DXY was down Friday night:

AUD was up a little:

JPY is sinking towards doom:

AUD bears bolted for the exit last week:

Oil up and gold down:

Dirt bubble keeps popping:

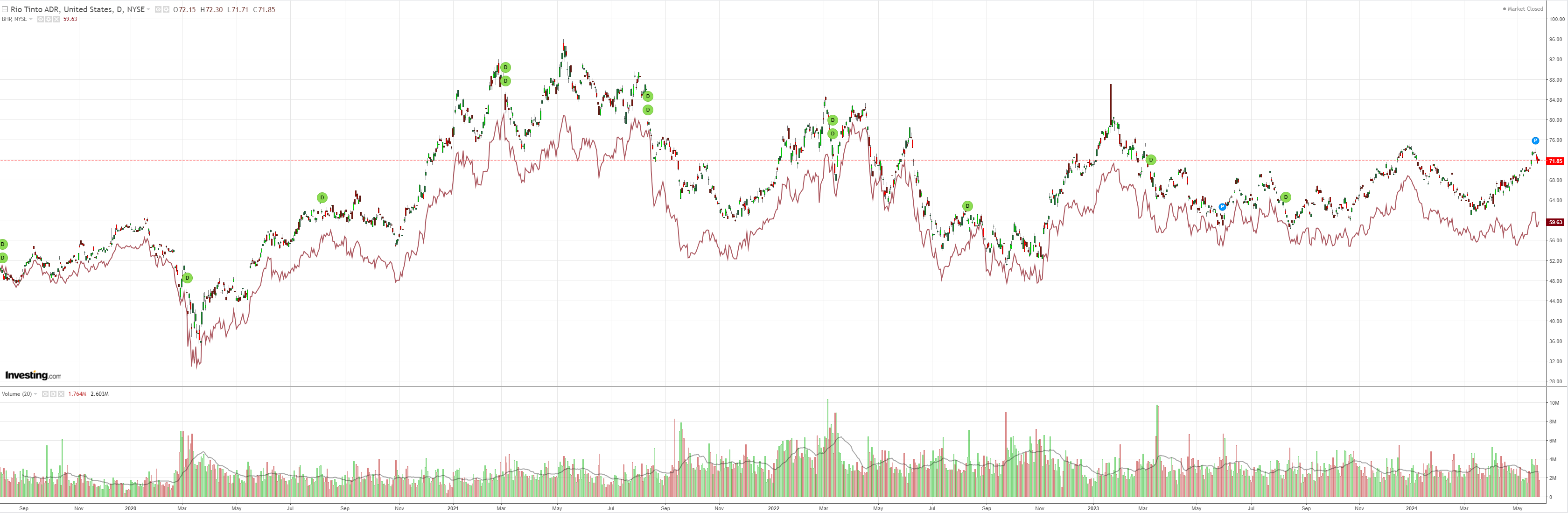

Big miners firmed:

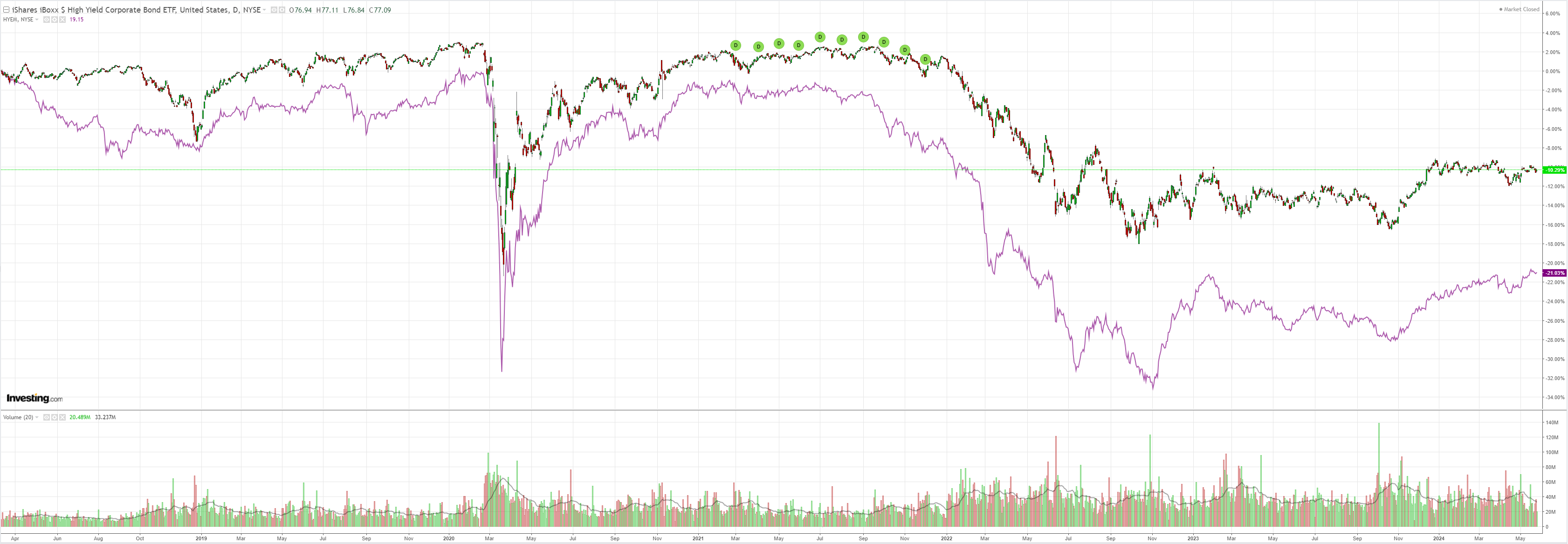

Junk firmed:

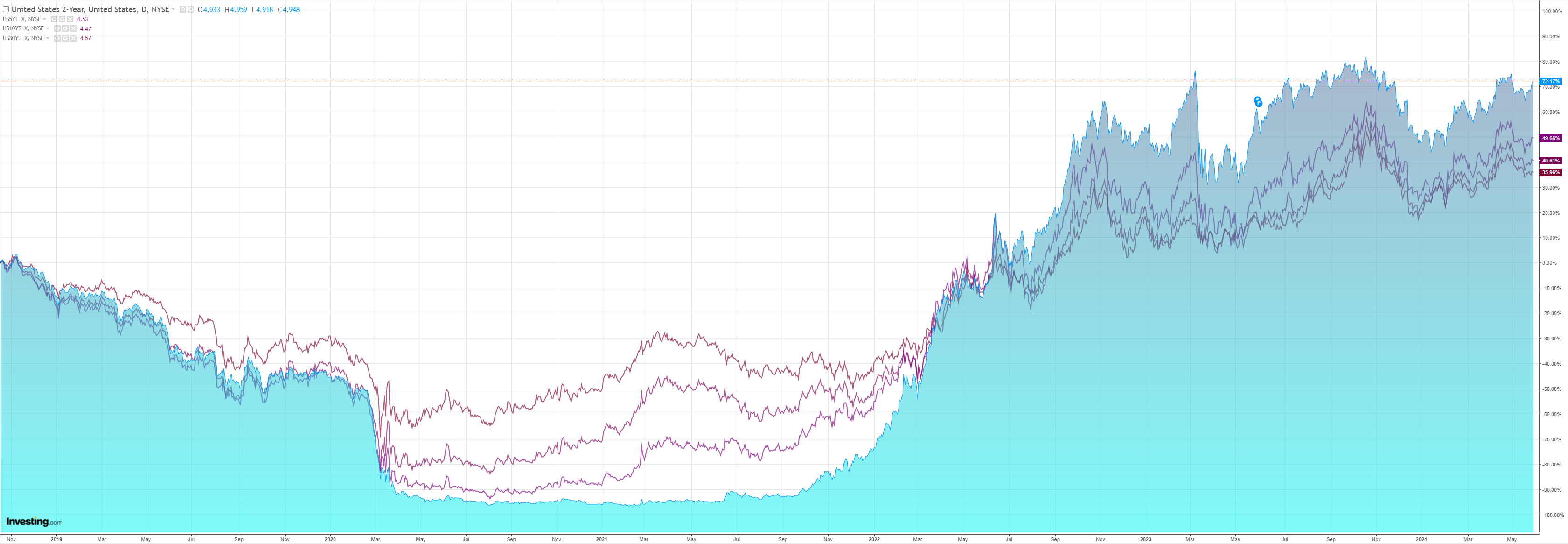

Treasuries too:

Which lifted stocks:

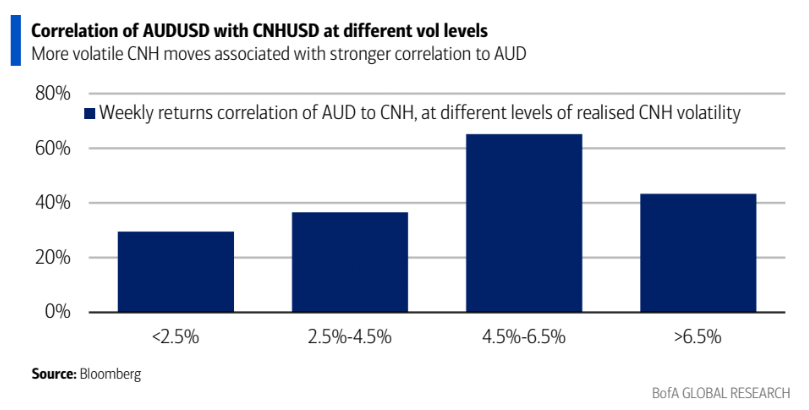

BofA captures the AUD’s soggy bounce:

China and AUD–headwind, tailwind or windless?

By some measures, AUD (specifically trade weighted ex USD) is no longer durably sensitive to China sentiment.

We take a deep dive into the impact of China on AUD,arguing that structural changes to Australia’s balance of payments partly explains this diminished beta.

However, China’s import impulse still matters, in our view, with recent AUD stability perhaps simply attributable to stable import growth from Australia.

China’s property impulse…

In our view, a recovery in China new home sales and steel production are necessary conditions for property-driven growth in commodity imports from Australia.

This is not evident yet and while recent property easing measures could lift sentiment, our economists do not expect an immediate impact on construction activity and investment.

AUDUSD is a better expression of China views relative to other AUD crosses…. and CNY still matter A risk for AUD, which appears to have diminished over the past few months, is major RMB depreciation.

Our USDCNY forecast of 7.45 implies ~3% RMB depreciation–which based on the latest betas would be associated with ~4% downside to AUDUSD and ~1% downside to AUD TWI (ex USD).

But in our view, the pace of RMB depreciation matters-a controlled depreciation may have less spill over than a sharp devaluation (see Exhibit11).

Bullish AUD crosses

While China poses some downside risk to our year-end AUD/USD forecast of 0.69, we are bullish AUD crosses and long AUDCHF as a carry trade supported by policy divergence and the short-term rebound in China sentiment.

Many points I have made myself. More motley pain ahead for the bears?