The notion that the Reserve Bank of Australia (RBA) needs to hike the official cash rate (OCR) further was put into question on Tuesday amid a hat-trick of weak economic data.

Three private surveys were released on Tuesday: (1) NAB June Business Survey; (2) WBC/MI July Consumer Sentiment Survey; and (3) SEEK’s June Employment Dashboard. All three surveys showed that the economy continues to soften.

The Head of Australian Economics at CBA, Gareth Aird, has examined this data, which is summarised below.

NAB’s June Business Survey shows broad-based weakness:

First, NAB’s June Business Survey showed that business conditions continued to ease, continuing the trend that has been in play since late 2022.

The headline conditions index dipped from +6 to +4 and is now comfortably below its long-run average of +6.5:

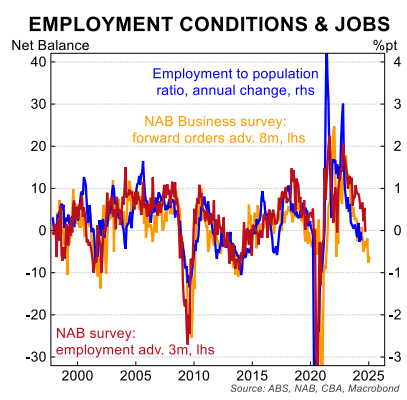

Aird notes that “we may be starting to see some convergence between employment growth and GDP growth”.

“Forward orders from the NAB business survey (-6 in June) have for some time been signalling that employment growth would step down more materially. On that score, all eyes are on the ABS June labour force survey (to be released 18/7)”.

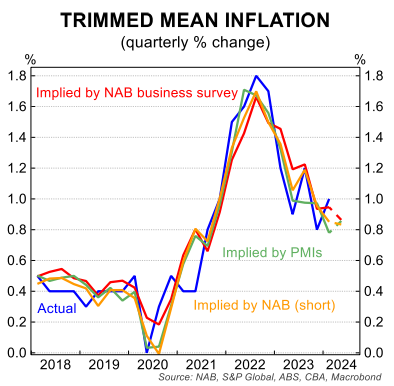

Encouragingly, the NAB Survey showed that final prices grew by 0.7% over the June quarter, down materially from 1.1% quarterly growth in May.

“This was the slowest rate of growth in output prices since February 2021”, noted Aird.

“The Judo Bank Australian PMI also eased in June (part of the S&P global suite of PMIs). Both the June NAB and Judo Bank consumer prices data leave us feeling a little more comfortable with our call for trimmed mean CPI to increase by 0.9%/qtr in Q2 24, although the risk does lie with a larger number”, Aird noted.

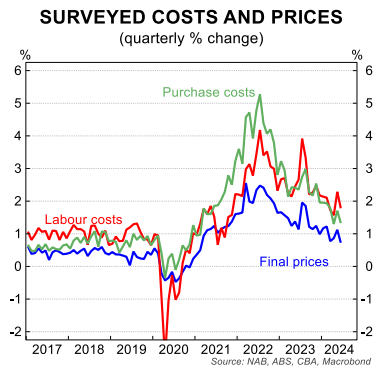

The June NAB Business Survey also reported lower purchase and labour cost growth:

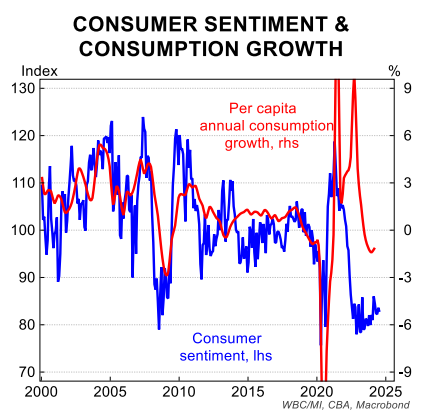

Consumer confidence stuck at recessionary levels:

The Westpac-Melbourne Institute consumer confidence index remained stuck at levels consistent with a recession or major negative economic shock.

“There is no change of narrative in the consumer sentiment survey”, noted Aird. “Households remained deeply concerned about both family finances and economic conditions over the next 12 months. And elevated inflation and heightened concerns over interest rates rising further continue to supress consumer sentiment”.

“The Stage 3 tax cuts and energy rebates have had no discernible positive impact on consumer sentiment”.

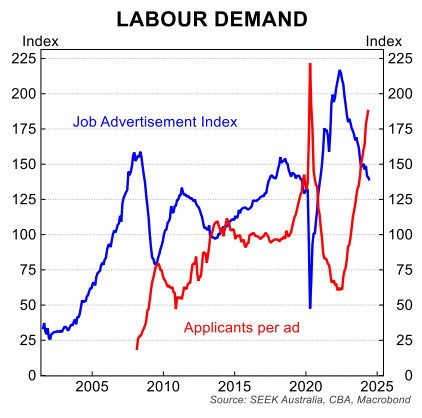

Jobs ads down, applications per job ad up:

Finally, SEEK’s June employment report showed further weakening in the labour market.

Jobs advertised on SEEK fell by 1.5% in June to be 17.1% higher year-on-year and tracking 36.2% below their peak.

The number of applicants per job ad surged 3.0% higher in May (latest available). Applicants per job ad are up by 61.6% over the year and an incredible 210.9% from their cyclical low in mid-2022.

“The ‘second tier’ SEEK job data suggests the labour market will continue to loosen”, noted Aird. “And we expect evidence of further labour market loosening to be in upcoming June ABS labour force survey”.

While the RBA will wait for the official June labour force report from the ABS and the Q2 CPI print before finalising its view on rates, the above data suggests that talk of rate hikes at the August board meeting was premature.