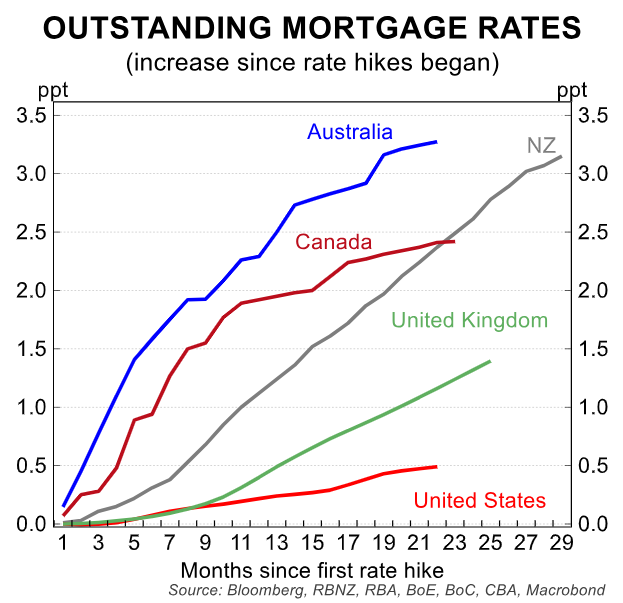

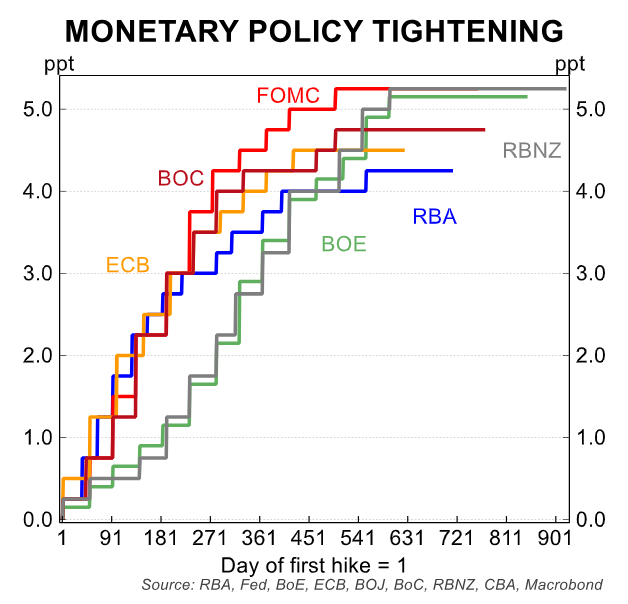

Australians have seen one of the most significant hikes in mortgage rates in the world:

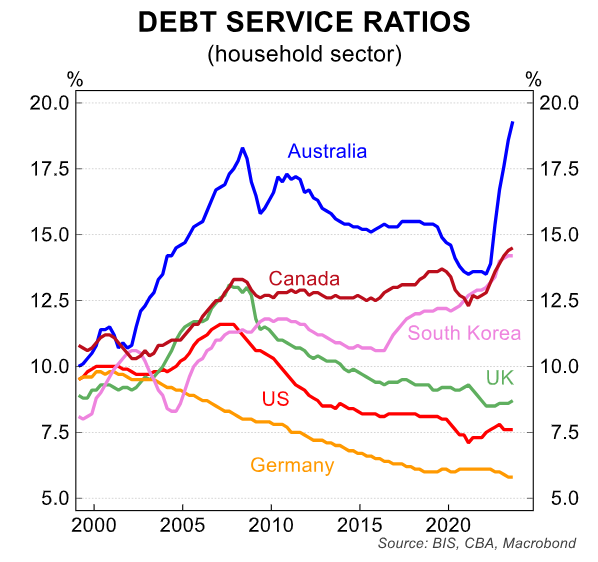

Australians have also seen the highest increase in debt servicing costs in the world:

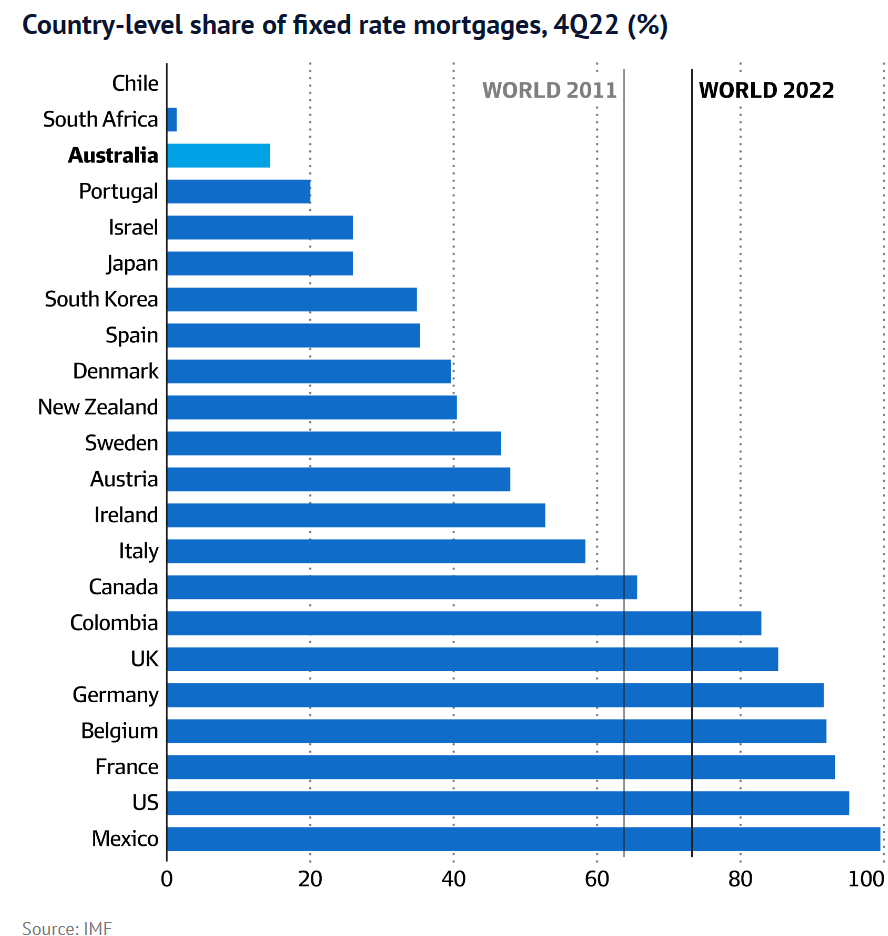

The reason why should be obvious. Australia has one of the greatest concentrations of variable rate mortgages in the world. Our fixed rate mortgages are also relatively short-term (i.e., three years or less):

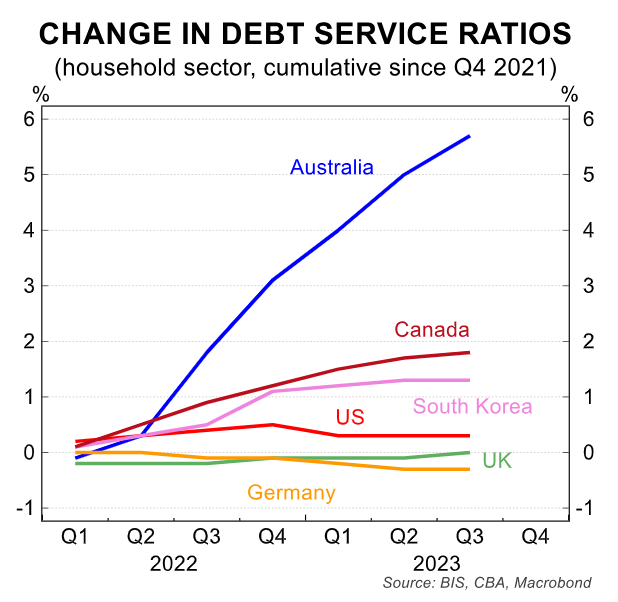

This extreme concentration of variable mortgages has resulted in Australian mortgage repayments rising far quicker than elsewhere, despite the Reserve Bank of Australia (RBA) raising official interest rates by less than elsewhere:

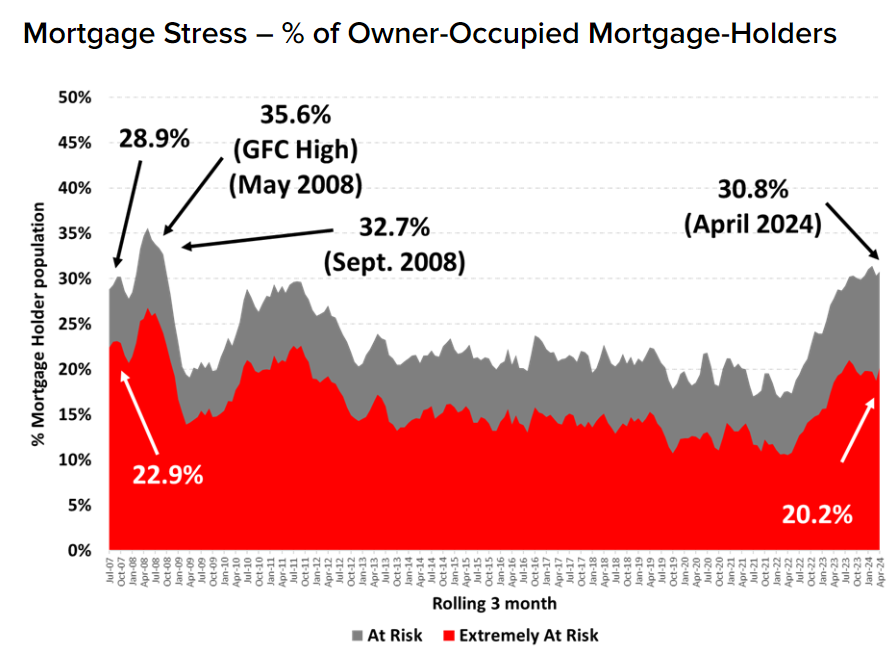

The impact on Australian household finances is illustrated in the following chart from Roy Morgan Research.

Roy Morgan estimates that nearly 1.6 million mortgage holders (30.8%) were ‘At Risk’ of ‘mortgage stress’ in the three months to April 2024:

In the two years since the RBA commenced its interest rate tightening cycle, the number of mortgage holders ‘At Risk’ of mortgage stress has increased by 753,000, according to Roy Morgan.

“The number of Australians ‘At Risk’ of mortgage stress has increased by 753,000 since May 2022 when the RBA began a cycle of interest rate increases”, Roy Morgan noted.

“Official interest rates are now at 4.35%, the highest interest rates have been since December 2011, over a decade ago”.

“The number of mortgage holders considered ‘Extremely At Risk’, is now numbered at 994,000 (20.2% of mortgage holders) which is significantly above the long-term average over the last 10 years of 14.4%”, Roy Morgan said.

While mortgage stress levels are currently running below the GFC peak, they have increased considerably over the past two years amid the RBA’s aggressive rate hikes.

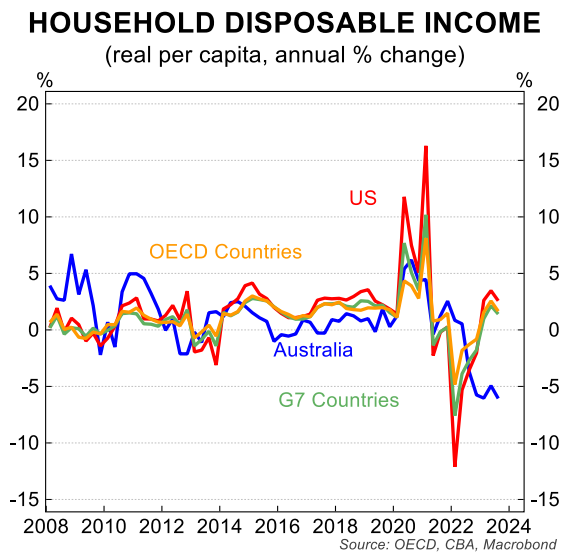

Australian mortgage holders have also been hit far harder than residents of other nations. This partly explains why Australians experienced the sharpest decline in household disposable incomes last year:

If you wish to save thousands of dollars in mortgage payments, try the MB Compare n Save mortgage comparison tool. It takes less than a minute.

And if you choose to refinance, Compare n Save will handle the process.