The question of which central bank will cut rates next is gaining attention in the wake of the Bank of Canada’s (BoC) decision to start its monetary easing cycle with a 0.25% cut to its official policy rate on Wednesday and the ECB’s 0.25% cut on Thursday.

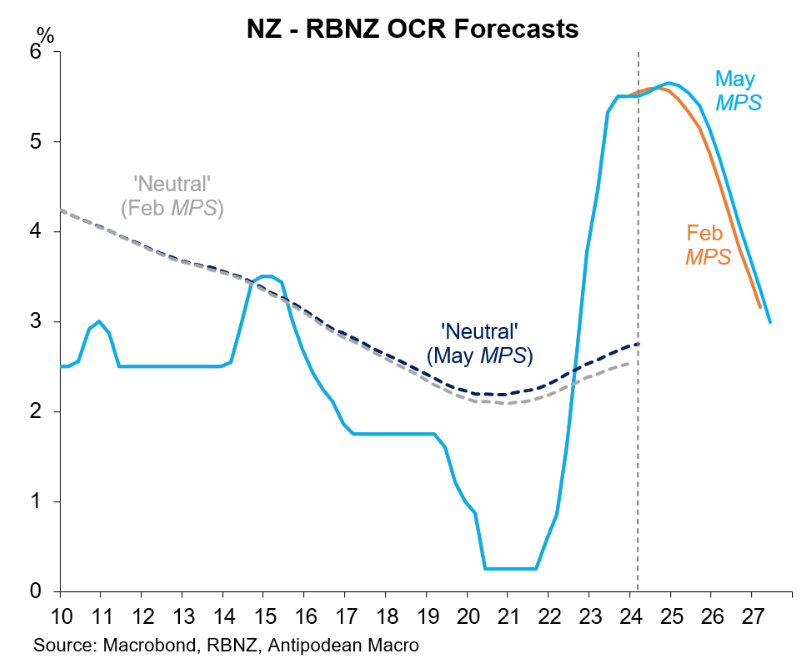

The Reserve Bank of New Zealand lifted its official cash rate forecast in its latest Monetary Policy Statement, released last month, suggesting that rates have not yet peaked:

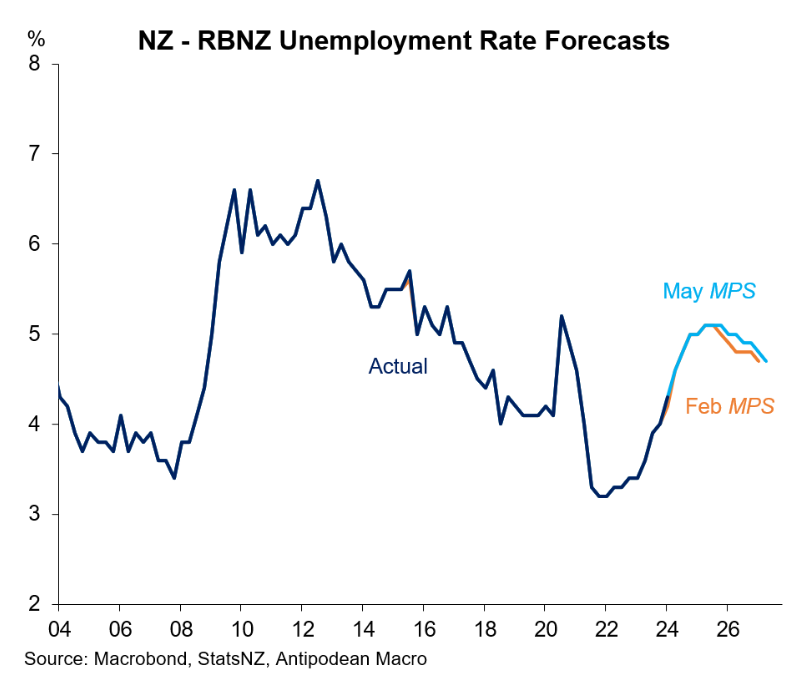

This came despite the Reserve Bank also lifting its unemployment forecast above 5%:

I don’t pay much heed to the Reserve Bank’s forecasts, given that the BoC was also speaking hawkishly on rates until recently.

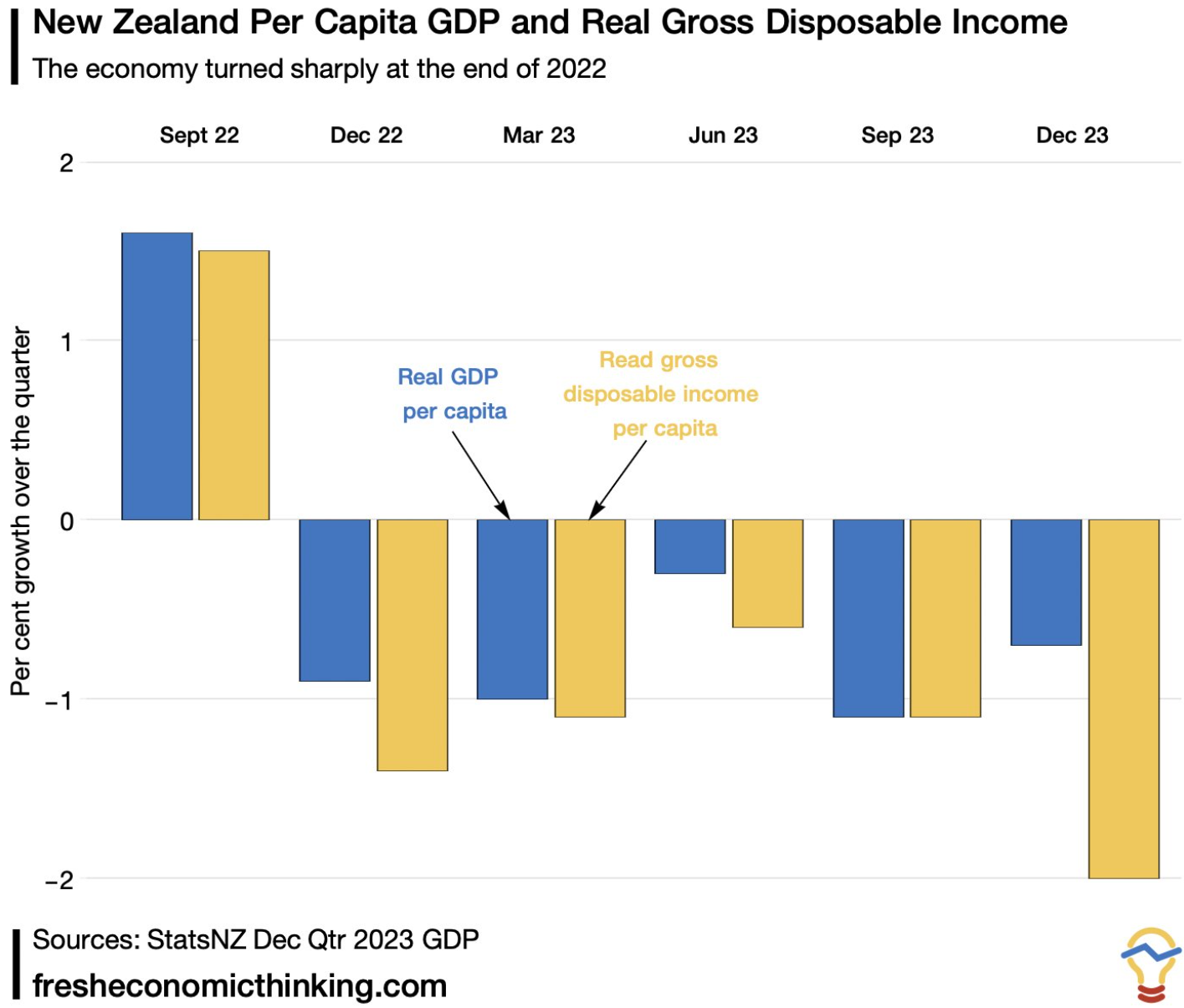

Moreover, like Canada, New Zealand’s economy is tanking.

New Zealand’s economy was already experiencing a technical recession in Q4 and a very deep technical recession:

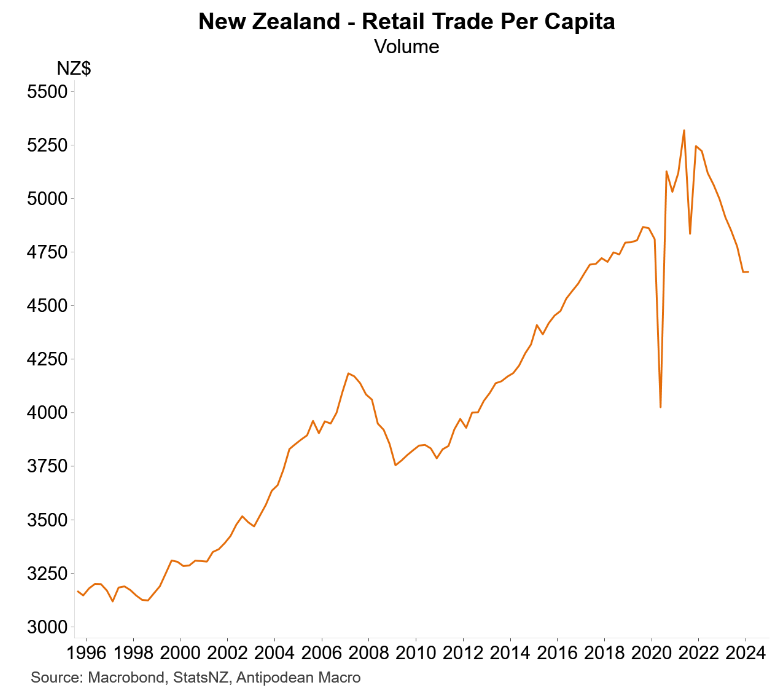

Retail sales per capita have since plummeted 12.4% below their peak:

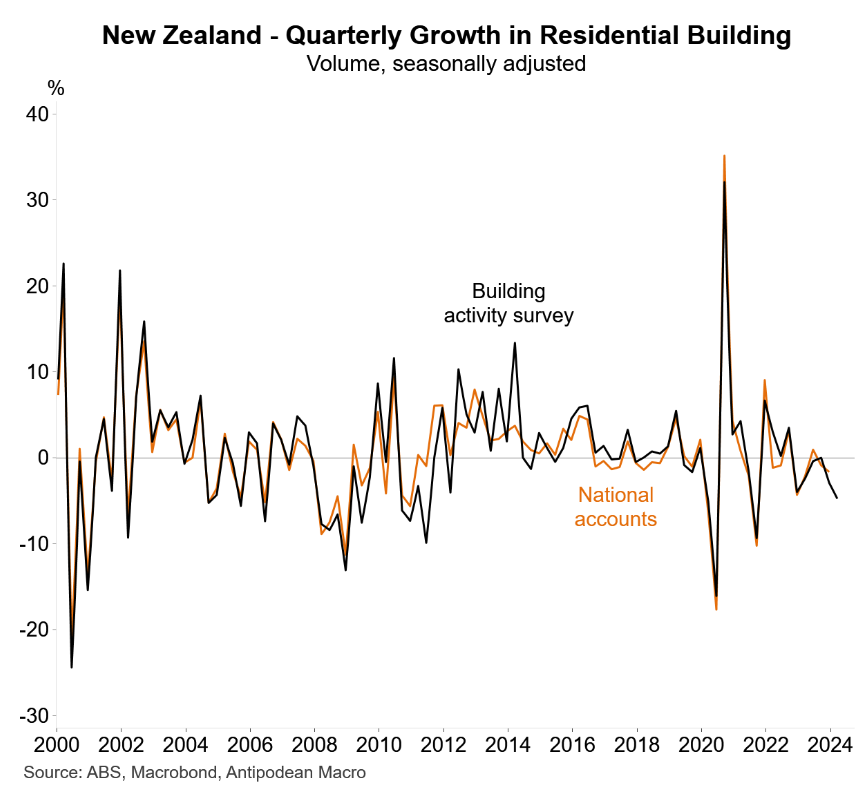

New Zealand residential building activity is also shrinking:

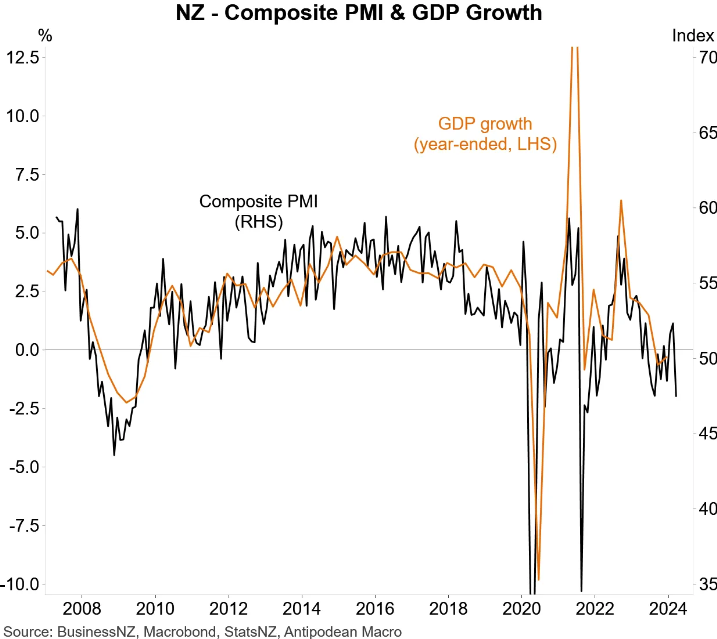

The composite PMI has likewise plunged and points to a worsening recession when the official GDP data for Q1 is released:

New Zealand’s official labour force data has weakened materially:

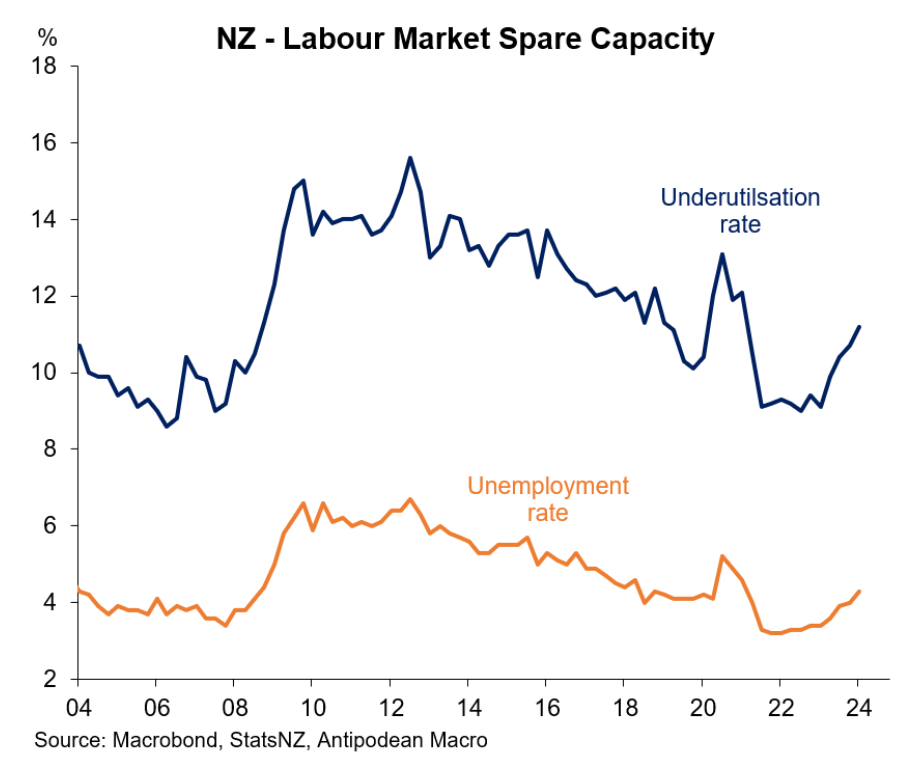

New Zealand’s unemployment and underemployment rates are rising, with more to come:

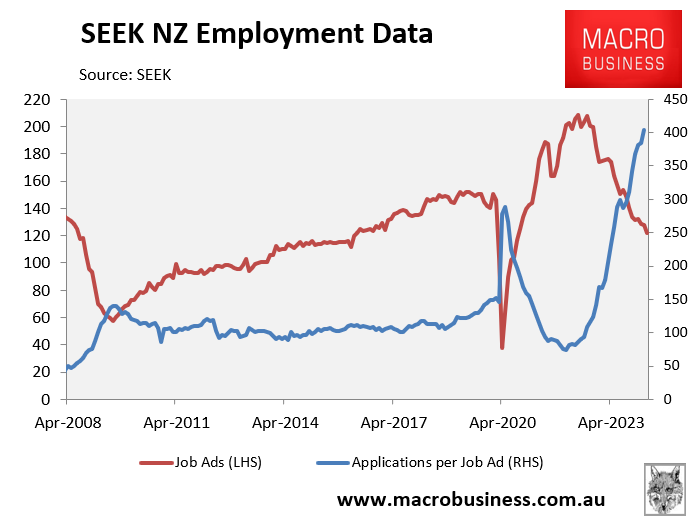

Worse is to come given the unprecedented surge in the number of applicants per job ad:

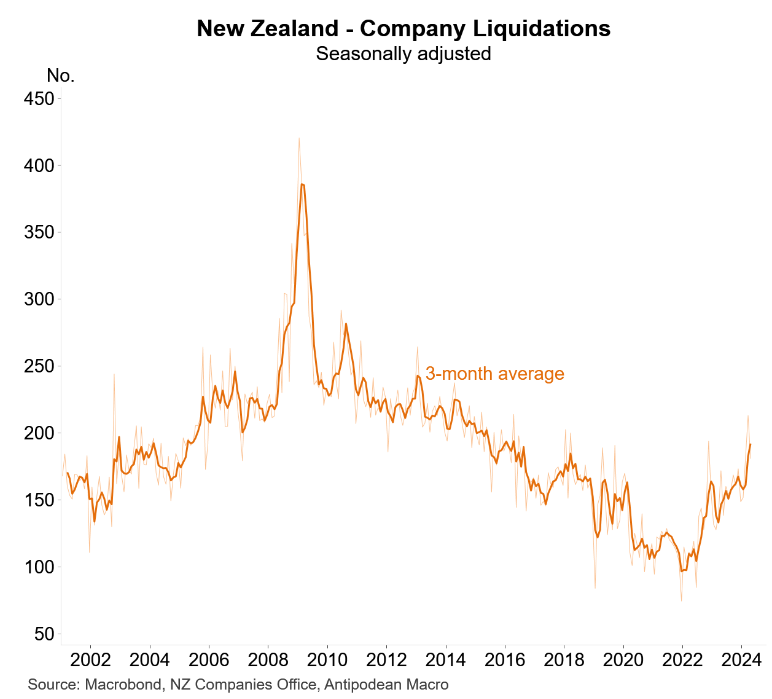

Company liquidations have also jumped in New Zealand:

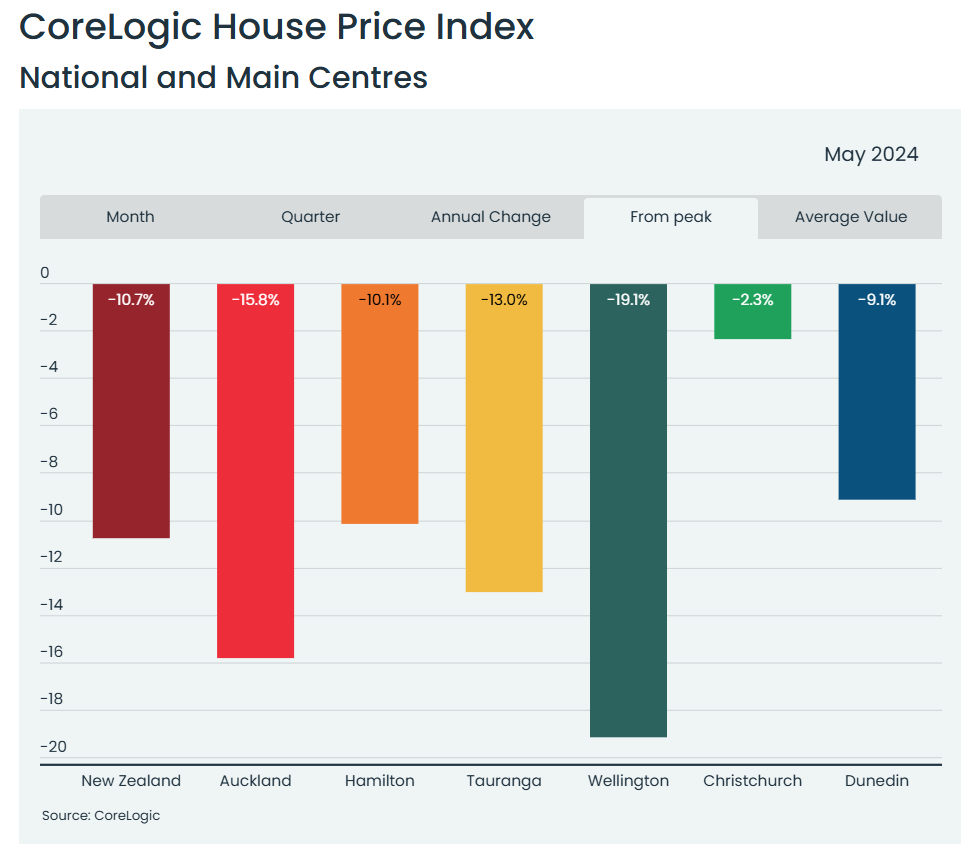

Unlike in Australia, New Zealand house prices are also declining and remain 10.7% lower than their peak.

CoreLogic’s house price index for May recorded a national average dwelling value of $931,438, down from $933,633 in in April and $934,806 in March.

The fall in average value was greater in Auckland, which fell to $1,279,454 in May, making a decline of $18,141 (-1.4%) over the last two months from $1,297,595 in March and $1,290,329 in April.

“Home value growth in Aotearoa has completely petered out in the past two months, with values dipping by 0.2% in May, after a minor fall in April”, CoreLogic reported.

Given the clear weakness in New Zealand’s economy, it is only a matter of time before the Reserve Bank follows the BoC and commences an easing cycle.