Dxy is sagging:

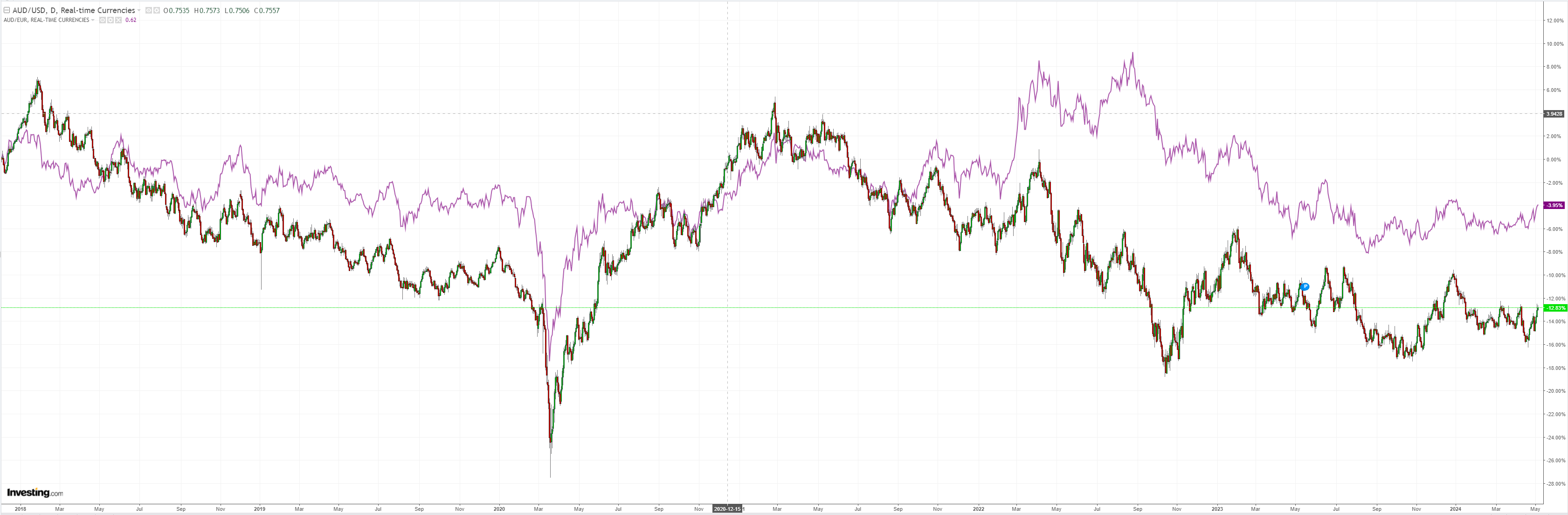

AUD has no clear pattern but is threatening recent resistant at 66 cents:

Nothr Asia was mixed:

Oil is putting risk back in play:

Metal are a Wall Street toy:

Miners look ok:

Junk signals risk on:

Yields tumbled:

Stocks to the moon:

The question is, will Michell Bullock and her malformed new RBA panic. Credit Agricole:

AUD: RBA’s credibility testAn article in the Australian local press over the weekend has made investors a little nervous about a potential surprise rate hike by RBA on Tuesday.

The article writtenby a well-known RBA watcher points to periods when QoQ trimmed mean inflation has been 1% or more, as it was in Q1, the RBA has gone on to hike rates at the next meeting with few exceptions.

These exceptions include the introduction of Australia’s Good and Services Tax as well as during the GFC and Covid. The latter is referred to as a policy error.

Some investors could be wondering if the RBA hasr eturned to signalling the market via the media.

The RBA used to use reporters to signal the market when it thought market pricing had become too extreme.

FormerRBA Governor, Philip Lowe, did not use the practise during his tenure though. While speaking ahead of assuming the role of chair of philanthropic investmentmanager Future Generation Australia on Tuesday, Lowe warned rates may be yet to peak in Australia.

Another former RBA Governor and Macquarie Bank Chair, Glenn Stevens, issued a similar warning. Australian rates have moved a littlehigher on the back of the newsflow, but continue to price in little chance of a ratehike tomorrow.

RBA Governor, Michele Bullock has previously said the Board has little tolerance for upside surprises in inflation or further delay of its return to the target band, so tomorrow will be a significant credibility test.

Inflation is running above and the unemployment rate below the RBA’s forecasts.

To maintain credibility, Bullock has to move back to a tightening bias from the neutral bias it installed in February. We continue to think the RBA will likely not move from a neutral bias to hiking rates tomorrow.

The central bank will also likely raise its near-term inflation forecasts by 25bp, but the important thing to look out for in our view is when the central bank forecasts inflation to fall back within its 2-3% target band.

On this front, the RBA will probably still have inflation falling back with in its target band by late 2025 citing seasonal factors behind the Q1 reacceleration in inflation.

This would justify an on-hold decision on Tuesday.

Overall,Bullock will likely take a wait-and-see approach to rates. Consumption data has softened lately and a large amount of mortgages are being rolled over into higher rates in the coming months.

But, the labour market remains tight and consumption could get its second wind from another large minimum wage increase, further government cost-of-living relief as well as scheduled tax cuts.

Bullock’s wait-and-see approach will not likely be enough to support current market pricing of about a 40% chance of a rate hike by September and ouldweigh on the AUD on Tuesday.

The labour market is as loose as a goose and if the RBA does not know it should be shut down:

On hold and no change to bias is my guess.