HSBC with a report that closely mirrors my own views on the AUD.

Keywords including “peak US exceptionalism”, “exhausted Fed repricing”, “peak China pessimism”, “commodity upcycle”, and “a higher-for-longer RBA” were commonly featured as arguments during AUD-USD’s recent rise.

We think this is only partially correct.

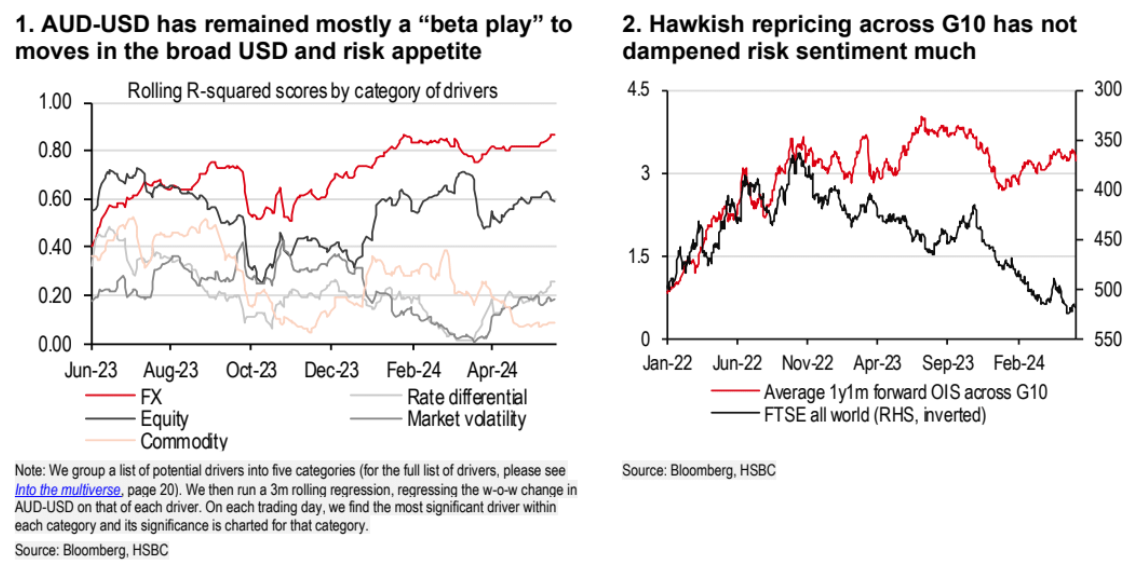

Being highly dependent on external drivers, AUD-USD has remained mostly a “beta play” to moves in the broad USD and risk appetite (Chart 1).

Hawkish repricing among most major central banks has been backed by positive growth surprises and upgrades, therefore not dampening risk sentiment (Chart 2).

Fed speakers have guided markets towards a narrow range of end-2024 OIS outcome, limiting further hawkish repricing and reducing rates volatility.

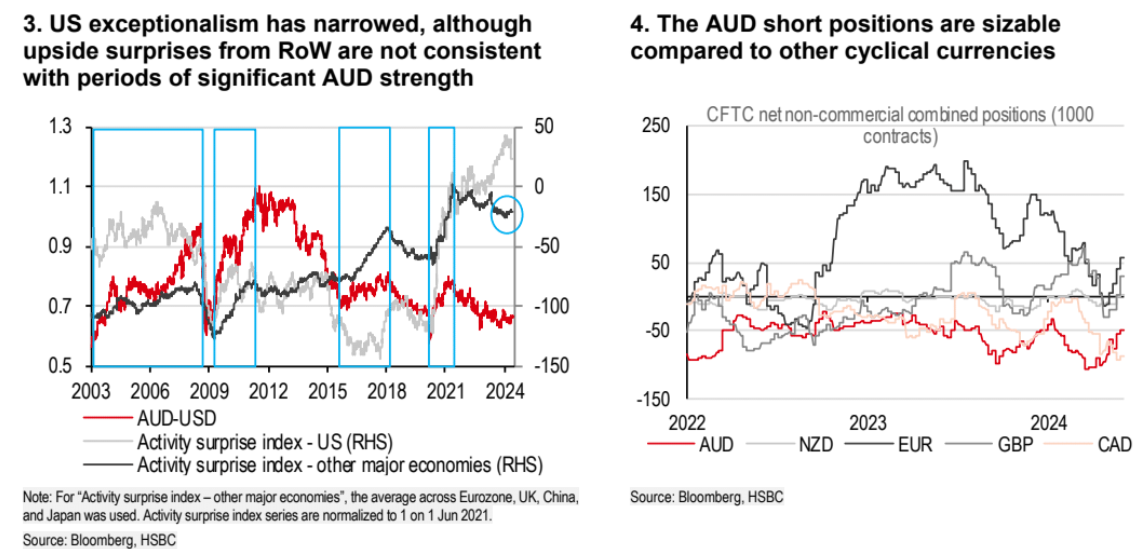

US exceptionalism has narrowed, although upside surprises from the rest of the world are not yet consistent with periods of significant AUD strength (Chart 3).

Should these macro tailwinds extend, AUD-USD upside could be a favoured expression, given sizable short positions built compared to other cyclical currencies (Chart 4).

However, we are not yet convinced that AUD-specific drivers (e.g. exports to China, link to commodity prices, rate differentials, etc…) will turn sustainably supportive.

Without their help, there may only be modest AUD strength this year at best and AUD-USD may be stuck being the “beta play”.

Stuck like this with the outlook of a severely strained US election is why I see AUD going nowhere this year.