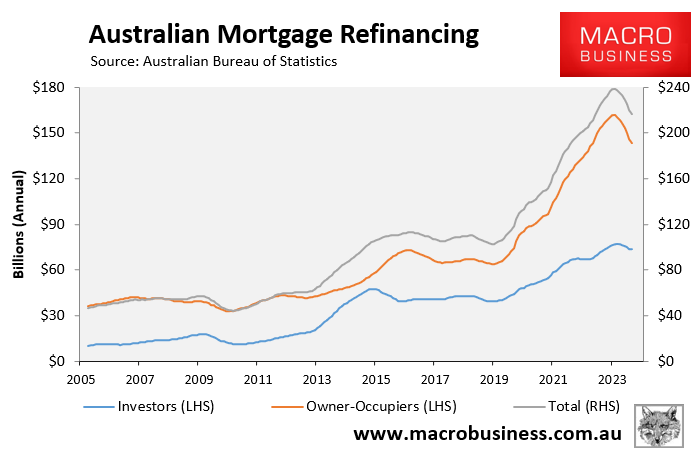

The prospect of the cash rate remaining on hold for some time has prompted a growing number of Australians to refinance their mortgages with a new lender or switch to an interest-only loan.

Finder estimates that around 500,000 Australians—about one in five borrowers—have switched to interest-only loans, while one in eight people has extended their mortgage loan period to reduce their repayments.

“The short-term saving is important”, Finder money editor Richard Whitten said. “If you can’t make ends meet, you’ve got to deal with today rather than tomorrow, but then you have to have that mind for the longer term”.

Meanwhile, the value of home loans that are in arrears by 30 to 89 days has risen to 0.66%.

With some economists now expecting an official interest rate cut to be delayed until mid-2025, Sally Tindall of RateCity says borrowers should budget for at least one more interest rate rise.

“Don’t start factoring in any kind of rate cuts into your broader budget”, she said.

“Focus on clearing one, if not two more interest rate rises. The extra money coming from the stage three tax cuts, will help support some families”.

Extending mortgage terms or switching to interest-only will obviously lower monthly repayments. However, this comes at the expense of paying more interest over one’s loan term.

RateCity figures also show that borrowers who have not refinanced since the beginning of this interest rate cycle may be paying an additional $277 a month versus those who moved to an average rate.

Therefore, it pays to undertake a health check of your mortgage to ascertain whether you can get a better deal.

If you wish to save thousands of dollars in mortgage payments, try the MB Compare n Save mortgage comparison tool. It takes less than a minute.

And if you choose to refinance, Compare n Save will handle the process.