AMP Chief Economist Shane Oliver has written a post explaining why he believes that the Reserve Bank of Australia (RBA) is still likely to commence an easing cycle later this year.

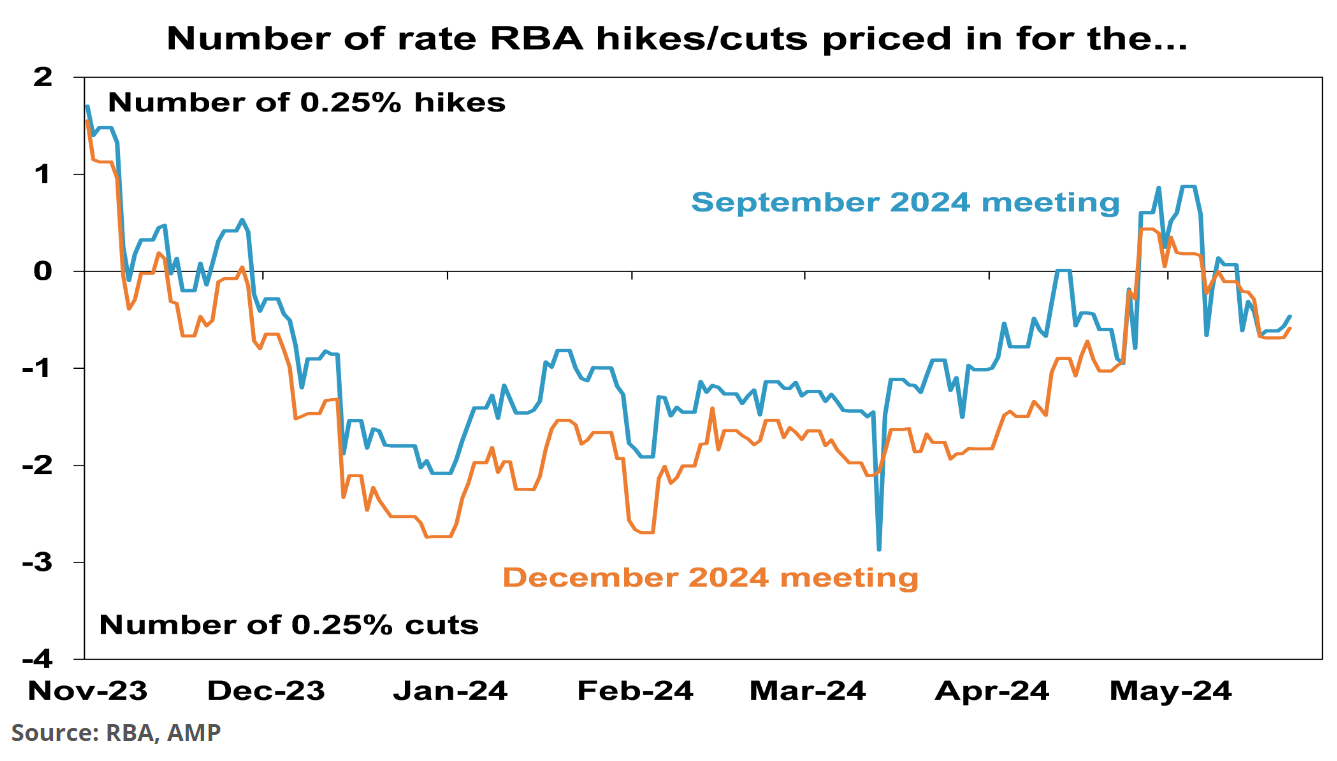

Oliver notes that interest rate expectations have been on a rollercoaster ride this year, with the RBA considering another hike and warning that “the risks around inflation had risen”.

The main arguments for further rate hikes include services inflation and trimmed mean inflation remaining sticky at 4.3% yoy and 4% yoy in the March quarter, wage growth potentially having another leg up, the Budget providing additional stimulus to the economy, and the RBA cash rate being below that in comparable countries.

However, Oliver argues that the RBA’s hurdle for another hike is high, requiring future data to threaten its forecasts for inflation to return to target in 2025 and 2026.

Oliver believes that the most likely outcome is the RBA holding at current levels, ahead of rate cuts later this year.

He also provides several reasons why the RBA’s next move is likely down later this year.

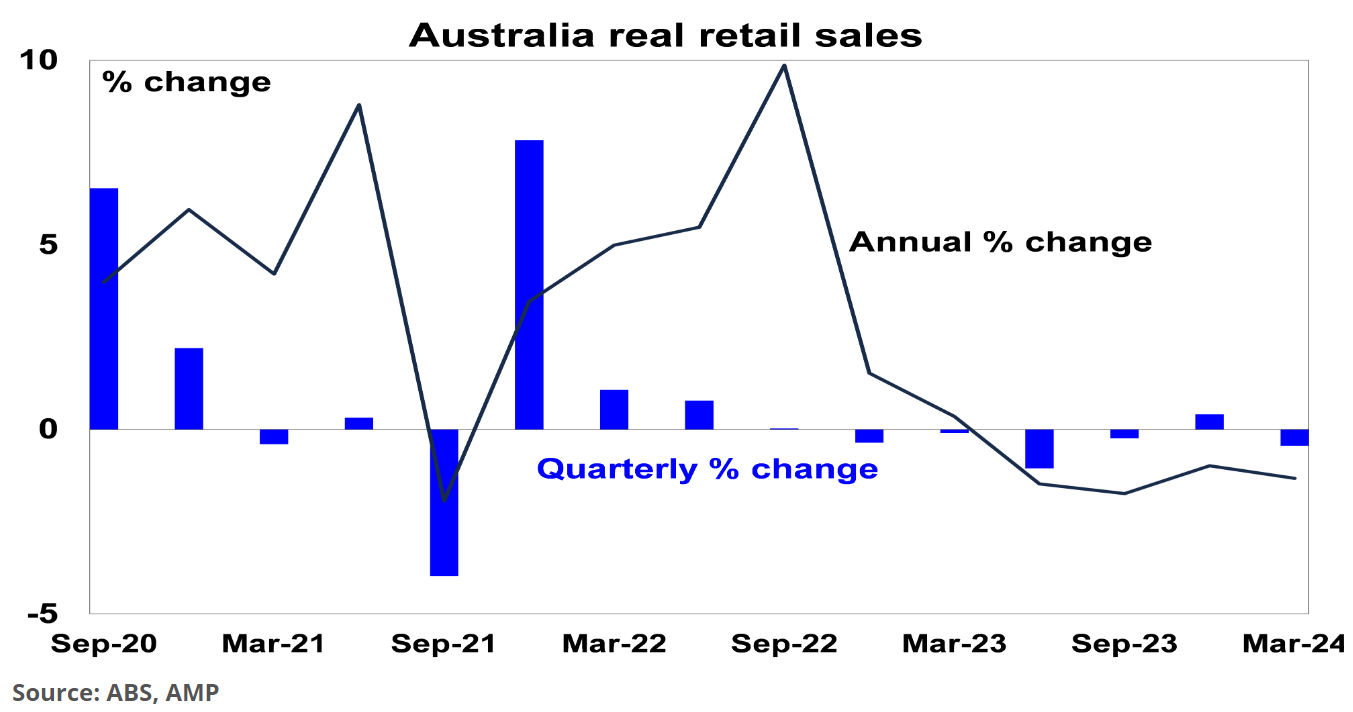

First, the economy has slowed to a crawl and likely remains in a per capita recession, with real retail sales falling again in the March quarter.

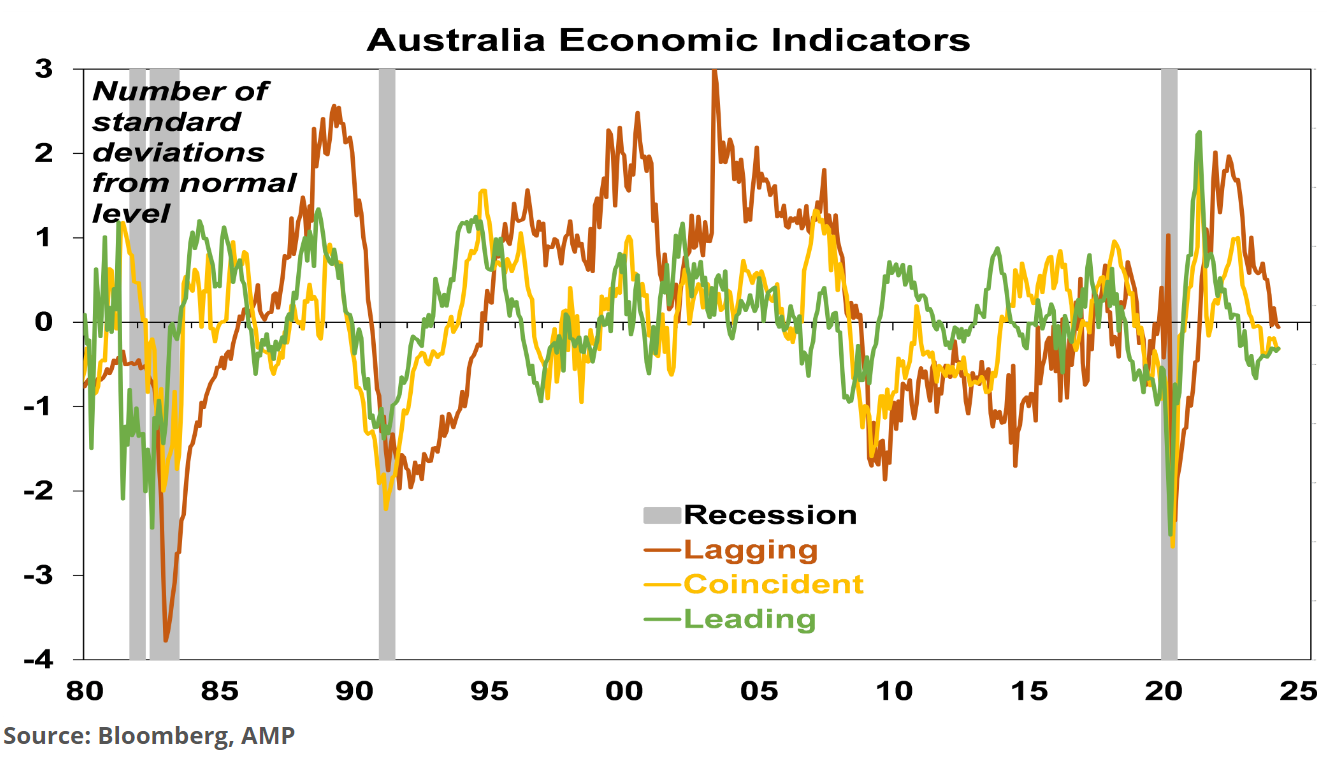

Household spending data suggests real consumer spending is flat to negative on a year ago. And leading indicators point to slow growth ahead.

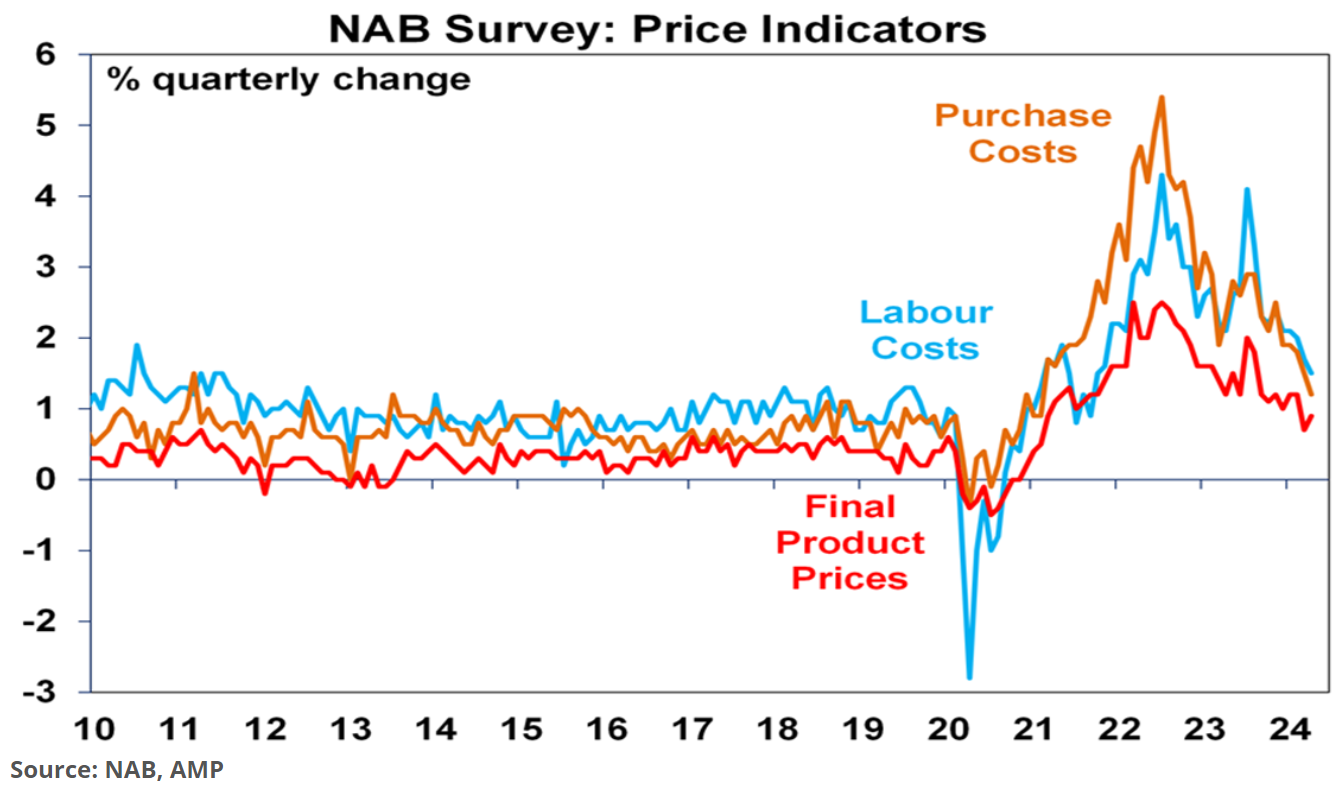

This weak demand means inflation is likely to resume its downswing. Notably, “the Melbourne Institute’s April Inflation Gauge points to a resumption of the falling trend; and similarly the NAB business survey points to a falling trend in cost and selling price inflation”, notes Oliver:

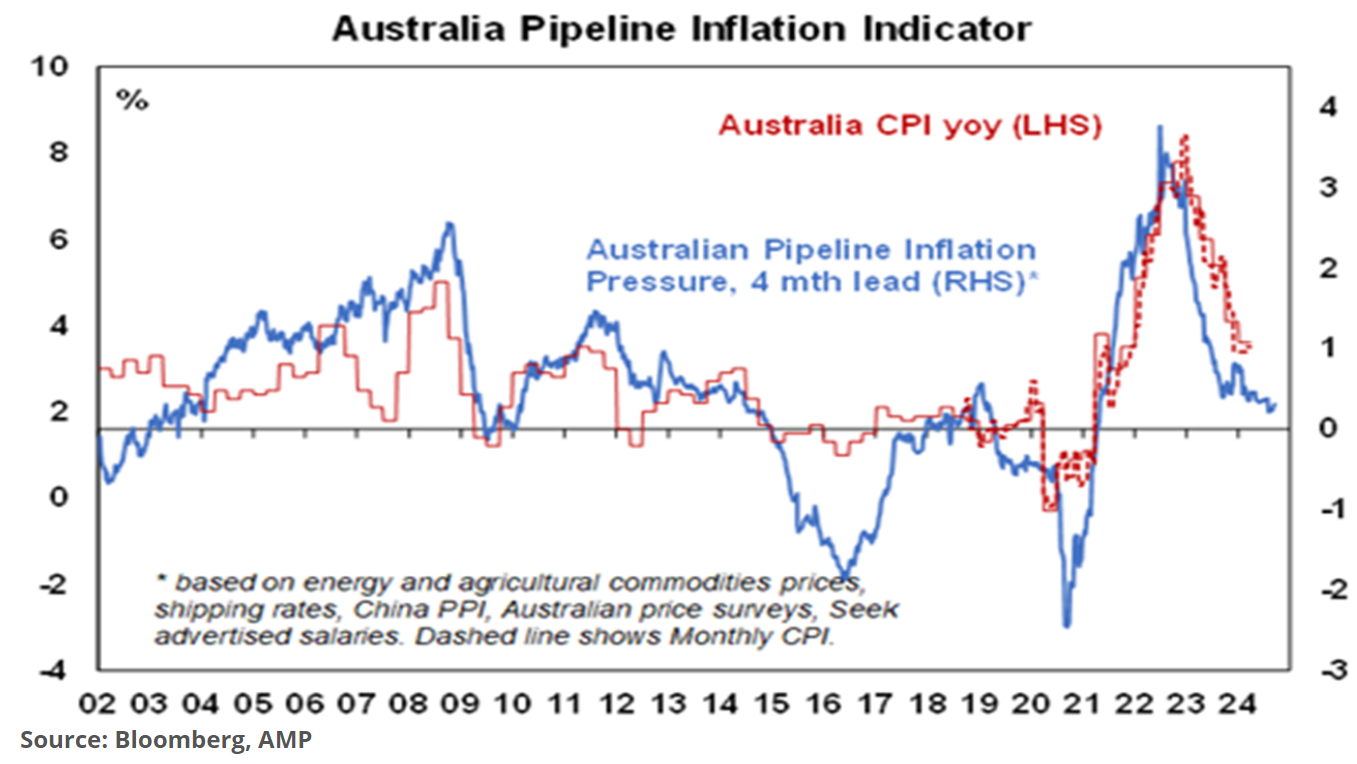

AMP’s own inflation pipeline indicator is also pointing to a lower inflationary pulse:

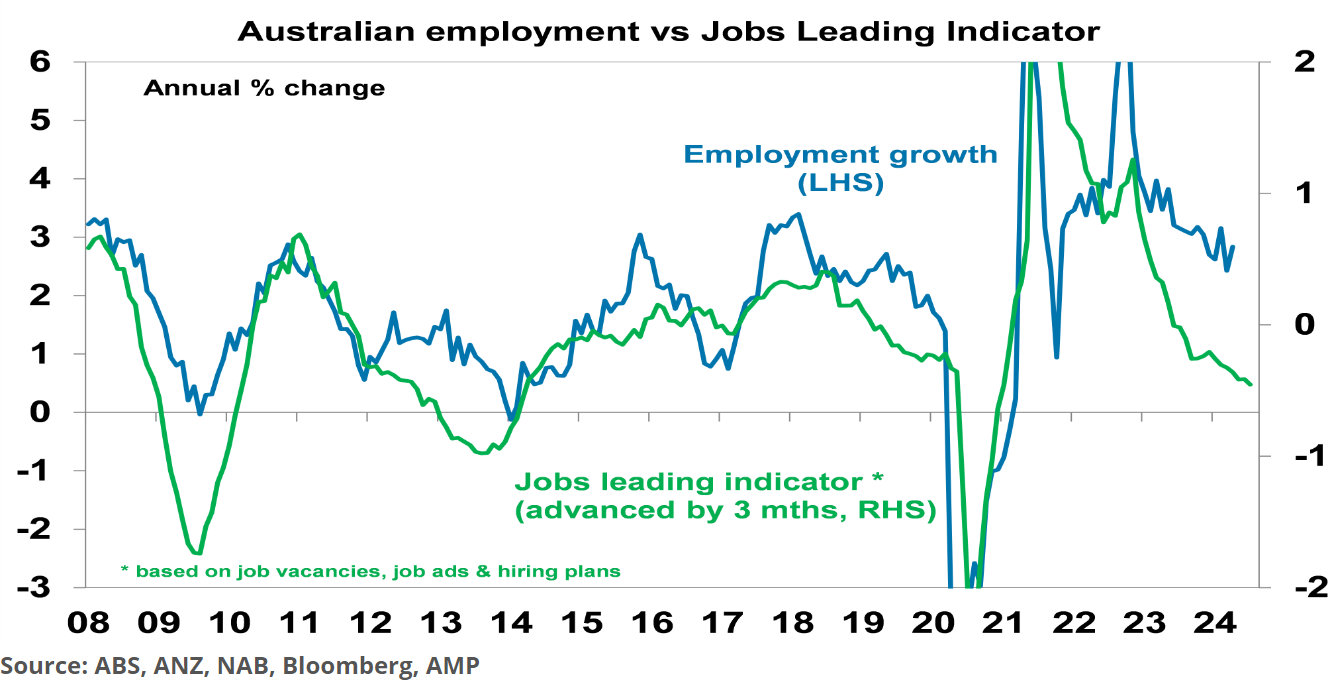

The Australian labour market is also cooling, indicating slower wage growth and lower services inflation:

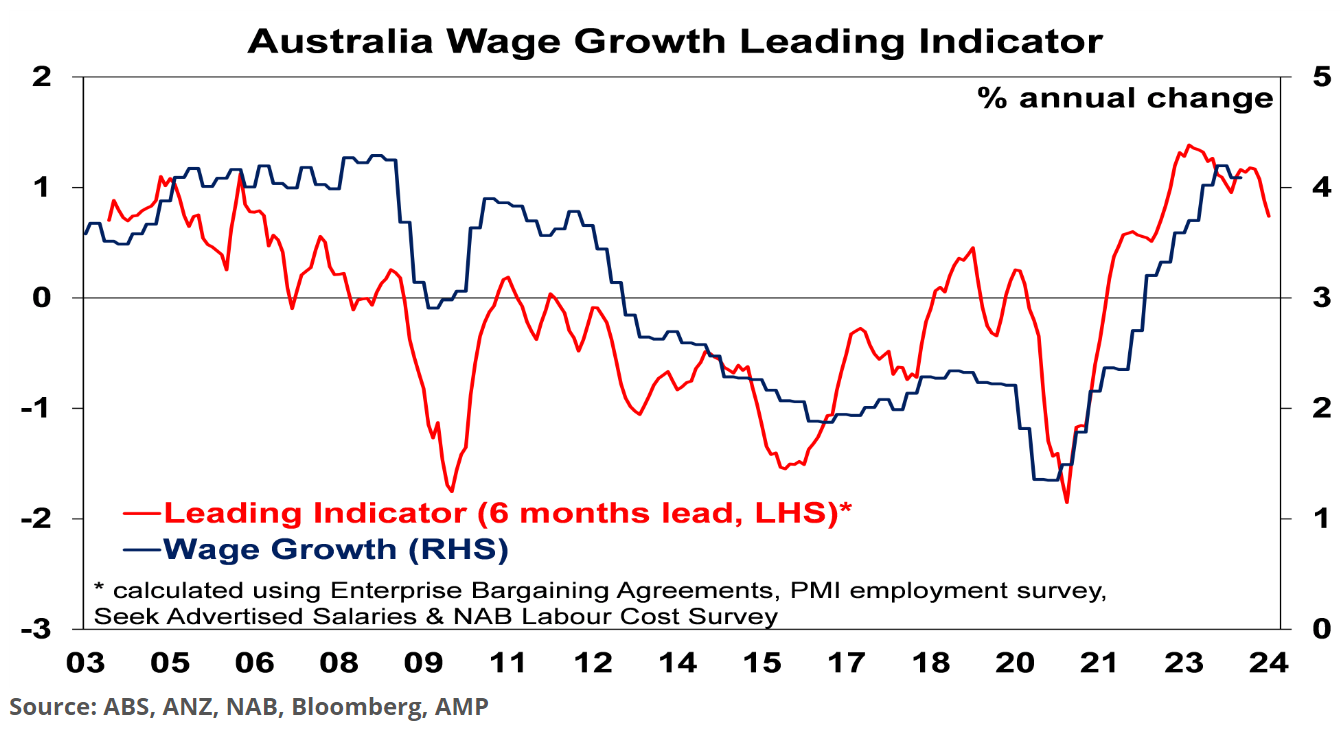

The AMP’s wages Leading Indicator also points to slower wages growth ahead:

The March quarter global inflation scare also appears to be receding, with Switzerland and Sweden cutting rates, the ECB, Canada, and UK looking on track to start cutting around mid-year, and the US Fed starting cutting in September.

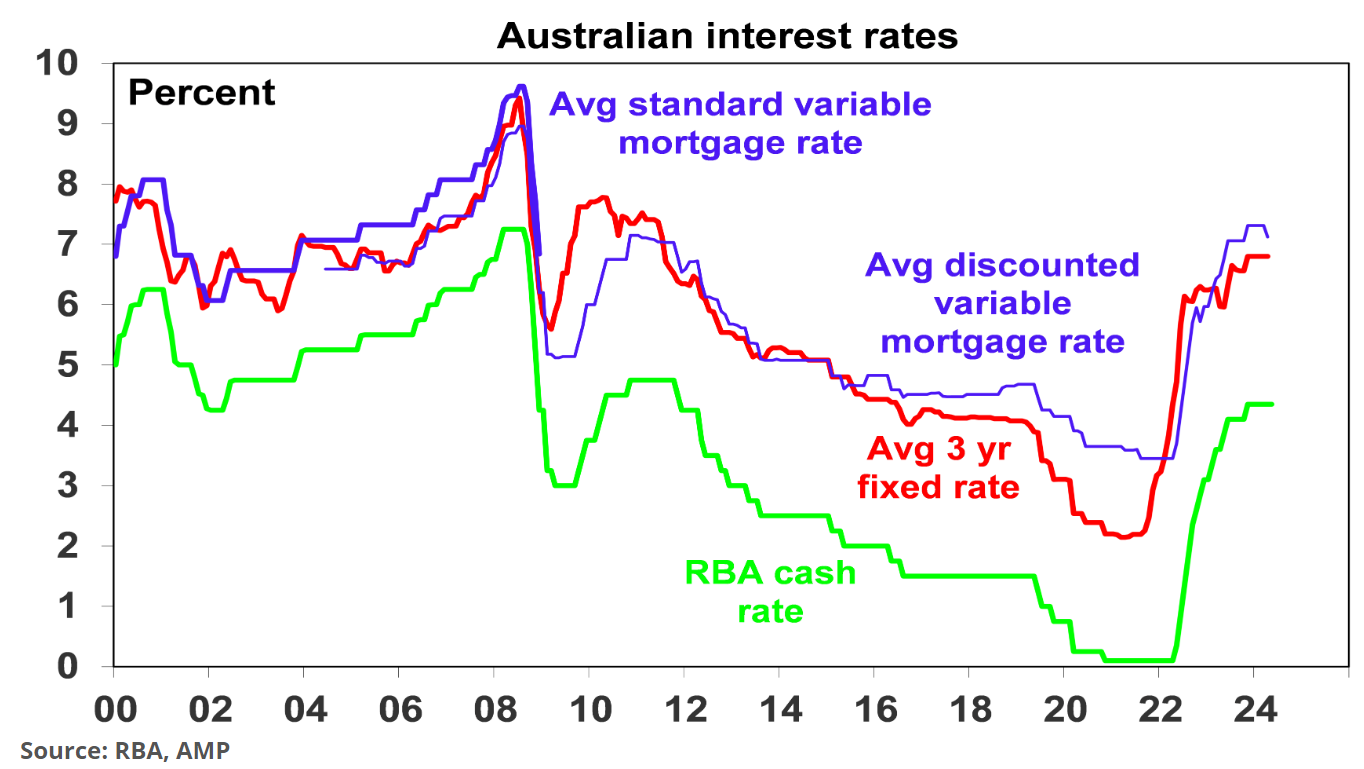

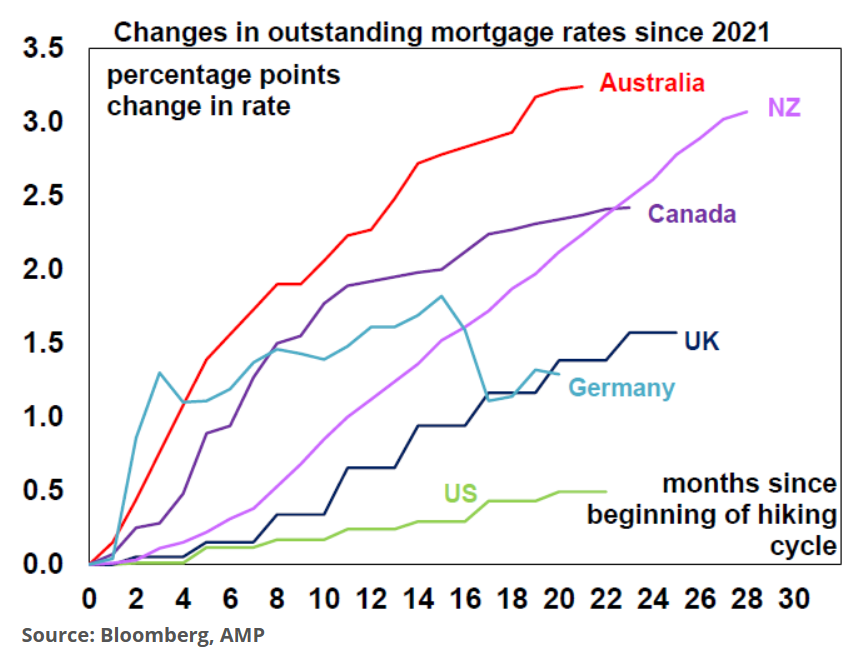

The rise in average outstanding mortgage rates in Australia also exceeds that in other countries, implying a bigger hit to households.

The Budget was more stimulatory than ideal, but the extra stimulus was relatively modest, potentially causing a downward revision to RBA inflation forecasts.

Oliver notes that the key things to watch will be monthly inflation data, the upcoming Fair Work Commission (FWC) decision regarding award wages, unemployment, and household spending.

I obviously agree with his analysis and have argued repeatedly that the next move in rates is down. It is only a matter of when.