Independent economist, Tony Alexander, discusses the recent weak economic data pervading New Zealand and how it increases the chances of “a series of quick interest rate cuts” later in the year.

The case for a quick series of interest rate cuts to occur and to commence before the end of this year was strengthened right at the end of last

week with a couple of data releases.

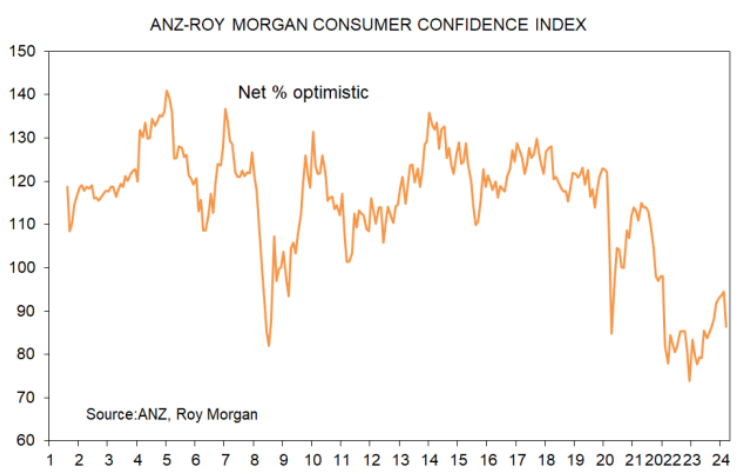

First, we had the ANZ Roy Morgan Consumer Confidence Index. The average reading for this measure over the past decade has been 112 and

just before the pandemic started early in 2020 the index stood just above 122.

It weakened to 85 briefly then soared to 114 as we went on a spending binge fuelled by excessively loose monetary and fiscal policies and inability to travel offshore.

The measure then fell to a record low of 74 at the very end of 2022 as people felt the strain from the credit crunch, falling house prices, and still rising interest rates.

There was also the November 2022 warning from the Reserve Bank (accurate as it turns out) that the economy was headed for recession.

It actually was already in it when they made that comment.

Over the second half of last year as house prices edged higher the index recovered to 95 in February. But this was still a relatively depressed level which helped encourage us economists to maintain a fairly downbeat outlook for consumer spending through all of 2024.

That outlook has now got worse because with confirmation of the economy being back in recession again the index has fallen back to just

86.

Consumers have a very negative outlook for the economy and the ANZ index move confirms the deterioration already revealed earlier in March by my own monthly Spending Plans measure.

It fell in March to a net 24% of respondents expecting to cut their spending over the next 3-6 months from -18% in February where the average reading has been -2%.

This graph shows the two measures together.

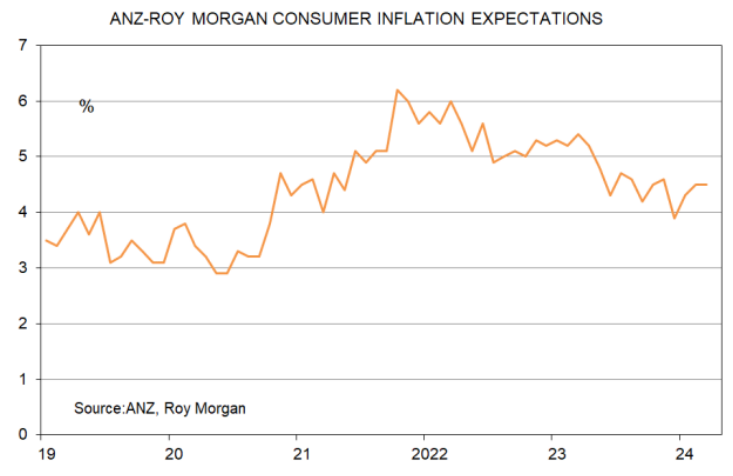

Unfortunately the fresh decline in sentiment has not been accompanied by a falling away of household inflation expectations.

After rising from 3.9% to 4.5% in February they held that level in March. This tells us that no policy easing from the Reserve Bank is imminent.

They need to see solidity of inflation heading to 2% and not just economic weakness.

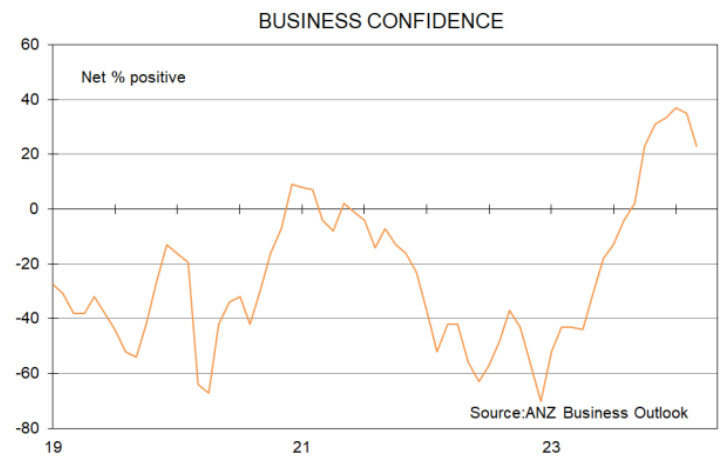

Which brings us to the second dataset released just before Easter. It also came from ANZ, and it also moved in line with what my monthly Business Survey with Mint Design had already shown.

The net proportion of businesses feeling confident about the NZ economy over the coming year has retreated to a still well above zero average of 23% from 35% in February.

Confidence of retailers still sits unusually high at a net 30% optimistic from 32% in February where the long-term average is 2%.

Given the terrible numbers coming out for retail spending over the past two years, the deterioration in consumer confidence, and announced closures of retailers, it seems reasonable to conclude that this result is politically driven.

That is, the change in government in October has been greeted so positively by many businesses that they are ignoring much of the business reality around them and expressing excess optimism.

Even farmers at a net 8% positivity sit well above average which for these perennially dour people is a net 22% feeling pessimistic about the

economy.

A net 4% of businesses say that they plan boosting payrolls in the coming 12 months. This is about where this measure has sat since August

and below the 7% long-term average.

Frankly it still looks a bit strong considering the layoffs occurring throughout the economy this year.

A net 4% of businesses plan raising their levels of capital expenditure in the next 12 months. This is down from 12% in February and well below the 11% average.

This is bad news for productivity growth in the economy which in turn is bad news for growth in incomes and inflation.

A key area of interest we all have in this monthly survey is the set of indicators relating to inflation.

In this latest edition a net 45% of respondents have reported that they plan raising their selling prices over the coming year.

This is a good change but only takes this measure to the bottom of its range of movement over the past year.

We cannot consider this to be a decisive shift down and neither will the Reserve Bank be jumping for joy.

At 45% this measure still sits well above the 25% average achieved during the period when inflation has average just over 2% in New Zealand since 1992.

The other prices-relevant measure is year ahead inflation expectations held by businesses.

There was a decent fall this month to 3.8% from 4.03% in February. The average is 3%. Things are heading in the right direction but again the Reserve Bank will not consider this to be a signal that everything is sweet, and they can start whispering about policy easing soon.

All up, the two sets of survey results from ANZ show a poor outlook for the economy and highlight the way positive business feelings about the government have swamped perceptions of the reality businesses are really facing – especially retailers.

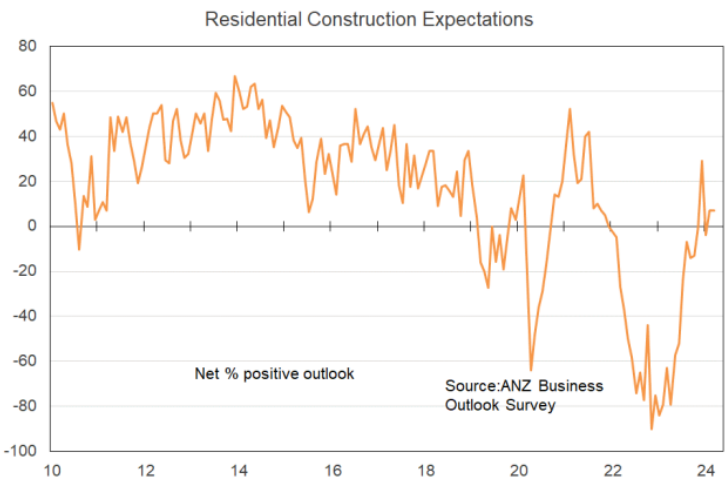

One more thing, a net 7% of builders have a positive outlook for their residential construction. This is up from a net 63% feeling negative a year ago.

The truly depressed activity expectations of a year ago may have been overblown, but the latest positive reading which is almost equal to the 9% long-term average does not gel with the reality being faced by home builders – especially multiunit developers. More liquidations loom.