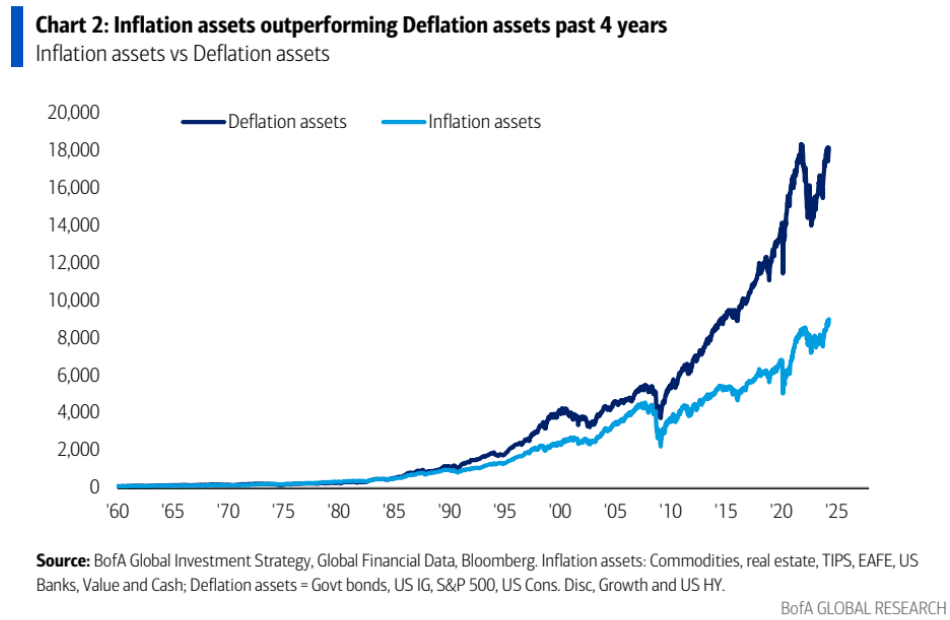

Michael Hartnett at BofA argues the inflation assets will continue to outperform over the long run:

The Price is Right: “Magnificent 7” up magnificent 24% YTD (Chart 3), contributing>50% of SPX return (NVDA alone=25%) as monopolistic mega tech monopolized performance; 3Cs of Crypto, China, Commodities also outperforming in ’24:bitcoin+60%, China +16%,gold+13%.; note commodities on course to be best-performing asset class 3 of past 4 years (Charts 5 & 6);biggest loser of’24 =30-year US Treasury(-6%).

Tale of the Tape: 2020s thus far: US national debt +50% (up $12tn),US nominal GDP+42% (up $9tn), US financial assets +38% (up $46tn–Wall St now 6 x size of Main St, Chart4), US Treasuries=48% of global government bond market, US credit & stocks>64% of respectiveglobal market caps….policy makers (and investors) know US “too big to fail,” set policy knowing recession more consequential than inflation.