RBA won’t drive another nail through households

After last week’s higher-than-expected inflation numbers for the March quarter, talk shifted to the Reserve Bank of Australia (RBA) potentially hiking interest rates further this year.

Warren Hogan, the chief economic adviser for Judo Bank, led the hawkish sentiment by suggesting that the RBA could increase the official cash rate three times this year to 5.1%.

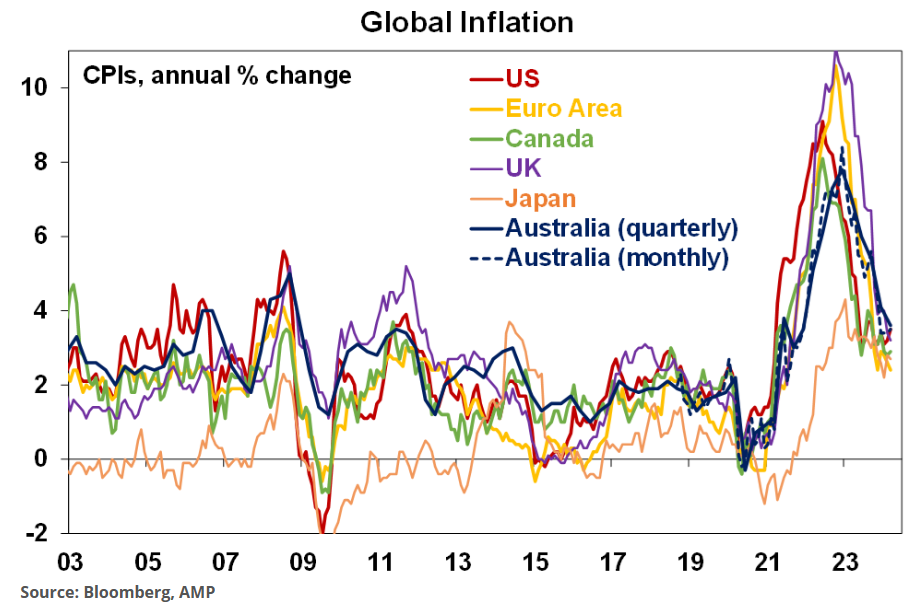

The hawkishness comes as annual Australian inflation continues to fall, down from a high in the December quarter 2022 of 7.8% year-on-year to 3.6% year-on-year in the March quarter 2024 and in line with the range of other major countries:

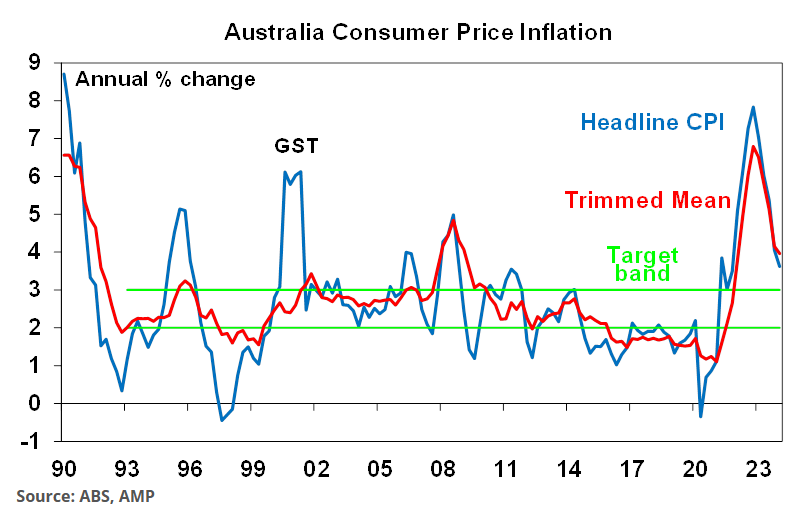

Nevertheless, CPI inflation came in higher than expected and remains higher than the RBA’s target, meaning that hopes for rate cuts have been delayed:

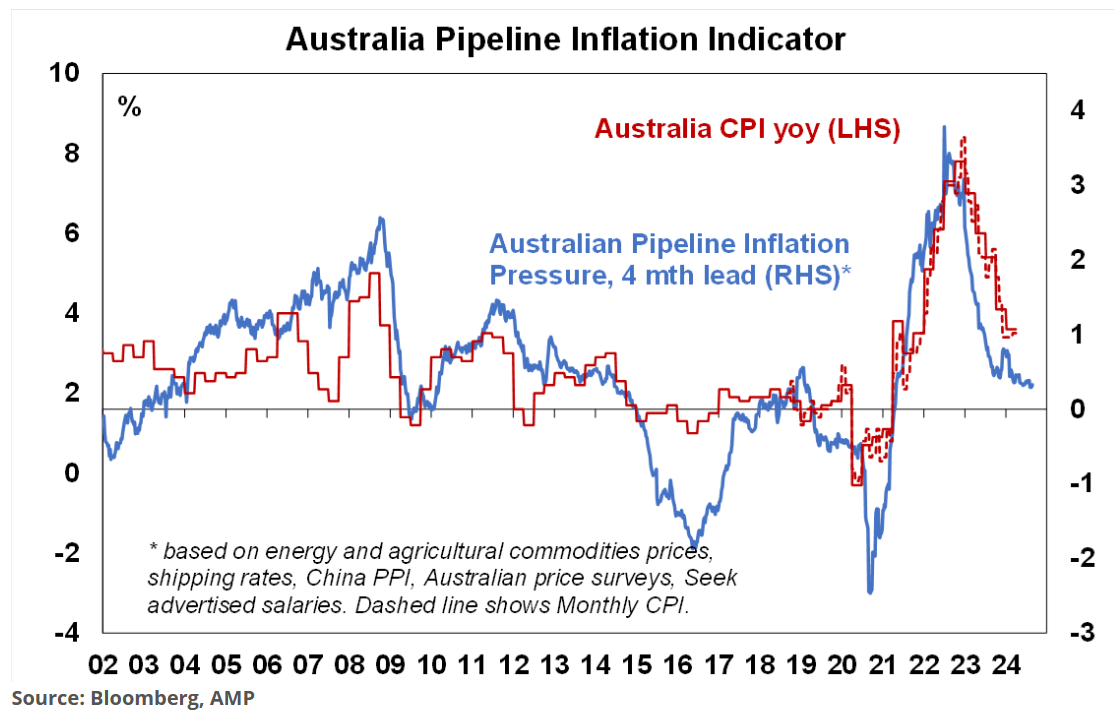

Still, AMP chief economist Shane Oliver notes that “pipeline Inflation Indicator is still pointing to lower inflation ahead and the March quarter inflation rate was boosted by seasonal increases for things like health and education so inflation should slow again in the current quarter much as it did in the December quarter”:

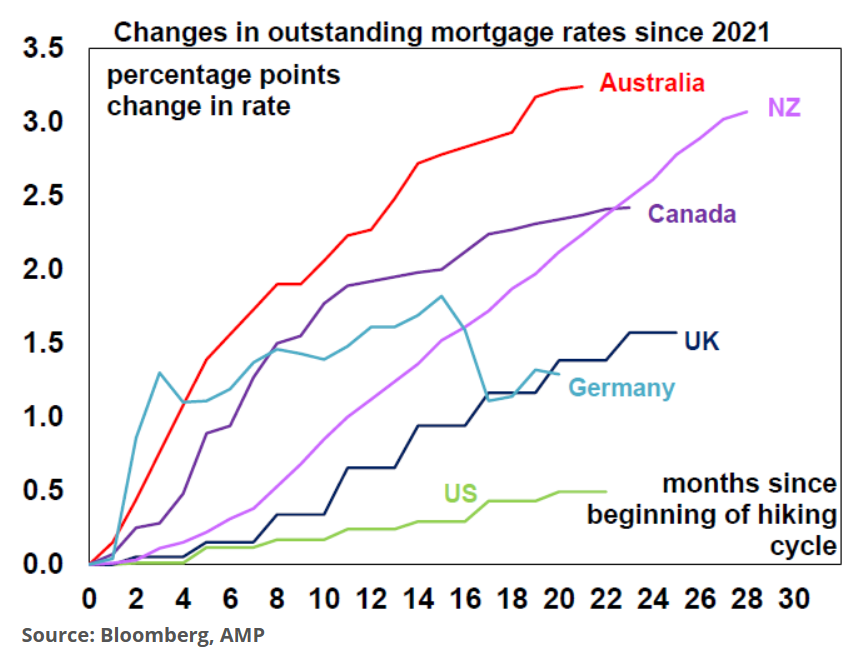

It is important to recognise that Australian households have been hit harder than elsewhere by monetary tightening owing to our predominance of fixed-rate mortgages.

This has meant that rate rises have been passed onto Australian borrowers far quicker than elsewhere:

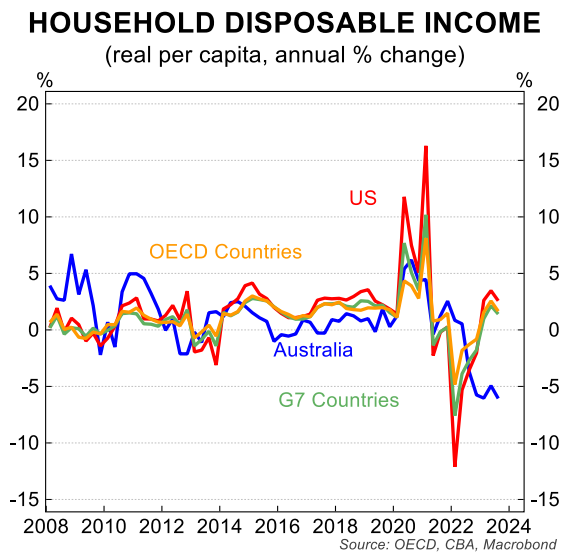

Australian households are doing it tough. They experienced the sharpest decline in real household disposable incomes last year, owing to the sharp lift in mortgage rates, relatively weak wage growth, and rising income taxes:

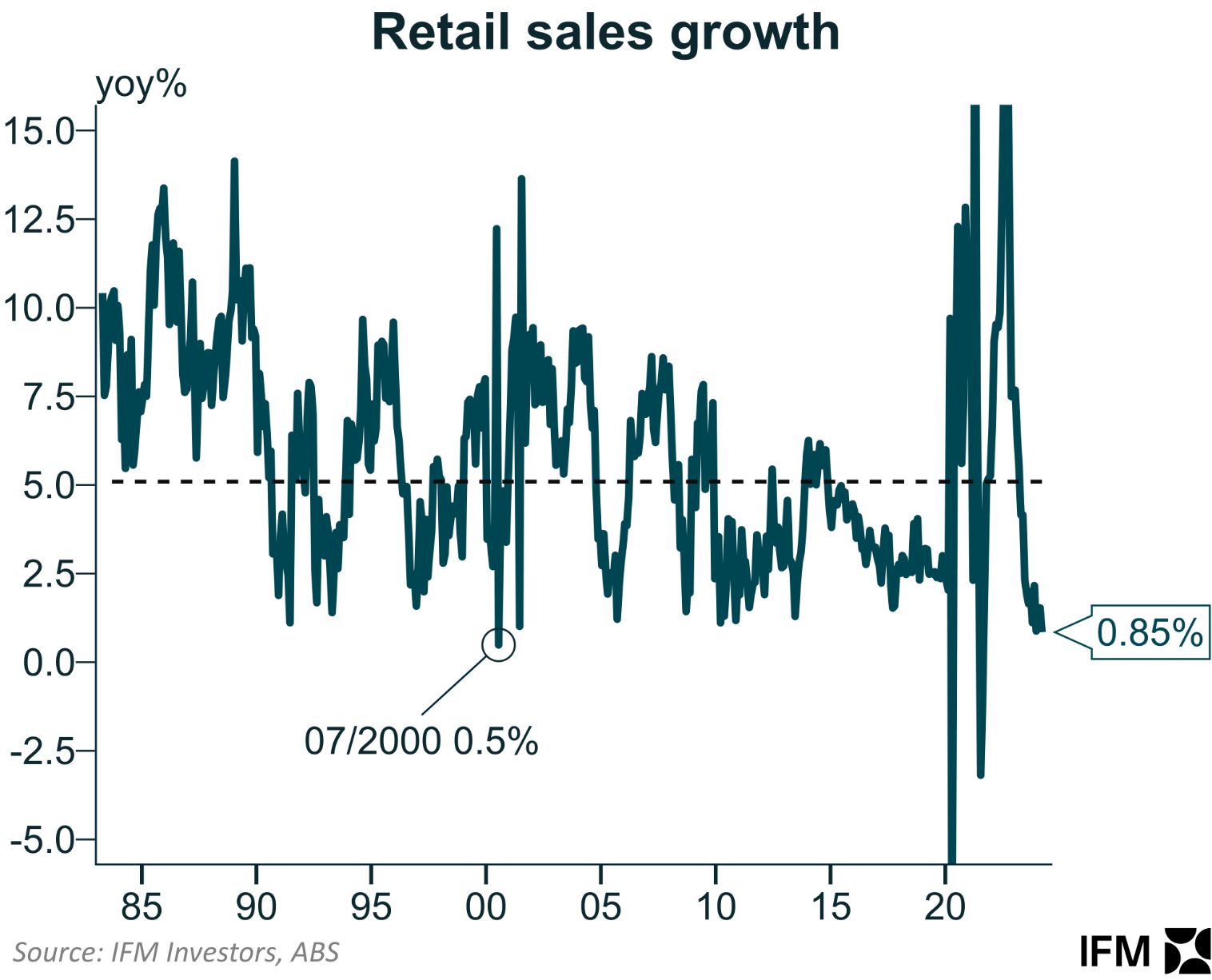

This consumer weakness was exposed on Tuesday when the Australian Bureau of Statistics (ABS) reported the lowest annual retail sales growth since 2000 (outside of the pandemic and the time when the GST was introduced):

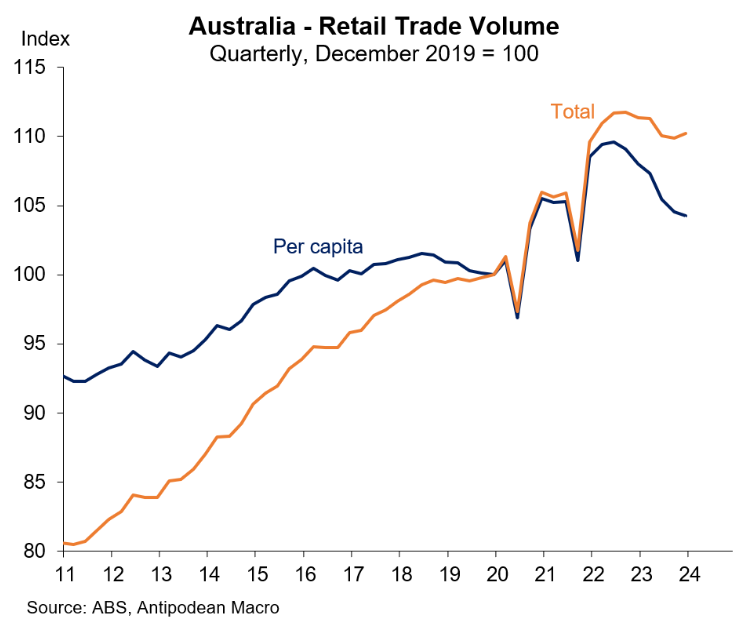

Indeed, as the below chart from Justin Fabo at Antipodean Macro shows, real per capita retail sales have collapsed into a deep recession:

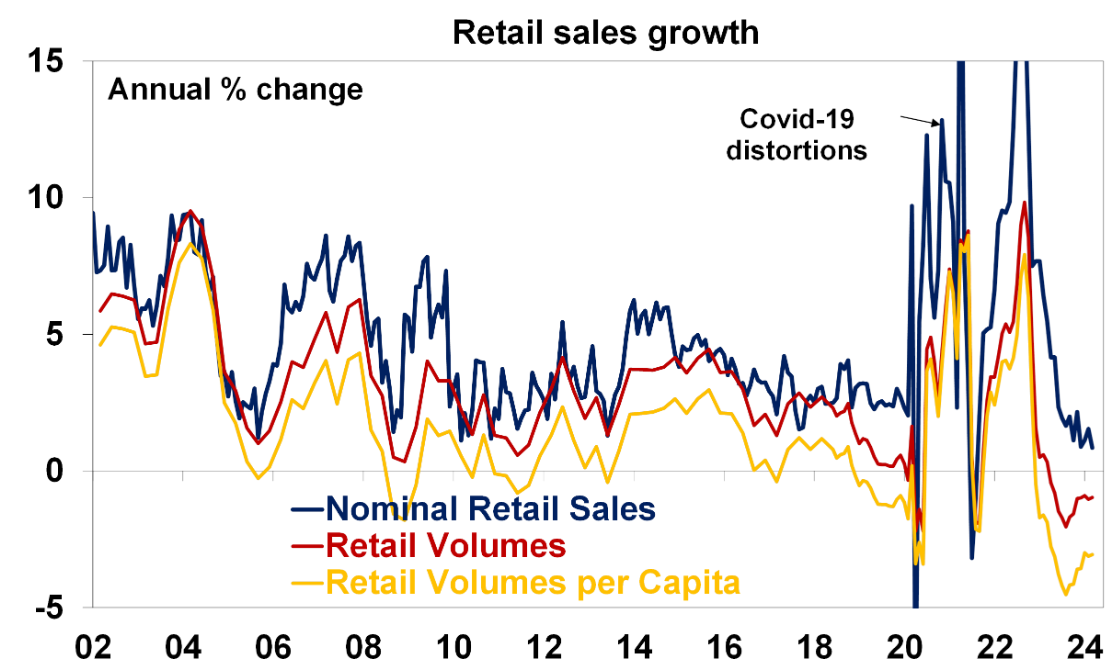

The next chart from AMP presents the same data on an annual change basis:

Source: AMP

It is difficult to see how the RBA would raise interest rates when consumer demand is so weak.

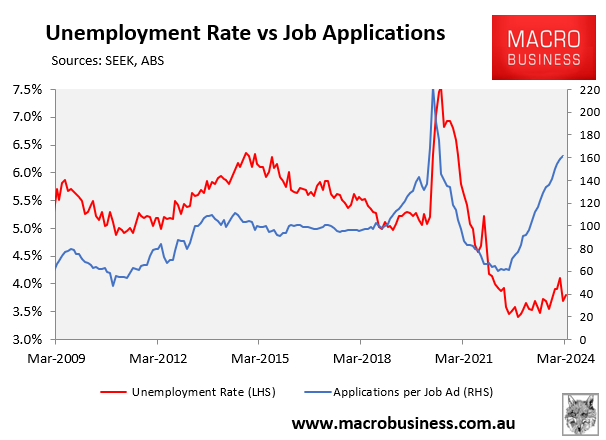

Unemployment is also destined to rise as labour supply growth swamps job creation:

The interest rate hawks need to take a chill pill and calm down. Rate cuts might have been delayed. But the next move in rates is still likely to be down.