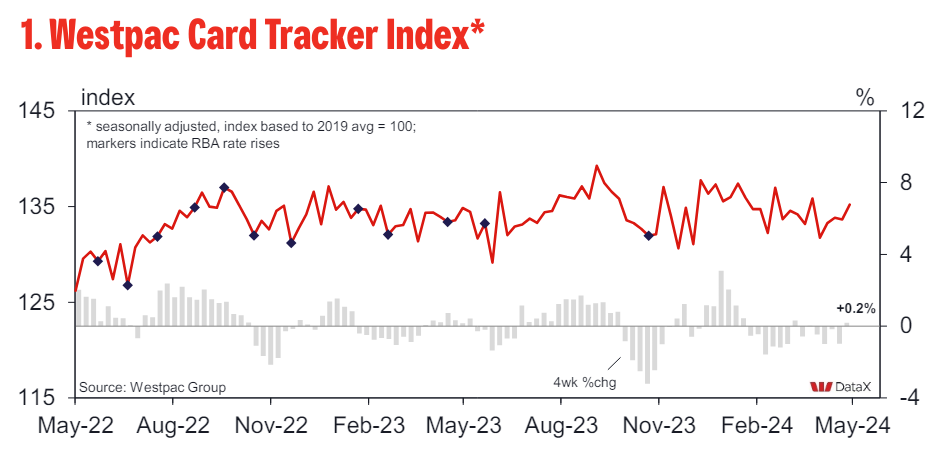

Over the past two weeks, the Westpac Card Tracker Index* has firmed once more, climbing 1.4 points to 135.2 as of the week ending May 18.

The Index is still somewhat below its April average and only 0.5 points over its level at this time last year, even with the firming.

The Index is now 1.8 points below its cyclical peak, which was reached in October 2022, a little more than a year and a half ago.

The quarterly growth pulse is still solidly negative, tracking at -0.9%qtr following a brief period in positive territory during March and early April, despite a slight uptick over the last four weeks.

All of these numbers are nominal, suggesting a more substantial contraction in real terms adjusted for inflation.

Although it has slightly improved, the most recent monthly momentum is unconvincing, says Westpac.

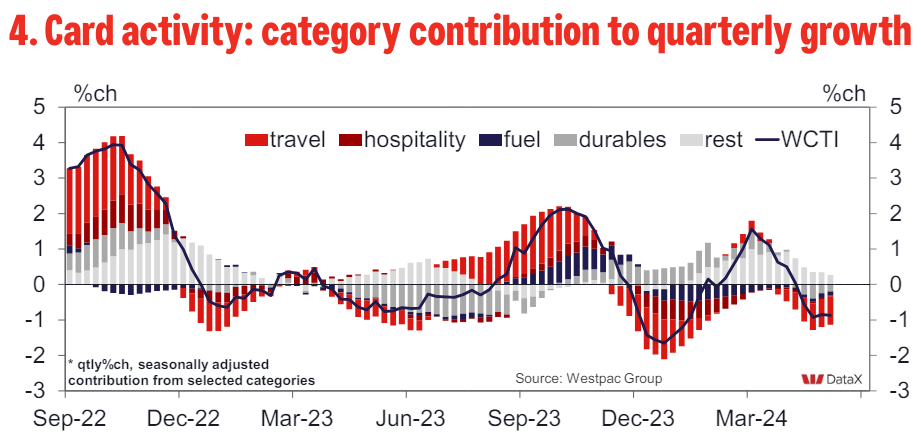

The category breakdown reveals a similar pattern, with discretionary factors—while durables’ effect on quarterly growth momentum has somewhat lessened recently—driving the recent negatives:

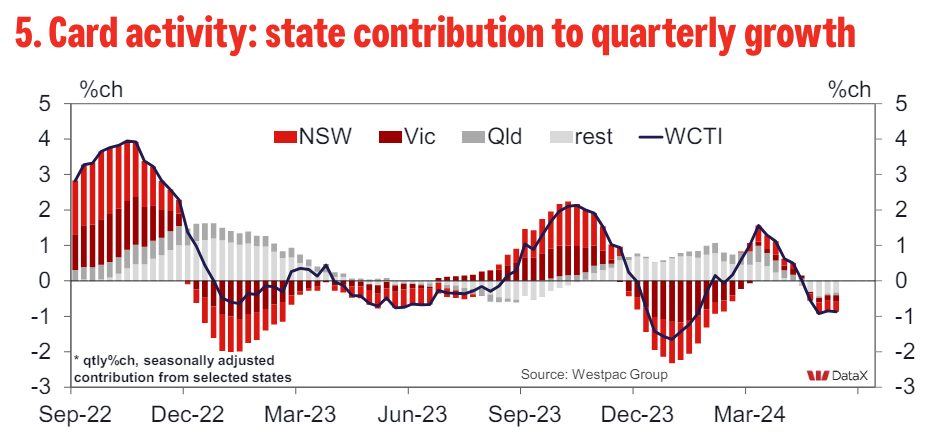

State-by-state decreases are still widespread. QLD is holding up marginally better than the other majors:

Westpac believes that unless disposable earnings start to look better, consumer spending is unlikely to show much of a comeback before the tax cuts take effect in July.