Goldman with wrap on this week’s Chinese yawnulus:

The Politburo announced that the Third Plenum will be heldon Jul 15-18.

On Jun 24, NDRC issued measures to promote and develop new consumption drivers.

Beijing became the last tier-1 city to relax home buying requirements for down payment and mortgages.

Industrial profits and revenue stayed roughly flat sequentially, and augmented fiscal deficit widened amid faster government bond issuance in May.

Inbound FDI fell for 12 consecutive months, with ytd amount dropping 28% as of May.

In short, anybody with a brain is fleeing the wreckage of the Chinese economy.

This does not include Albo’s Australia.

We will find out our next instalment of property yawnulus mid-month so a dead cat bounce for iron ore has few weeks of grace.

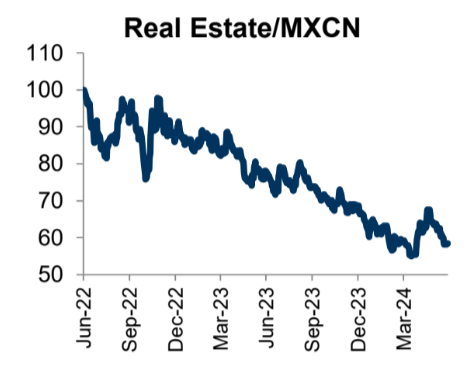

Judging by the state of Chinese property stocks, it isn’t going to move the needle.

This week we also get the PMIs. Goldman again:

We expect the NBS manufacturing PMI to be49.8 in June, vs 49.5 in May.

High frequency indicators such as steel demand improved slightly in sequential terms, and the decline of commodity prices might help boost new orders in June.

Post-Covid residual seasonality implies an uptickin the NBS manufacturing PMI from May to June.

On the flip side, our commodity equity research team’s channel check suggests a softened demand for most downstream sectors in June.

Onwards and downwards!