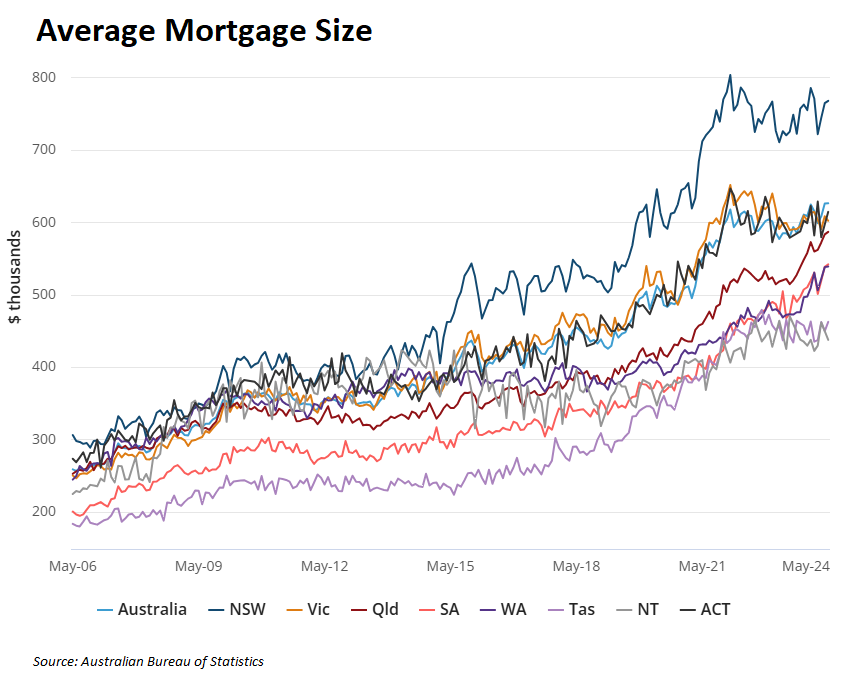

Data from the Australian Bureau of Statistics shows that the average new home loan for owner-occupiers reached a record high of $626,055 nationally in May.

In May, the average size of new home loans reached fresh highs in Queensland, South Australia, and Western Australia.

NSW still boasts the nation’s highest average home loan, at $767,584; however, this is below the state’s peak of $803,235 in early 2022. In contrast, the average home loan in Victoria fell to $601,891 in May, compared with a peak of $651,364 in 2022.

Sally Tindall of RateCity notes that home buyers are taking out bigger mortgage loans than ever, despite the cash rate rising to its highest level in 12 years.

“Over the last two years, buyers have seen their maximum borrowing capacity plummet, in some cases by hundreds of thousands of dollars, as a result of the RBA hikes, and yet the average new loan size has hit a new record high”, she said.

“It’s astounding to think owner-occupiers are, on average, taking out larger loans than ever before despite the fact the cash rate is sitting at a 12-year-high”.

Meanwhile, the National Debt Line (NDL) received 145,166 calls in the 2023-24 financial year, the highest number of calls in four years.

Financial counsellor Mike Dunkley says he is experiencing his busiest time since he has been with the NDL, with calls increasing over the latter half of 2023 as the impact of interest rate increases began to take their toll.

Dunkley says that most of the calls that the NDL gets are about mortgages and rents, while it has also been getting some calls about the Australian Taxation Office in recent months.

“I’ve been on the NDH now for 2.5 years and I reckon this is the busiest I’ve ever seen it”, he said.

“It’s going to be three things [people call in about]: number one: mortgages; number two: lots of rent; and lately, for probably the last five or six months, it’s the ATO”.

For his part, Financial Counselling Australia CEO Peter Gartlan notes that the demand for financial counsellors has “gone through the roof in recent times”.

“What the banks are saying is that approximately 75% to 80% of mortgage holders are in front of their mortgage”, Gartlan said. “What that means of course is that 20% are not”.

“So we are seeing that those are the people that are ringing us”, he said.

The debt situation would obviously worsen if the RBA raised interest rates further.

Those taking out record mortgages are playing with fire.

If you wish to save thousands of dollars in mortgage payments, try the MB Compare n Save mortgage comparison tool. It takes less than a minute.

And if you choose to refinance, Compare n Save will handle the process.