DXY was soft last night:

AUD held its ground:

The uptrend versus North Asia is a powerful warning that AUD can’t get far:

Oil held:

Commods fell:

Not sure why miners were bid:

EM has taken the Fed hint:

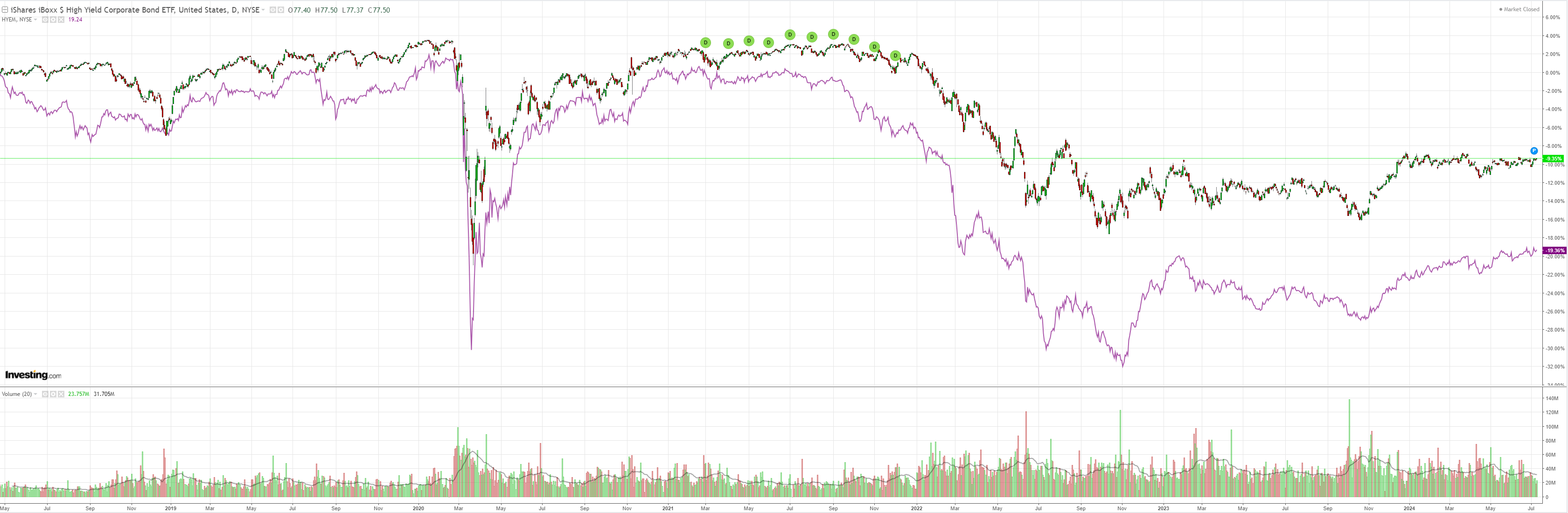

It would be nice if junk joined the party:

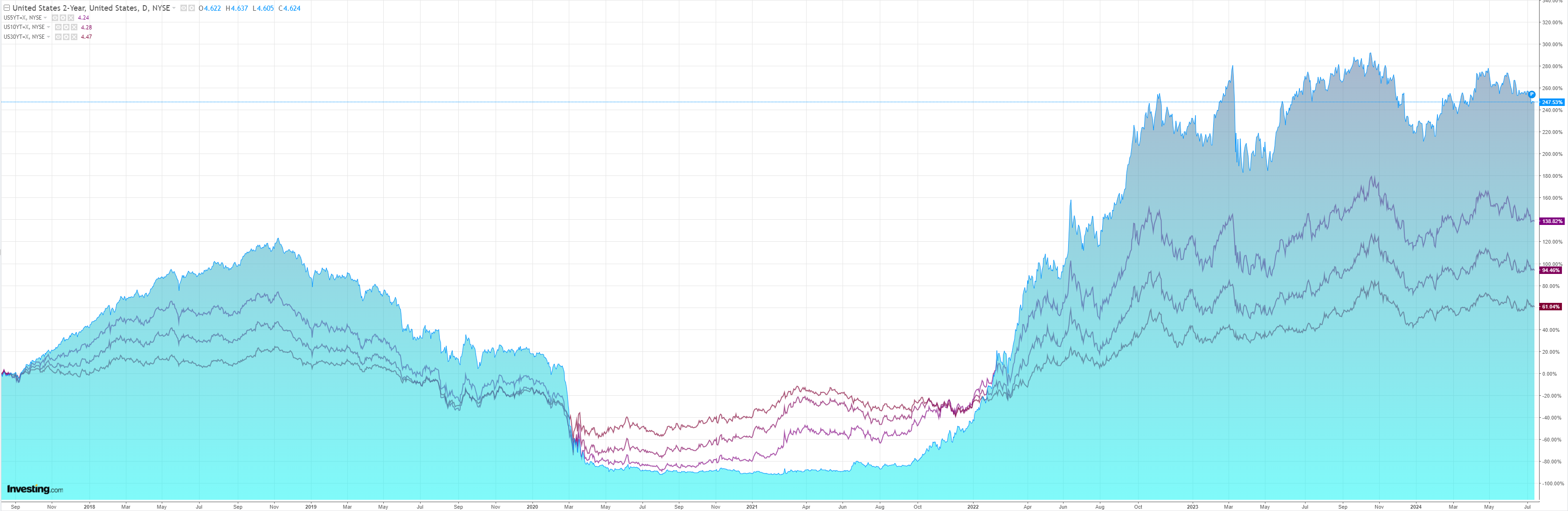

But yields are waiting too:

Stocks only go straight up:

Tonight’s US CPI is previewed by Credit Agricole:

Recent inflation reports have shown clear improvement after the pattern of upside surprises in Q124.

This was particularly evident in the downside surprise in May CPI, and we look for the pattern to continue with a similarly benign report in June.

Specifically, we project headline CPI to rise 0.1% MoM, though our forecast is right on the cusp of rounding down to a second consecutive flat print, with the YoY pace slowing to 3.1% from 3.3% and the NSA index at 314.560.

Energy will likely act as a drag once again, contributing to the soft MoM reading.

Furthermore, we expect core CPI to rise 0.2% MoM for a second straight month, a clear step down from prints of 0.4%MoM throughout Q124.

Unfavourable base effects would leave the YoY pace unchanged at 3.4%, though the three-month annualised pace should drop further.

Turning to the core details, we look for core goods to decline by around -0.2% MoM, with used cars to dip back into negative territory following an unexpected increase in May.

This would result in core goods slowing even further to -1.9% YoY from -1.7% YoY.

Services prices have been stickier overall, and that trend should continue, even if there has been some softening compared to the beginning of the year.

Here, we look for a MoM increase that could round down to 0.3%, up from 0.2% last month but below the Q124 average of 0.55%.

This would see the YoY pace holding steady at 5.3%.

The stronger-than-expected Q124 readings make clear that the path back to 2% is likely to be a bumpy one.

However, the improvement in May, along with our expectations for a softer report in June, suggest that disinflation is resuming, even if gradually.

As such, a report consistent with expectations would be another positive for the Fed, helping to slowly build confidence that inflation is sustainably on track to return to target.

The June report on its own will not be enough to reach the necessary confidence level to cut rates, but when combined with increasingly evident signs of labour market cooling, it could leave the Fed on track to cut rates in September.

Shelter remains the key and will keep falling.

AUD ready for higher short-term.