The NAB Survey for April was not pretty for workers.

Business confidence and conditions slipped 2 points to +7 index points, below the 10-year average but around the long-term average of the monthly series.

Confidence remained positive at +1 index points.

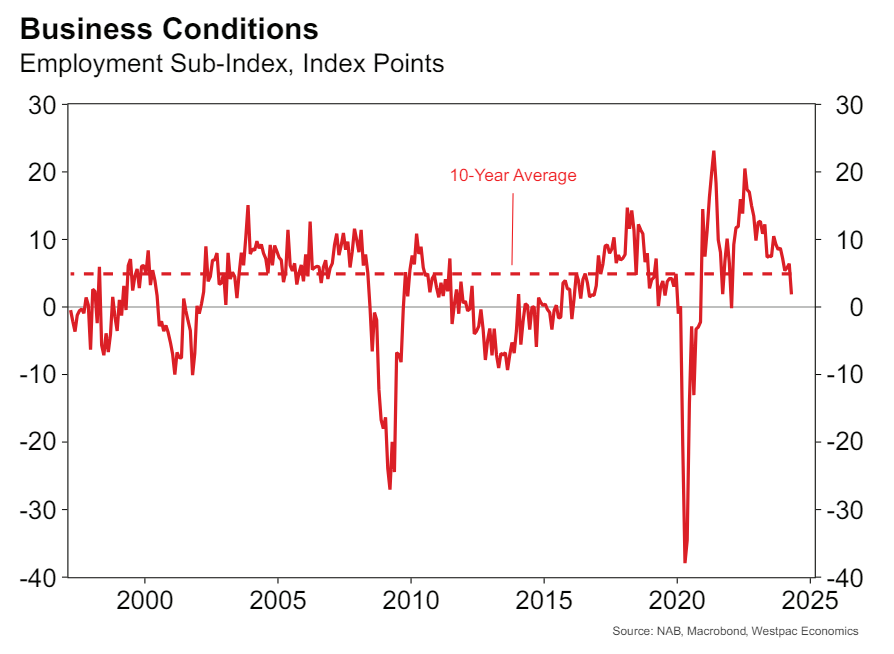

However, the employment sub-component fell 5 points to +2 index points, the lowest level in over two years and the first time this measure has fallen below the 10-year average since January 2022:

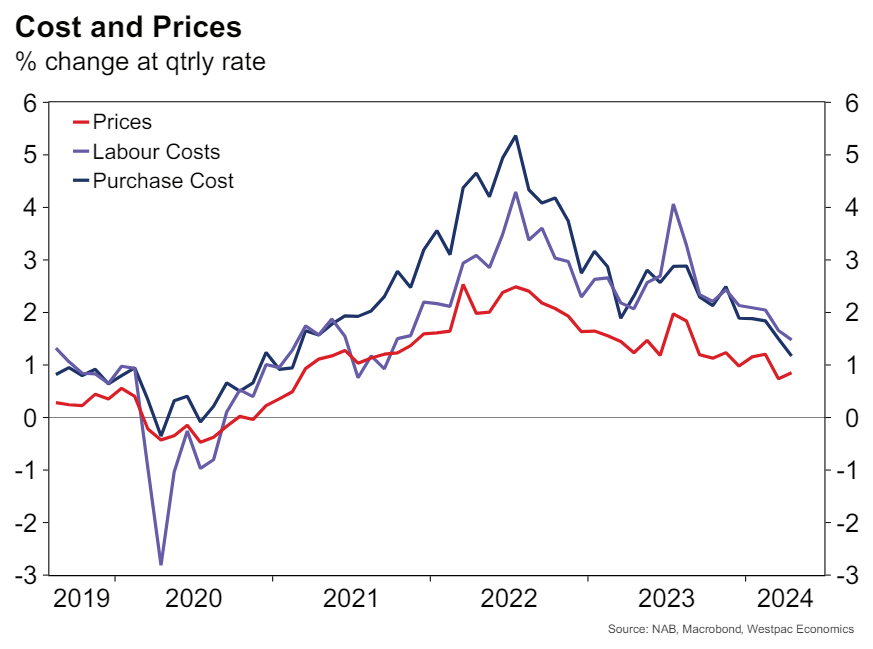

Wage growth is cooked:

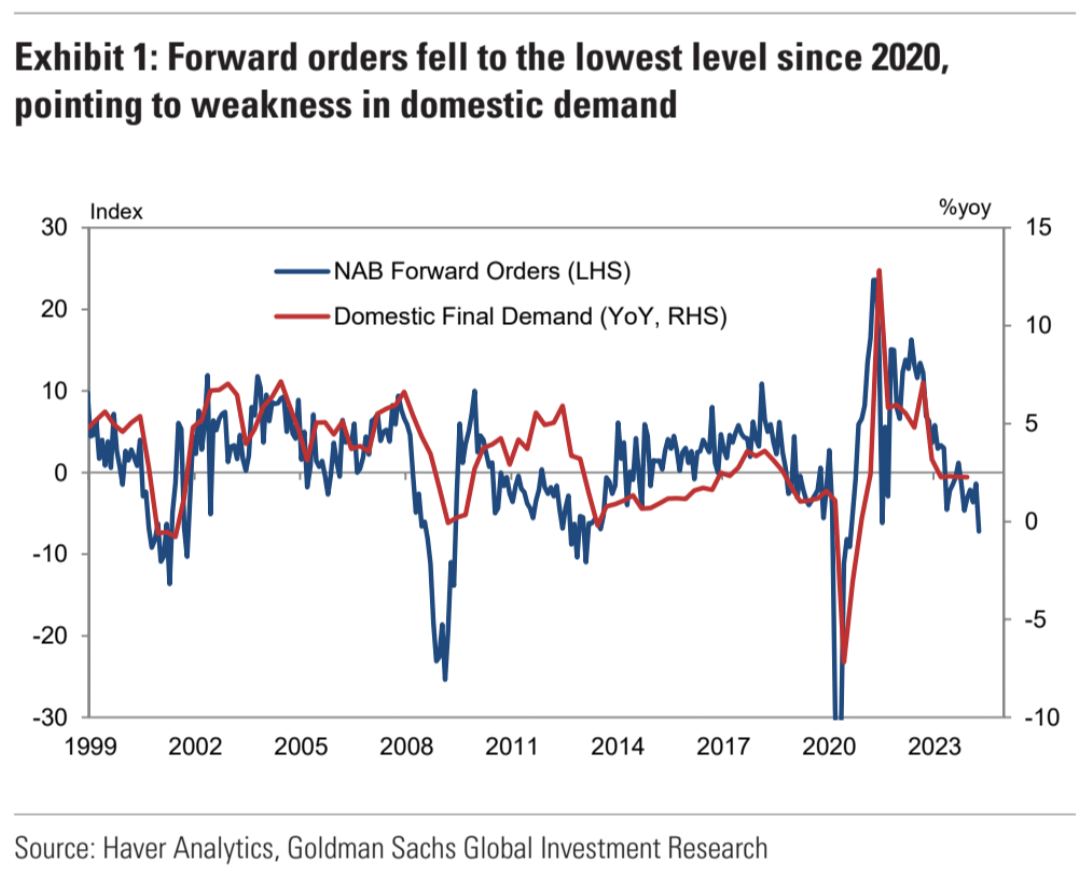

And forward orders indicate deepening downward momentum:

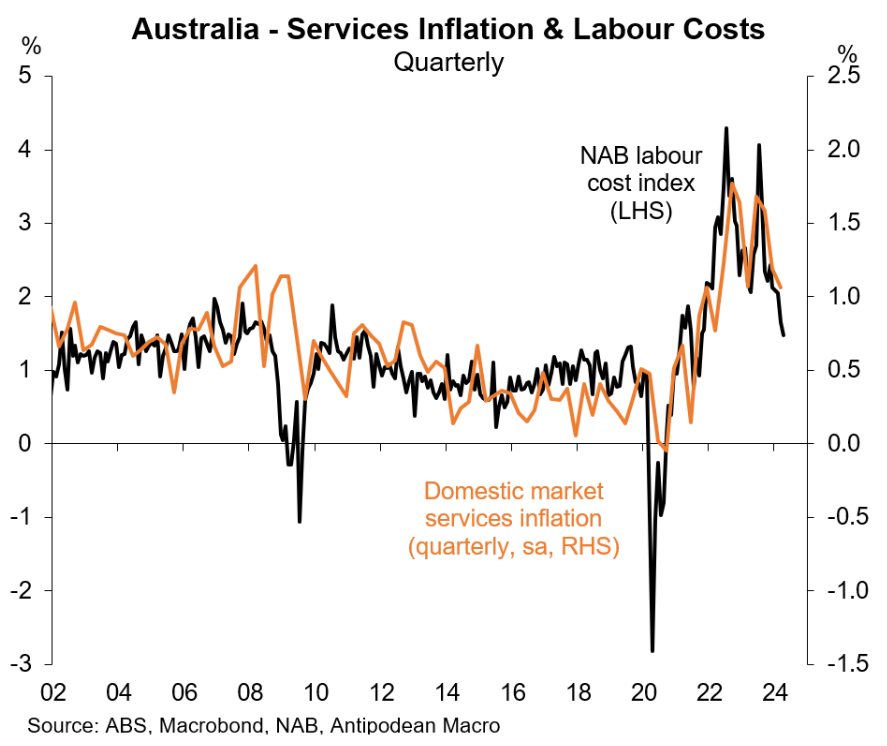

We are tumbling back into the lowflation period for wages. Sticky services inflation will break lower with wages.

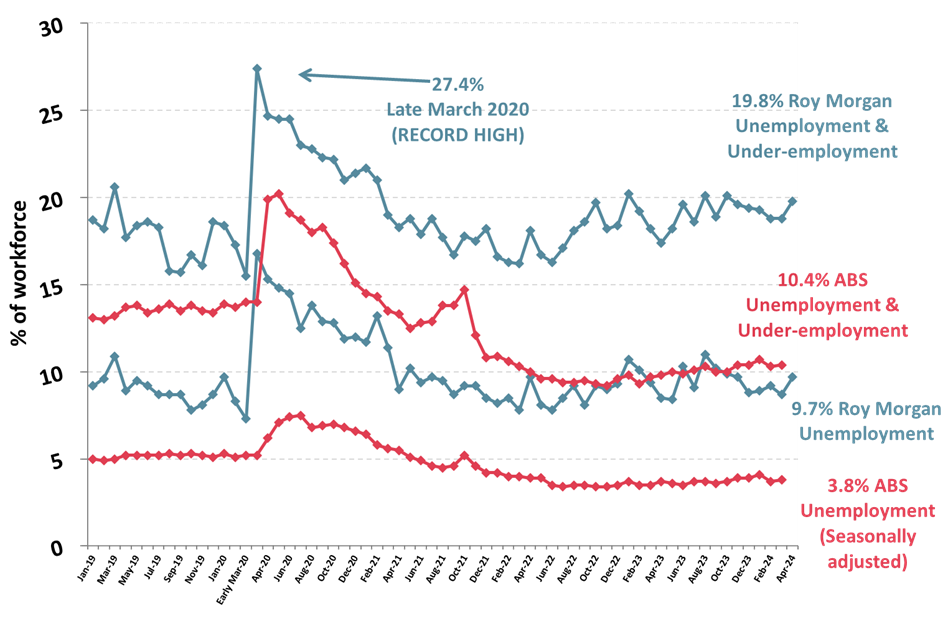

Adding further corroboration is the Roy Morgan Unemployment & Underemployment rate, which has been trending higher for a year. Remember that underemployment is a key feature of the labour expansion mass immigration model and we are well above pre-COVID looseness:

In April 2024, Australian ‘real’ unemployment increased 177,000 to 1,535,000 (up 1% to 9.7% of the workforce) despite overall employment remaining near its all-time high at over 14.2 million.

In addition to the increase in unemployment, there was also a slight increase in under-employment, up 18,000 to 1,594,000. These combined increases mean a massive 3.13 million Australians (19.8% of the workforce, up 1%) were unemployed or under-employed in April – the highest level of total labour under-utilisation for over three years since October 2020 (3.15 million) during the early months of the pandemic.

Every private labour market survey says the same thing. The labour market is loose as a goose, and wage pricing power has collapsed. Only the lagging and outdated ABS measure of unemployment is out of step.

The RBA needs to cut, not hike.