Westpac notes today that reduced motor fuel costs, energy subsidies, and cost-of-living support will lead to a very slight 0.1% increase in the CPI in September 2024. This will lower the annual pace of inflation to 2.7% and then 2.4% in the first half of 2025.

There is also a chance that declining petrol costs may cause the CPI to slightly decline in the September quarter, perhaps bringing inflation down to the middle of the RBA’s target range if crude oil prices fall steadily below US$80/bbl, says Westpac.

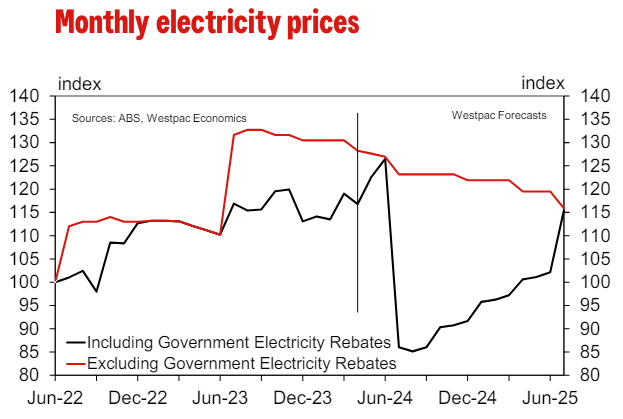

Westpac says that energy rebates will have a minimal effect on core inflation but will bring headline inflation back inside the RBA’s target range this year, earlier than the RBA is presently predicting (the RBA projections excluded the most recent energy rebates).

For the end of 2024 and 2025, Westpac’s Trimmed Mean forecast is still 3.5% and 2.8%, respectively.

The moderation of wages, the smaller-than-expected increase in the minimum wage by the Fair Work Commission in 2024, the improvement in productivity, and the moderation of unit labour cost inflation have been more significant.

Westpac anticipates a spike in the cost of electricity in the September quarter of 2025 because state and federal energy rebates will not be renewed. As a result, headline inflation will rise 3% annually in the second half of 2025.

Given a -0.4%mth fall in May 2023, Westpac’s early projection for the May Monthly CPI Indicator is for a flat print in the month, which will cause the annual pace to rise from 3.6%yr to 4.0%yr.

The specifics point to some tensions, however, with clothes and footwear prices being higher than anticipated. As a result, Westpac’s June quarter CPI prediction has these components revised upward.

Westpac’s initial projection for the June quarter CPI is 1.0% qtr/3.8% yr.

The RBA will examine headline volatility while concentrating on core inflation. A rate reduction in November might be possible if core inflation keeps falling, says Westpac.

I will only add that I can’t see energy rebates ending any time soon. The political cost of allowing bills to reflect the true state of affairs in gas and electricity markets is simply far too high.

It would be pointlessly destructive for the RBA to pretend otherwise.