real interest rates and debt deflation. There is no recovery coming for property or domestic demand:

After our seasonal adjustment, household loans expanded mildly by 2.0% month-over-month annualized in June (vs. 1.9% in May), and the sequential growth of corporate loans slowed further (7.2% mom annualized in June vs. 8.8% in May).

China is positioning itself as an external sector-dependent economy just as the world closes its borders.

Is it about to change? BofA:

The Third Plenum is set to begin its 4-day session next Monday.

As we have flagged before, the focus will likely be on long-term structural reforms instead of counter cyclical easing.

In our view, key areas of discussions will likely include promoting tech self-sufficiency, addressing demographic headwinds and improving social welfare.

That looks right.

Nothing but deflation and more of it ahead for China.