Below are CBA’s and Westpac’s takes on the federal budget and its impact on the economy:

CBA’s Take:

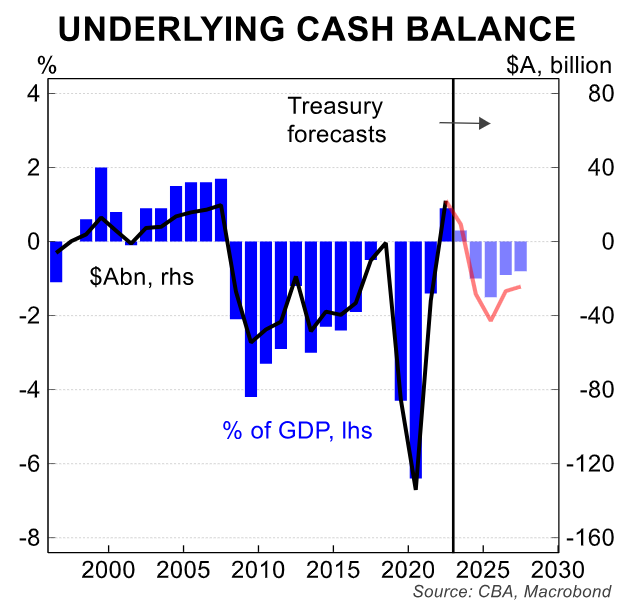

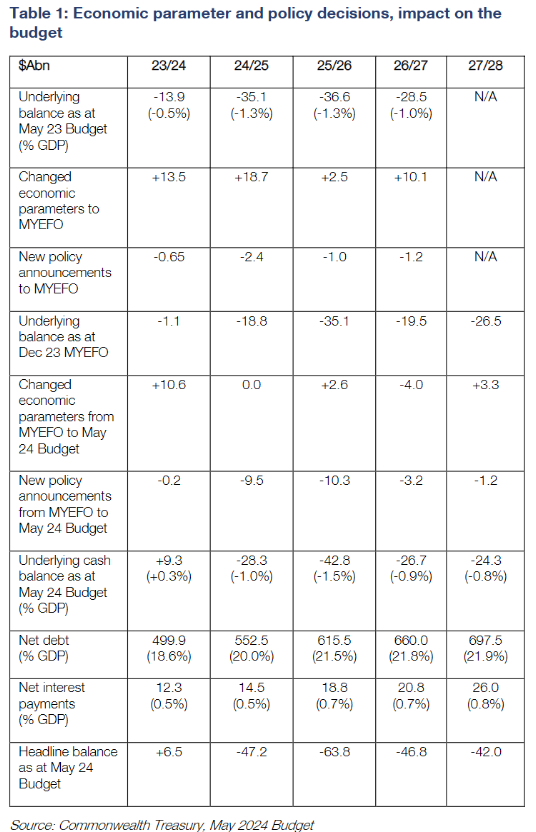

- For 2023/24 the Budget is now expected to be in surplus by $A9.3bn (0.3% of GDP), up from the December 2023 MYEFO estimate of a deficit of -$A1.1bn (0.0% of GDP)and the original estimate of a deficit of -$A13.9bn (-0.5% of GDP).

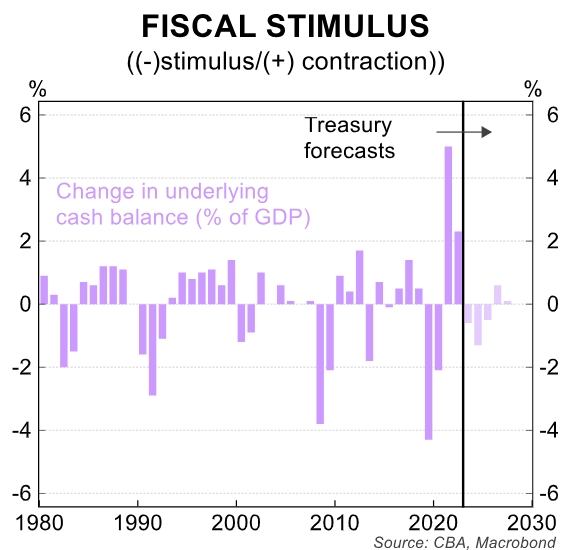

- This will be the second year in a row of budget surplus for Australia –a good outcome and a significant contrast to the ongoing large deficits in most other major economies.

- But the 2024/25 Budget estimates a deficit for the year of -$A28.3bn(-1.0% of GDP). This is a deterioration from the MYEFO estimate of a deficit of $A18.8bn (-0.6% of GDP) and is much larger than our expectation of a deficit of just $A5bn (-0.2% of GDP).All of this deterioration comes from policy decisions.

- Major policies announced in the Budget include: the previously announced income tax cuts, electricity relief for all households, increased rental assistance, lower cost of medicines, a lowering of tertiary student debt, funding to help build extra housing and the implementation of the Future Made in Australia strategy.

- Disappointingly, the budget deficits out to 2027/28 are now projected to range from 0.8% to 1.5% of GDP and are larger than the MYEFO estimates. These deficit estimates are larger than ideal for an economy that is expected to see a high level of investment for several years coming from both the private sector and Federal and state governments.

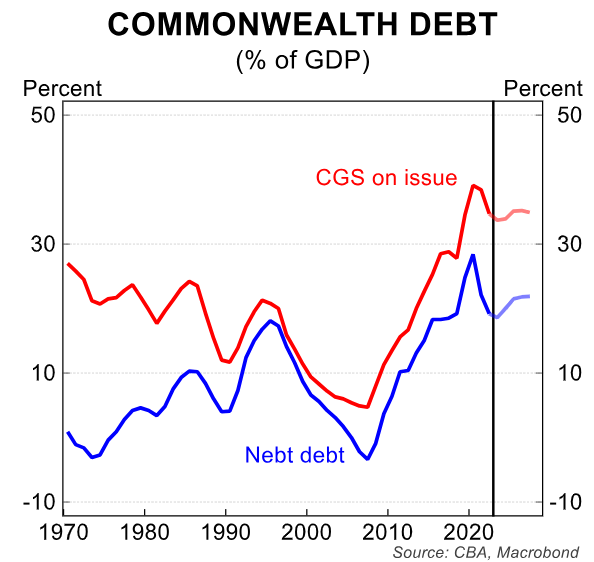

- From an estimated 18.6% of GDP as at June 2024, net debt is now projected to rise to 21.9% of GDP by June 2028. While this net debt level remains low by global standards, the increasing trend is not a welcome development.

- In terms of the government’s economic forecasts, extensive cost-of-living relief underpins inflation forecasts that are materially below the RBA’s recent headline inflation estimates. More broadly, the economic forecasts indicate an ongoing period of subdued economic growth before some ‘circuit breakers’ arrive from H2 2024.

- The turnaround from a surplus of 0.3% of GDP in 2023/24 to a deficit of -1.0% of GDP in 2024/25 represents a larger-than-expected easing of fiscal policy.

- While headline inflation is still forecast to be 2.75% in 2024/25, the RBA is likely to remain cautious. We had flagged that fiscal policy was one of the risks that could delay our base case that monetary policy easing would start in November this year. This risk is now more real

Overview –On the edge of the narrow path:

The Australian economy is on a narrow path. Economic growth is slowing under the weight of higher interest rates, as the RBA is focused on returning inflation to the 2%-3% target range -without doing too much damage to the labour market.

In this process, a significant share of the Australian community is enduring a large rise in the cost of living, while some households are doing very well.

This is the context for the 2024/25 Budget and the environment in which the government has decided to ease fiscal policy in the year ahead. Noticeable, policy changes will add $A9.5bn to the expected budget deficit in 2024/25.

For 2023/24 (i.e. the year just ending) the government now projects a surplus of $A9.3bn (0.3% of GDP).

This is well up on the original estimate, in May 2023, of a deficit of -$A13.9bn (-0.5% of GDP) and better than the December 2023 Mid-Year Economic & Fiscal Outlook (MYEFO) update of -$A1.1bn (0% of GDP).

This will be the second year in a row of a budget surplus for Australia –a good outcome and a sharp contrast to the ongoing budget deficits in most other major economies.

However, for 2024/25, the Budget is now projected to be in deficit by -$A28.3bn (-1.0% of GDP), an improvement from the previous budget estimate of a -$A35.1bn (-1.3% of GDP), but a noticeable deterioration from the MYEFO estimate of -$A18.8bn (-0.7% of GDP).

Our estimate was for a deficit of -$A5bn (-0.2% of GDP).As detailed in Table 1, this deterioration in the budget bottom-line for 2024/25 relative to the December 2023 MYEFO estimates has come all from policy decisions, ie. $A9.5bn, not economic parameter changes.

In our view, the turnaround from a surplus of 0.3% of GDP in 2023/24 to a deficit of -1.0% of GDP in 2024/25 represents a larger-than-expected easing of fiscal policy. While headline inflation is still forecast to be 2.75% in 2024/25 due to specific policy measures (see below for details), the RBA is likely to remain cautious.

We had flagged that fiscal policy was one of the risks to our base case that monetary policy easing would start in November this year and that the neutral cash rate of close to 3% would be reached by the end of 2025.

The risk is now more real that the first interest rate cut could be delayed and that the neutral cash rate is higher than we currently estimate due to the expansionary fiscal setting and the high level of investment in the economy.

As the table above also shows, the budget deficits out to 2027/28 are all forecast to be larger than previously estimated at $A42.8bn (-1.5% of GDP for 2025/26, $A26.7bn (-0.9% of GDP) for 2026/27 and $A24.3bn (-0.8% of GDP) for 2027/28.

In our view, deficits in the range of -0.8% to -1.5% of GDP over coming years are larger than would be ideal in an economy that is likely to see ongoing large investment requirements from the private sector and the Federal and state governments.

The large budget deficits projected in the out years (see table above), which will have a direct impact on the required borrowing for the government and raise net debt in the years ahead.

From an estimated $A499.9bn (18.6% of GDP) as at June 2024, net debt is now expected to grow to $A697.5bn (21.9% of GDP) as at June 2028.

Economic forecasts:

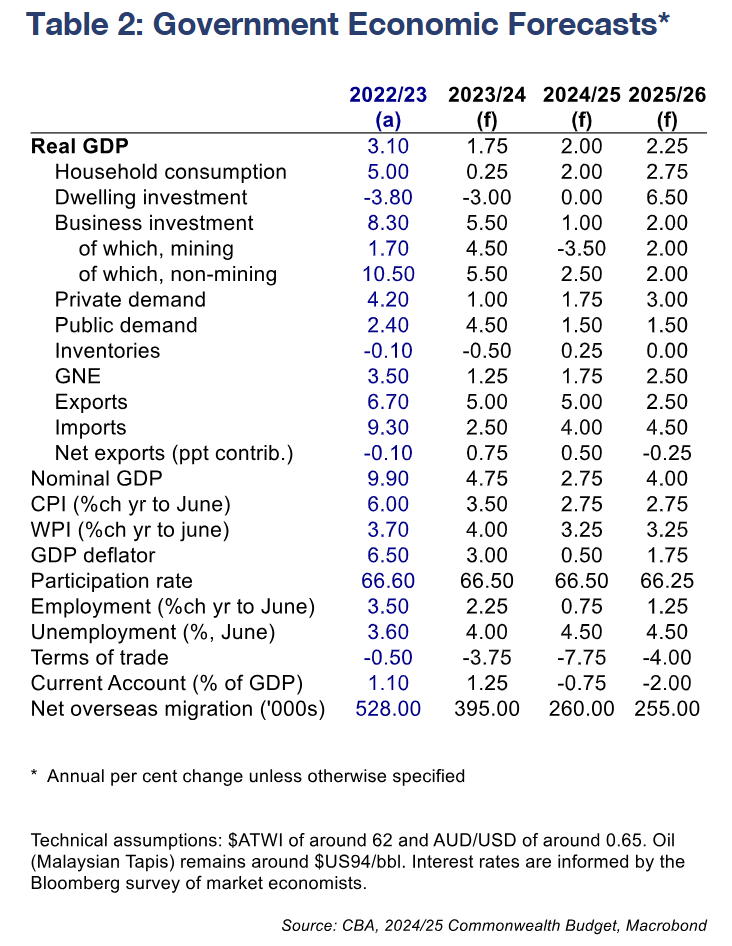

The government’s expectations for the path of the economy over coming years are detailed in the economic forecasts contained in the Budget.

As is the custom, economic forecasts are provided for the Budget year and the subsequent financial year. Economic projections are included for the following two years.

Here we focus on the nearer term forecasts rather than the government’s projections in the outer years.

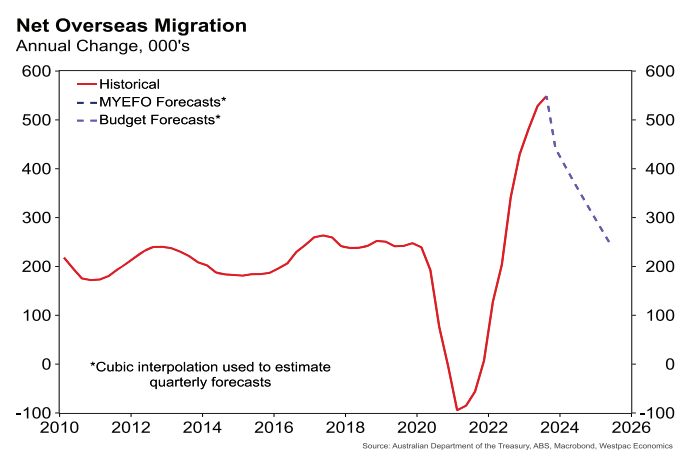

Population growth is a key assumption in the Budget, which is in turn driven by net overseas migration (NOM).

In 2022/23, migration was much stronger than expected (+128k), and this has flowed on to an upgrade for NOM in 2023/24 of +80k (~0.3% of population) relative to last year’s budget.

Stronger NOM this financial year boosts GDP and employment forecasts, all else equal.

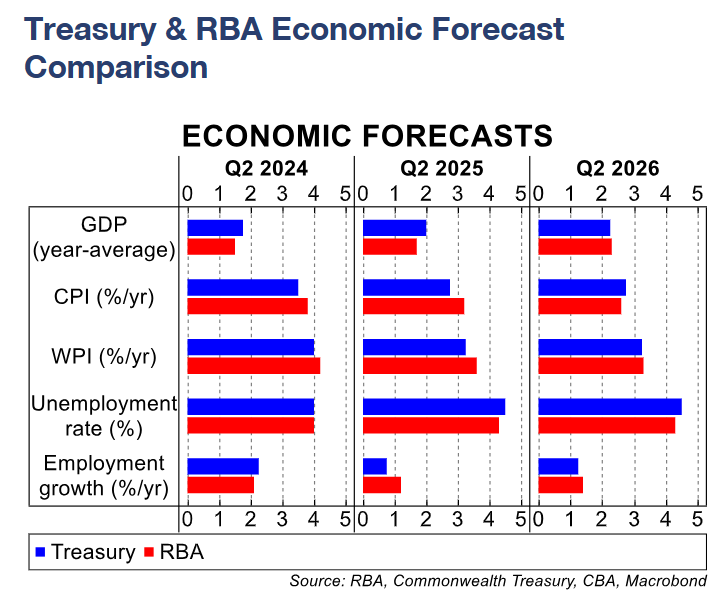

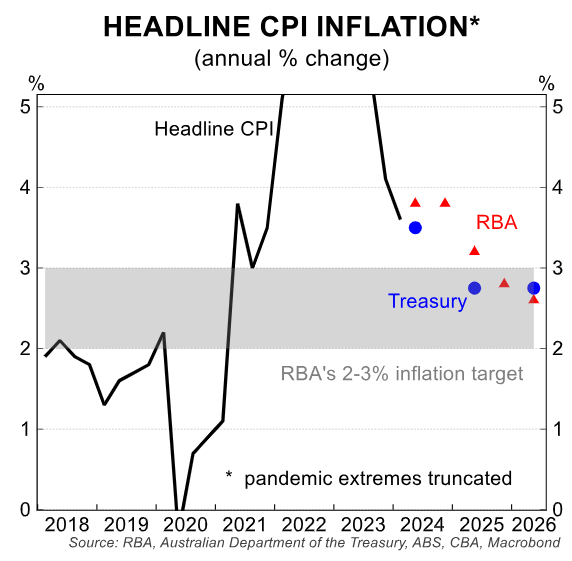

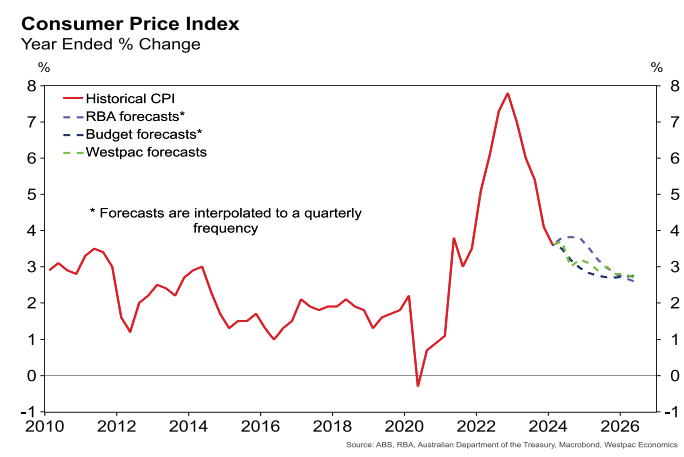

Headline inflation forecasts in the Budget are notably lower than the RBA’s latest forecasts in the May Statement on Monetary Policy. Specifically, headline inflation is forecast by the government to be 3.5%/yr in Q2 24 and 2.75% in Q2 25.

The Q2 24 CPI forecast is a quarter point lower than at MYEFO and a quarter point higher than expected at last year’s Budget.

The Q2 25 CPI forecast has not been changed. Inflation in Q2 26 remains at 2.75%. Note that the government does not forecast trimmed mean CPI inflation.

The RBA is forecasting inflation at 3.8%/yr in Q2 24, 3.2%/yr in Q2 25 and 2.6%/yr in Q2 26. The discrepancy in Treasury and RBA forecasts for the headline CPI rate had been flagged earlier by the Treasurer; the Treasury forecasts incorporate elements of the Budget that the RBA’s forecasts do not.

This includes energy bill relief and an increase in Commonwealth Rent Assistance. The government estimates that these two measures reduce measured inflation by 0.5ppts in 2024/25.

While the government only provides forecasts for the June quarters, i.e. end of financial year, the Budget notes that headline inflation “could” be back within the RBA’s 2%-3% inflation target by end 2024, three quarters earlier than the RBA’s forecasts.

That means there is ~0.8ppt difference between what the two official forecasting families are expecting for the Q4 2024 inflation figure, given the RBA expects a 3.8%/yr outturn.

CBA’s forecasts for inflation are more closely aligned to the government’s numbers. We expect headline inflation to be 3.6%/yr in Q2 24, 3.2% in Q4 24 and to fall to 2.8%/yr by Q2 25.

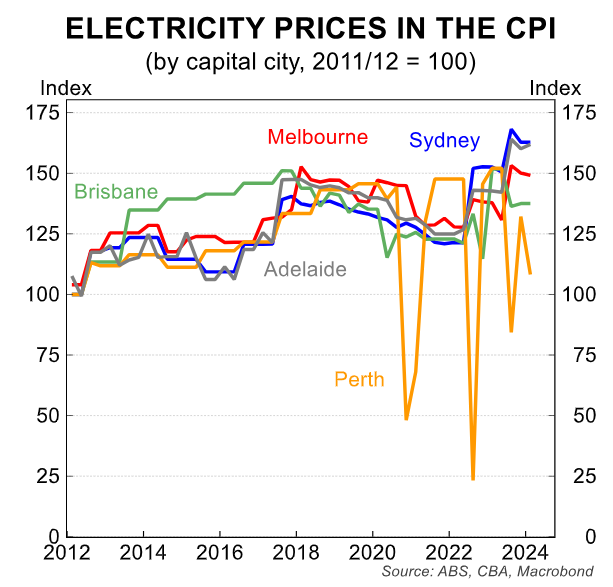

Measured CPI inflation could be even lower if the recently announced electricity rebates from the Qld and WA state governments are incorporated. The Qld government notes its $A1,000 rebate will mean a majority of Queenslanders will see their bills fully offset until 2025.

A back-of-the-envelope calculation suggests a ~0.2ppt knock off headline CPI in Q3 24, and a bit less in Q4 24 (electricity accounts for 2.4% of the total CPI basket, and Brisbane contributes 8.8% of the electricity share).

Subsidies to the household sector via these rebates will mean more disposable income and spending power than otherwise. And there is an argument that this will add to demand in the economy, thereby exacerbating current inflationary pressures.

However, it will mean vulnerable households already facing big increases in their essential costs will see some relief.

The boost to demand too may be more muted than in other circumstances; households with mortgages are currently paying down their debt faster than before the pandemic, and faster than expected by the RBA.

This has been spurred by the high interest rate environment, which has increased the opportunity cost of not saving. It has also contributed to consumption growth being very weak.

Another factor to consider is that a lower headline CPI means that wages, costs and prices that are indexed to it will also be lower, helping contain inflation and wage expectations.

In any case, what is certain is that these rebates will likely add to more volatility in the monthly CPI figures –the timing of these rebates and the subsequent unwinding will move the monthly inflation figures around–making a read of the underlying inflation pulse more difficult.

Turning to wages growth, the government expects the Wage Price Index (WPI) to have already peaked. Annual growth in WPI is expected to be 4.0% in Q2 24, below its Q4 23 pace of 4.2%, and moderate further to 3.25% by Q2 25.

That’s similar to CBA’s forecasts for wages growth, but below the RBA’s.

The RBA expects annual wages growth at 4.2% in Q2 24, with the pace of wages growth moderating to 3.6% in Q2 25. Q1 24 wages data will be released on Wednesday, where the RBA, the consensus of market economists –CBA included –expect annual growth of 4.2%.

The Fair Work Commission decision on the minimum and award wage, to be handed down before 30 June 2024, will be important to the wages outlook in 2024/25.

With inflation having moderated substantially from its end 2022 highs, the annual wage decision should come in well below last year’s 5.75%.

The government’s forecast for WPI includes an assumption that the FWC delivers an outline broadly in line with inflation.

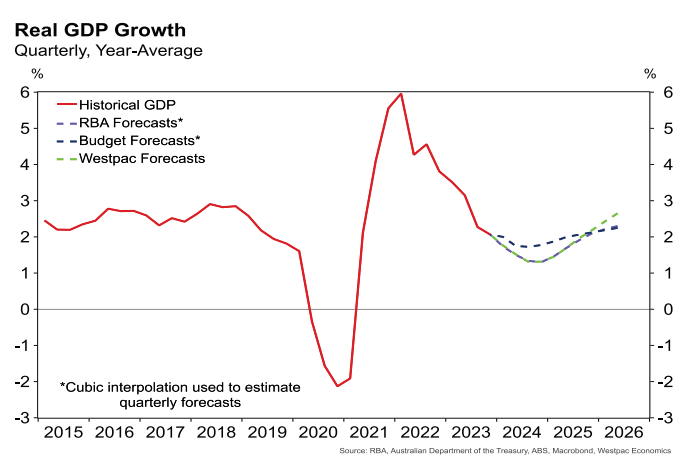

On the real activity side, there are smaller differences between the government and the RBA forecasts. GDP growth is expected to moderate to 1.75% in 2023/24, before lifting a little to 2.0% in 2024/25 and 2.25% in 2025/26.

These figures are a touch higher than the RBA’s: 0.25ppts this financial year and 0.3ppts in 2024/25.

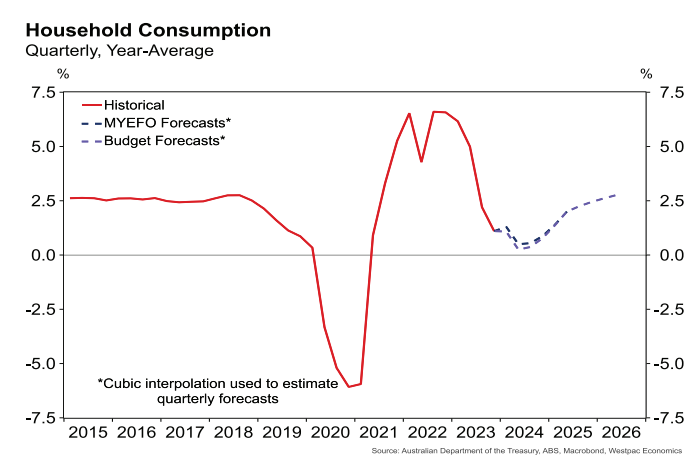

It appears the stronger growth outcomes in part reflect a stronger household consumption profile embedded in the government’s forecasts.

CBA expects annual average GDP growth more in line with the RBA’s estimates: we expect growth for 2023/24 to be 1.5%, rising to 1.8% for 2024/25.

Despite slightly higher GDP growth expected, the government’s forecasts have a slightly faster slowing in the labour market relative to the RBA. Employment growth is forecast to be 2.25% over the year to the Q2 24 and just 0.75% the following year.

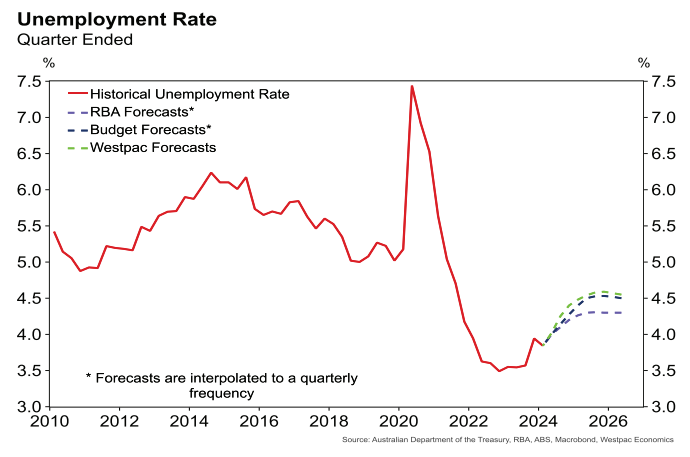

The unemployment rate is expected to edge up to 4.5% by June 2025 and remain there the next year.

Overall, more expansive cost-of-living relief underpins inflation forecasts that are materially below the RBA’s. The measures announced in the Budget account for much of this difference.

The government’s forecasts for real GDP growth does look optimistic relative to ours. But we agree with the government’s expectations around the labour market and wages growth.

Westpac’s Take:

- The government is walking a fine line on spending to keep the economy on a narrow path. The cost-of-living squeeze is real, but the government does not want to stoke inflation further. Many measures have been designed to lower reported inflation, including expanded energy bill relief, greater rent assistance and cheaper medicines. The government’s forecast of headline inflation reaching 2.75% by the end of 2024–25 is a little below our own but it is entirely plausible. These changes should not materially shift the timing of RBA decisions on rate cuts.

- But new spending – including on housing, infrastructure and the care sector – adds additional stimulus. Most of the net new spending (close to $20bn) is frontloaded into 2024–25 and 2025–26.

- After recording a second consecutive surplus in 2023–24, the budget swings into a bigger deficit than we expected in 2024–25. Some of this stems from the new spending and slower nominal growth. As in past years, though, conservative assumptions about commodity prices and bond yields also contribute. One cannot rule out another positive surprise in the 2024–25 final outcome in 12 months’ time. And at 1% of GDP, the projected deficit for 2024–25 is notably smaller than those in many peer economies.

An Even Softer Landing:

Inflation and Wages:

A central source of discussion in tonight’s forecasts is the trajectory of inflation. The Federal Government has cut its near-term inflation forecasts.

In 2023-24, the Government has lowered its inflation forecasts to 3.5%, from 3.75% in the MYEFO. The new policy announcements around subsidies for housing and energy relief to households and small businesses are expected to take ½% off headline inflation in 2024-25.

However, the net impact on inflation is difficult to ascertain. The direct effect is to soften inflation via the associated subsidies and lower indexation of some other prices the following year. It may also help contain inflation expectations.

But there’s an indirect effect; the relief provided to households may spill over into extra spending that could see inflation take longer to moderate.

For 2023-24, the RBA forecasts CPI growth of 3.8%, which will not include the impact of subsidies announced on budget night.

Our forecast, taking into account the subsidies, which were largely as anticipated, is higher than the Government’s at 3.7%.

In 2024-25, the Federal Government expects the rate of growth in the CPI to fall to 2.75%, within the RBA’s inflation target band, which if materialised would allow for rate cuts from the RBA.

The government’s forecast contrasts with the RBA’s higher forecast of 3.2% in 2024-25. Our forecast adjusting for subsidies is between these estimates at 2.9%.

Forecasts for the wage price index remain unchanged and appear reasonable at 4.0% for 2023-24 and 3.25% for 2024-25 and 3.25% for 2025-26.

Optimistic consumer rebound:

Real disposable income is forecast to grow by 3.5% in 2024–25, driven by growth in labour incomes, the cost-of-living tax cuts, lower interest rates and a smaller drag on real incomes from inflation compared to recent years.

If realised, this would be the fastest rate in over a decade (excluding the COVID period), although this is mostly clawing back the heavy decline in 2022 and 2023.

The forecasts look a little optimistic given the soft profile for employment growth.

Turning to GDP and the Federal Government is forecasting softer growth in 2024-25. Real GDP is expected to grow by 1.8%, similar to the MYEFO forecast, but real GDP growth in 2024-25 has been cut from 2.3% previously to 2.0%. It recovers modestly to 2.3% in 2025-26.

Within the GDP mix, there’s an expectation of a sharp turnaround in household consumption from 0.3% growth in 2023-24 to 2.0% in 2024-25.

We expect the consumer recovery to follow a slower, more gradual path, growth only lifting to 1.3% in 2024-25. The Government notes this as a key uncertainty for the domestic outlook.

Investment and public demand:

Business investment and public final demand have also been upgraded, business investment noticeably so. If realised, the Government’s business investment forecasts imply the longest sustained upswing in business investment since the mining boom.

We actually see some upside to this profile, with an upturn in business investment expected to become a more prominent driver of growth in 2025-26.

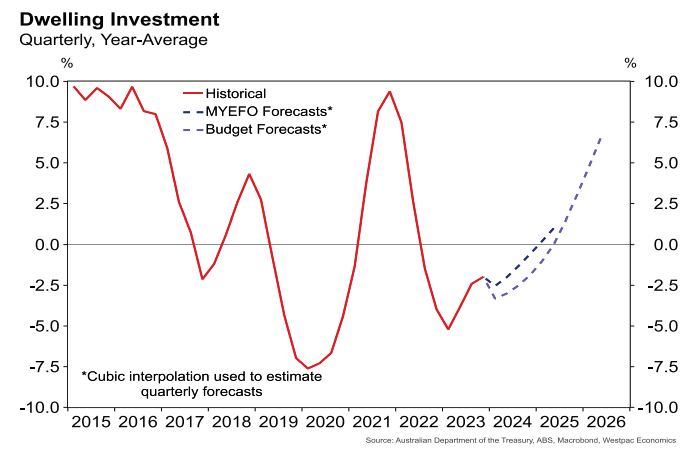

Dwelling investment forecasts were marked down in the near-term reflecting ongoing challenges in boosting housing supply.

However, the Government is backing the impact of its housing policies, forecasting dwelling investment to surge 6.5% in 2025-26 compared to a flat reading in 2024-25.

Nominal GDP growth has been revised up by 0.5 percentage points in 2023-24 and again in 2024-25, leaving nominal growth at 4.75% and 2.75%, respectively.

And the declines in the terms of trade over 2023-24 to 2025-26 are smaller than previously anticipated.

Labor market and population:

The Budget forecasts mark to market the near-term strength of the labour market reducing the June 2024 unemployment rate forecast to 4.0%.

However, the expected terminal unemployment rate was left unchanged at 4.5% in both 2024-25 and 2025-26, despite a slight downgrade to economic growth.

The resilience of the labour market is perhaps justified by the ambitious projected slowdown in NOM, which will reduce the labour supply pulse.

Budget forecasts have NOM drying up to 395k in 2023-24. The latest population statistics have NOM running at 548k over the year to the September quarter of 2023.

In 2024-25 and 2025-26 NOM is expected to slow to 260k and 255k, respectively.

Risks:

Pulling this all together, the budget’s economic forecasts are not all that different to Westpac’s.

We are slightly more pessimistic on growth near term and around the pace of the consumer and housing recoveries, but more positive on growth in 2025-26 with these and an upturn in business investment expected to provide more momentum.

The budget’s domestic forecasts are also more positive than Westpac’s around consumer spending and dwelling investment, but this is balanced by a flatter profile for business investment and public demand.

For 2025-26, we are stronger on business investment.