The latest survey from independent economist Tony Alexander warns that Kiwis have become increasingly concerned about job insecurity, which is dampening their appetite for consumption.

Alexander also argues that the Reserve Bank’s aggressive monetary tightening is grinding households and businesses.

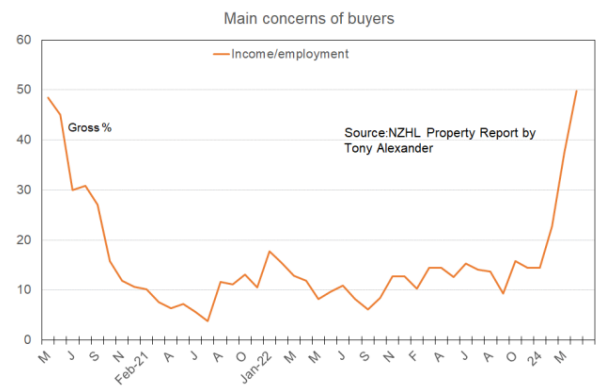

Buyers are more worried about their incomes than at any other time during the four year period of my monthly survey.

A net 50% of agents have reported that they are observing people express concern about their jobs etc. The average for this measure is 16% and only three months ago the reading was below this average at 14%.

This has been the key change in the economy since the start of the year. People, and especially young ones who have known nothing other than strong employment conditions, are shocked by the reports of layoffs…

Jobs growth essentially stopped in the middle of last year and the long-running ability of people to pick and choose amongst potential employers has ended.

The ability to tell a current boss or a potential new one how many days you plan to work from home is eroding.

The media have this past week noted the jump in youth unemployment and asked why this is happening.

Three reasons. First, this always happens when labour markets soften. The quantity of new young people entering the workforce continues to go up whereas this is largely not the case for most other age groups where people are already in the workforce. It’s a purely mathematical thing.

Second, it is possible that the expectations of young people seeking employment are less realistic than those of older folks. The older people may have mortgages to service, partners and children to support, and will be more willing to “eat bitterness” as the Chinese would say than young people with lower regular cash outgoing requirements and parents to fall back on.

Third, young people offer less experience and have less knowledge of what they are good at and what they enjoy than those who have been in work for a few years. They tend to be a riskier bet for businesses hiring staff than older folk…

Householders are certainly doing their part in drastically cutting back spending…

The longer they take the worse will be this endgame period for monetary policy tightening. Remember that it takes 18-24 months for tight policy to have its greatest impact on inflation…

But the initial rate rises were only 0.25% and we did not get the 0.75% jump and warning from the Reserve Bank of recession until November 2022.

In May 2024 we are only 18 months along from that shock tightening. Only now are we in the really intense period of the deepest grinding into cash flows and attitudes of the policy tightening.

ENDS

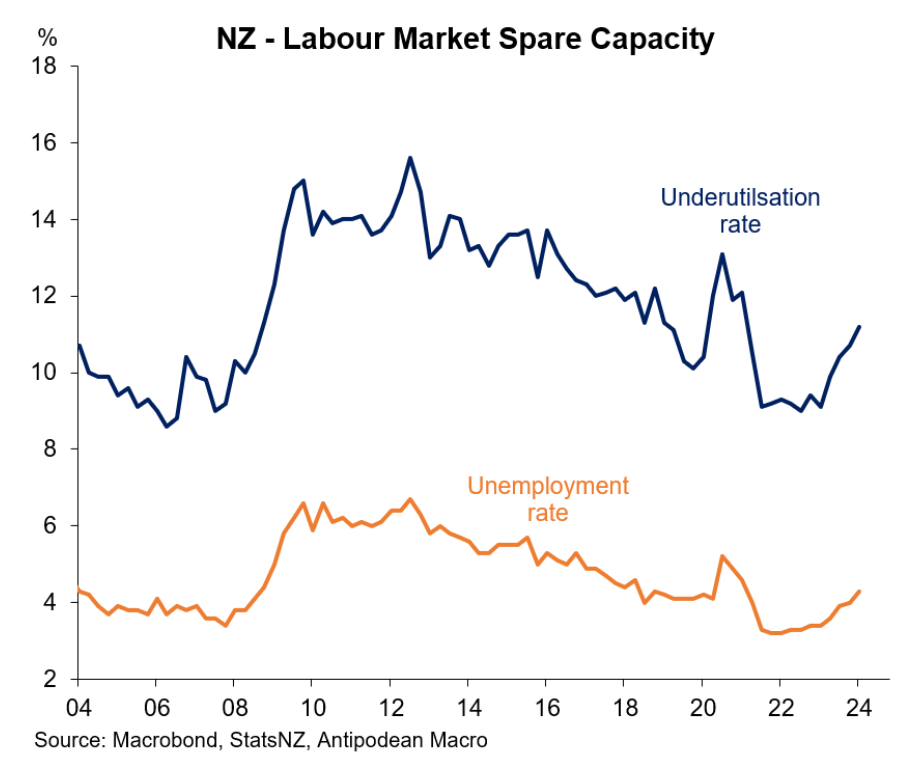

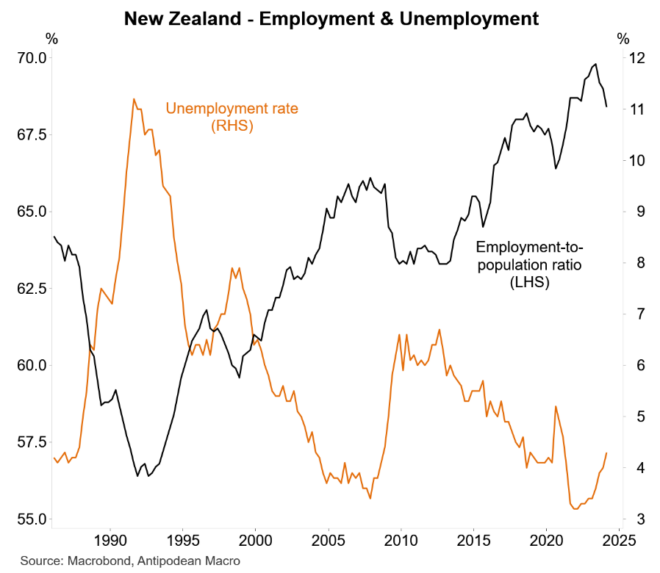

New Zealand’s unemployment and underemployment rates are rising, as illustrated below by Justin Fabo at Antipodean Macro:

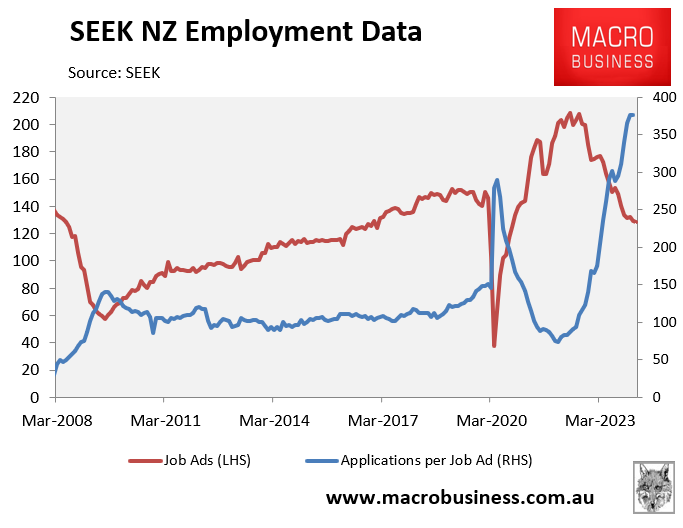

Seek’s latest employment report for New Zealand showed that the labour market is grappling with record immigration levels amid weakening job creation.

As shown above, Seek’s applications per job ads series has surged way above the pandemic peak, pointing to rising unemployment in the period ahead.

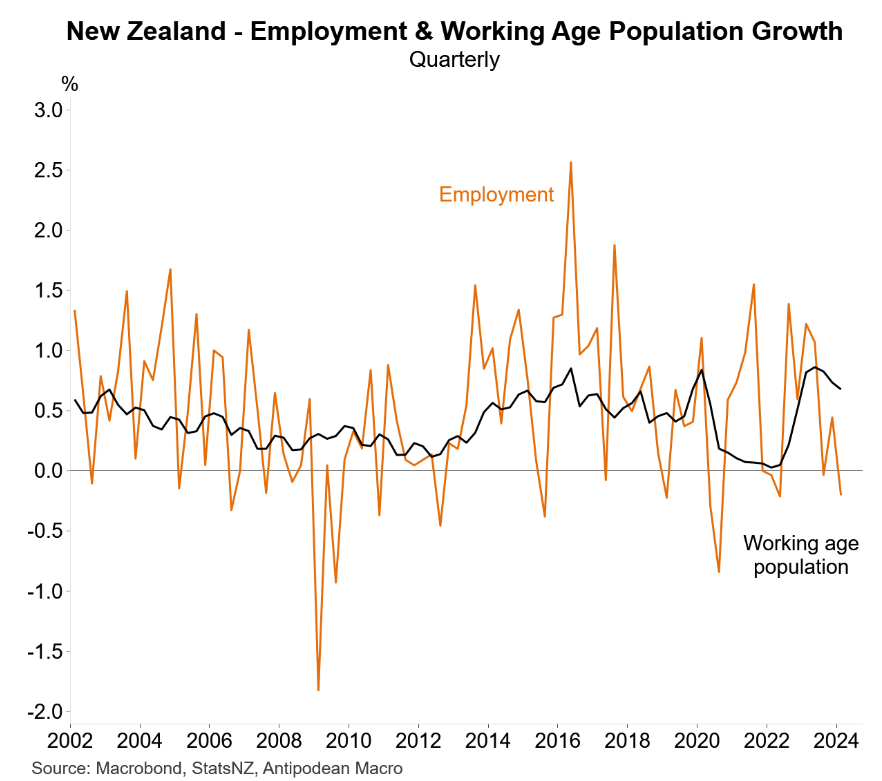

The jump in unemployment and underutilisation occurred alongside a 0.2% quarterly decline in employment and a large 0.6% fall in the employment-to-population ratio:

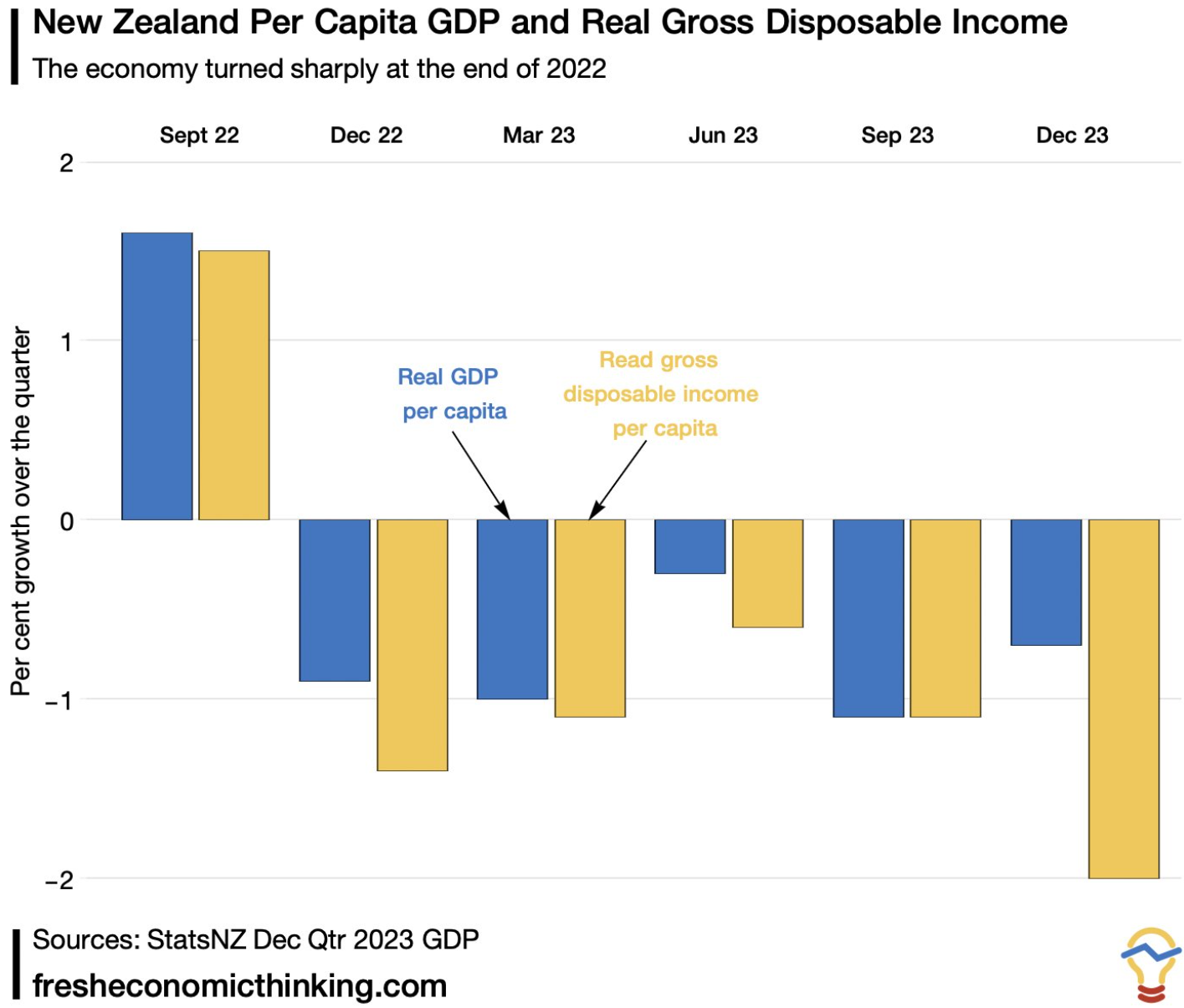

New Zealand’s economy is already suffering a technical recession and a very deep per capita recession:

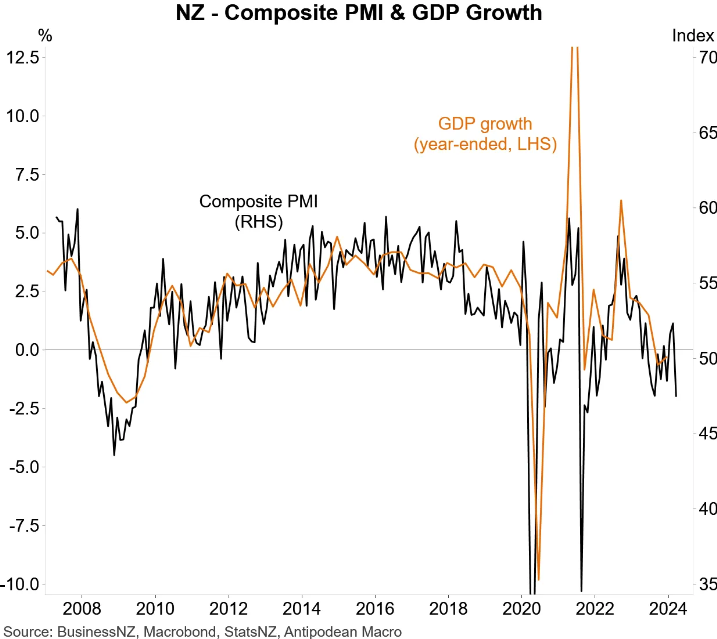

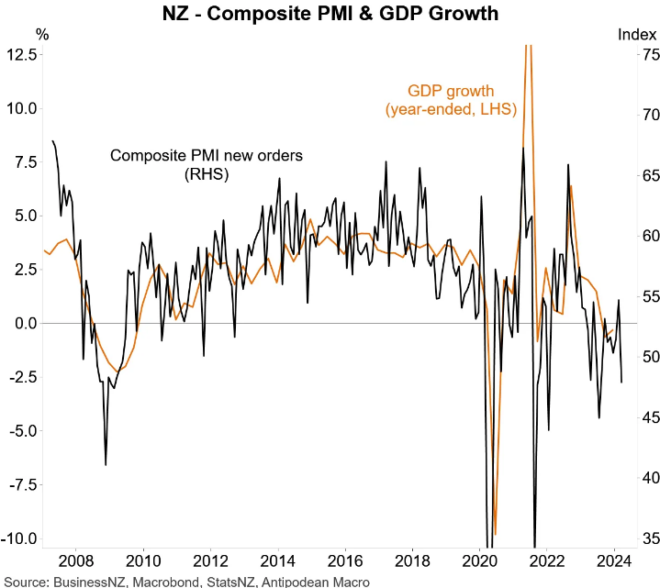

Forward indicators of activity have fallen post election, pointing to further declines in GDP growth over the first quarter of 2024:

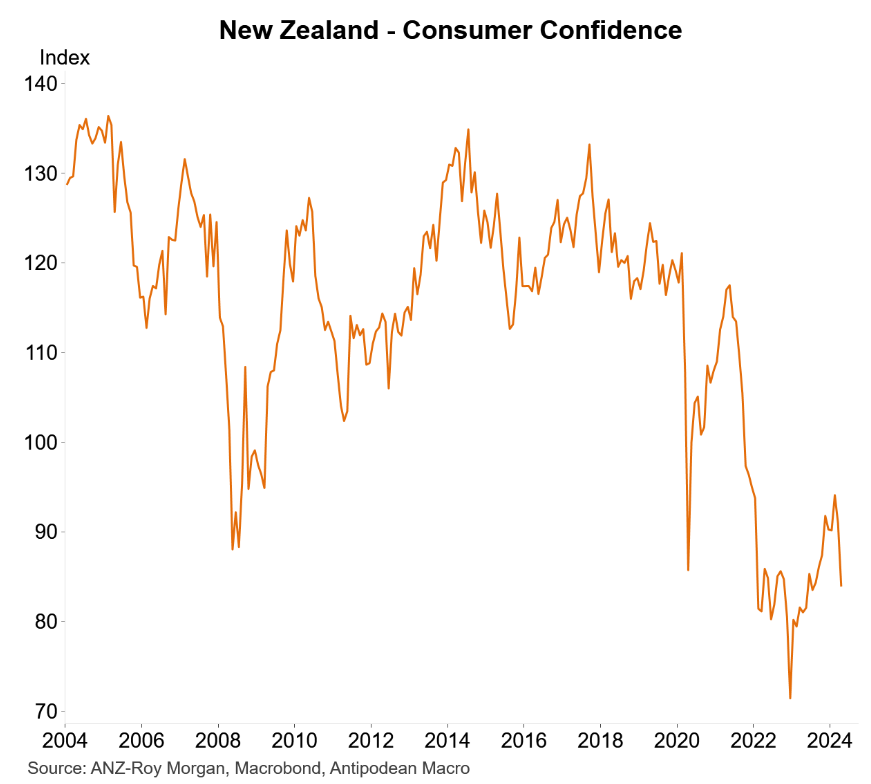

Consumer confidence has also soured following the obligatory post-election bounce that comes from a change of government:

One wonders how long the Reserve Bank can keep interest rates at these highly restrictive settings:

Given the souring employment and growth outlook, it seems only a matter of time before the Reserve Bank is forced to cut interest rates.