DXY is firming again:

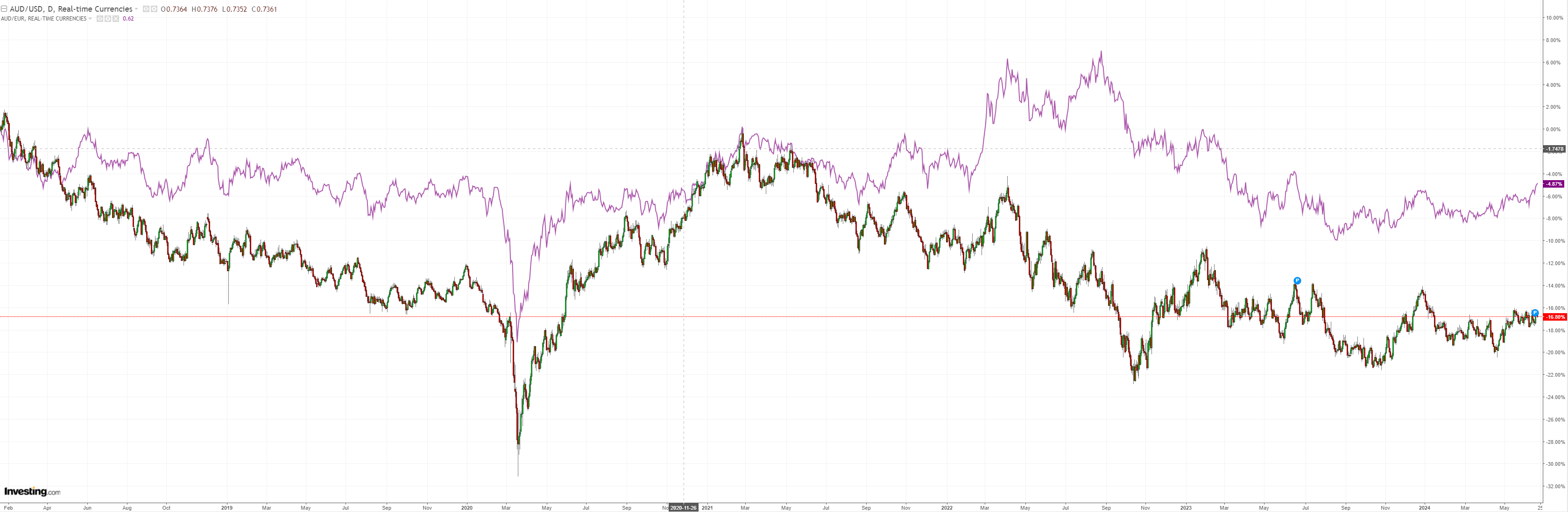

AUD is stuck in the range. Up against EUR:

North Asia is woeful:

CTAs are pressing another oil head fake:

Driving metals:

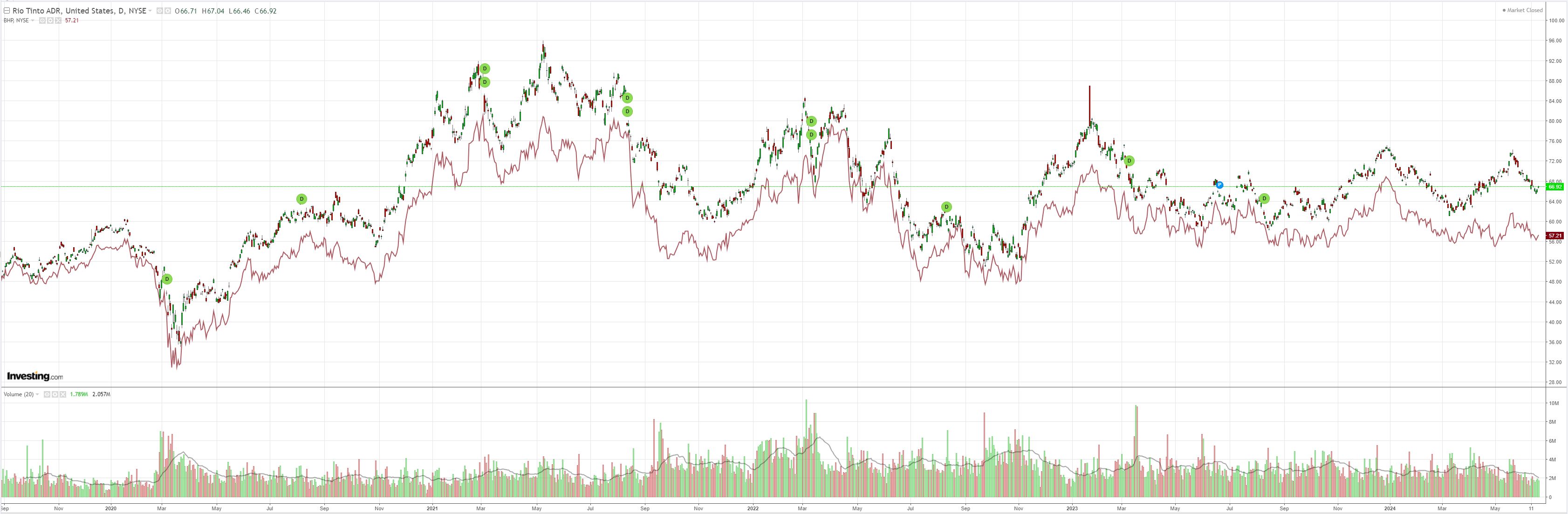

And miners:

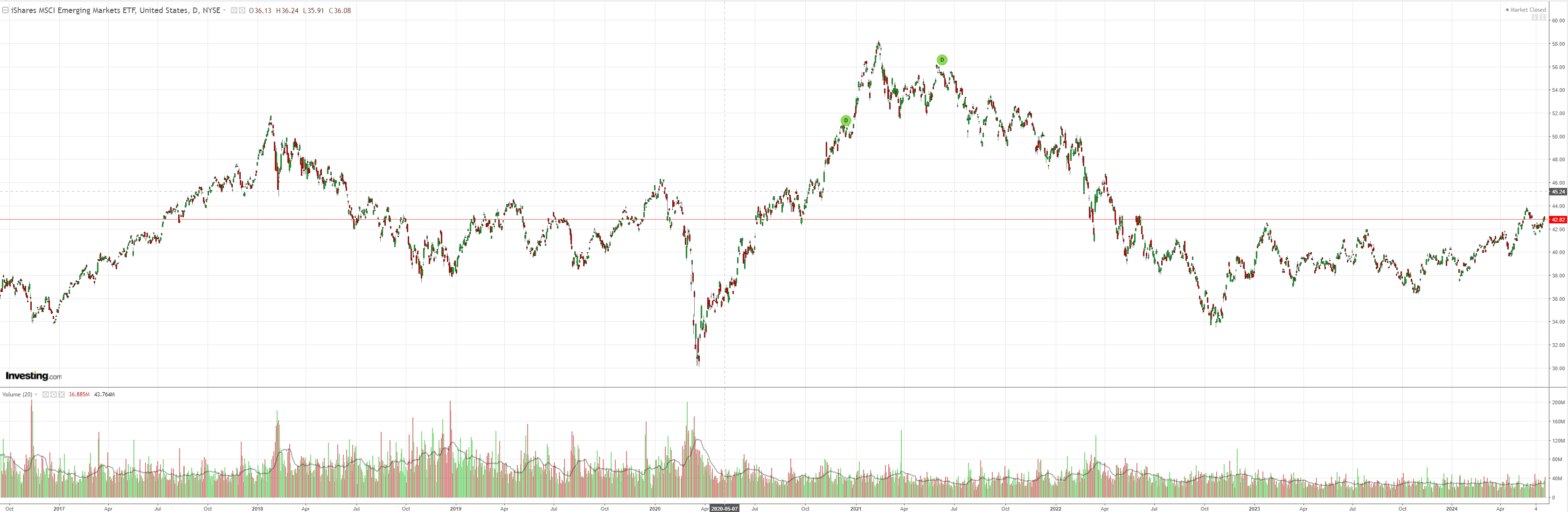

EM has held support:

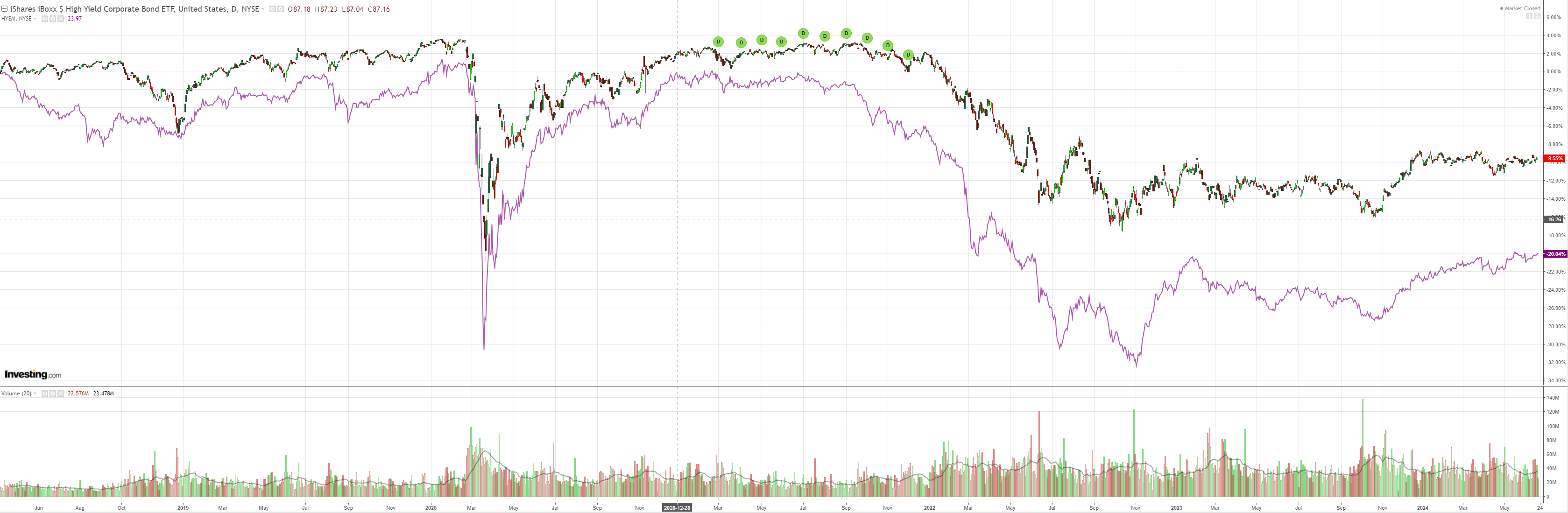

Junk is threatening breakout:

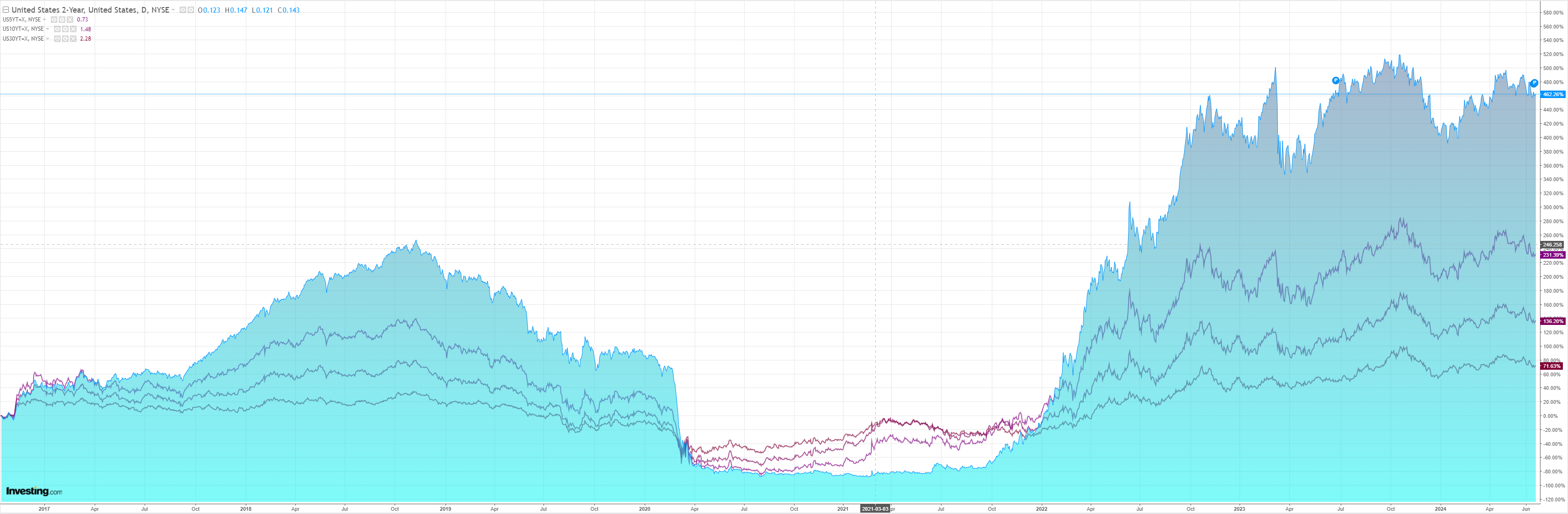

The yield curve steepened:

Stocks reversed:

The AUD is being hit from all sides by forex:

- DXY is being driven by US exceptionalism, oil and the H2 election.

- EUR is being hit by France.

- CNY and JPY are on the highway to hell as compete for exports amid failing Chinese growth.

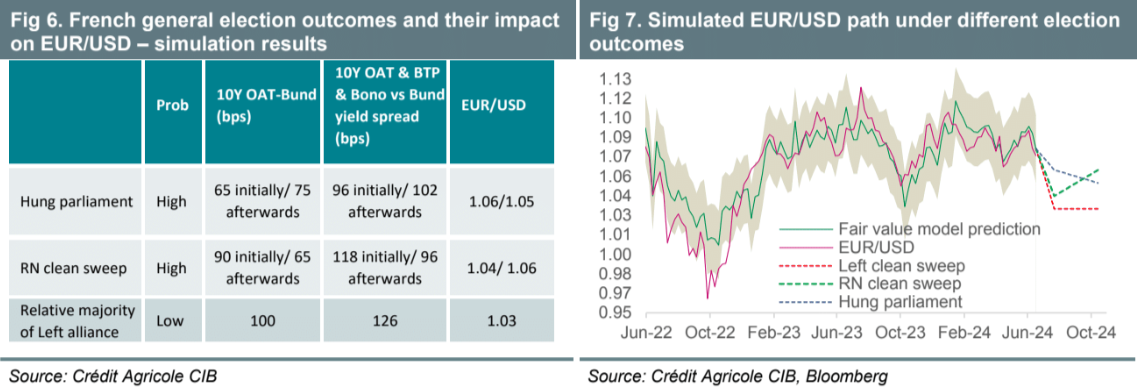

Of these, the most pressing is EUR. Credit Agricole:

Our analysis suggested that a GDP-weighted average of OAT, BTP and Bono yield spread over Bunds has a better explanatory power than OAT-Bund yield spread alone(Figure 5).

We therefore simulate the EUR-impact using our FASTFX model’s EUR/USD fair value estimate derived using the forecastof the GDP-weighted average of OAT, BTP and Bono yield spread over Bunds.

We further consider two time periods for the impact analysis–immediately after the vote; and the start of the fiscal budget talks in Q224.

Our results (also shown in Figures 6 and7)suggest that:

1.The most negative impact on EUR/USD would be a relative majority of the left-wing NPF alliance

2.A clean sweep for NationalRally (RN) could weigh on the EUR initially before a cautious recovery

3.A hung parliament could weigh on EUR/USD over time

Not much positivity there for EUR or AUD.

On the upside for AUD, Albo’s new energy vandalism is hurting the interest rate outlook. But given the bill rebates that are coming, it will not hit in the near term.

AUD pressured within the range, I suggest.