The AFR is a card-carrying inflationista:

Tim Toohey, chief strategist at Yarra Capital…notes that the United States didn’t see across-the-board price rises in the first three months of the year.

“There’s still a strong disinflationary effect coming through the tradeable goods sector, which largely reflects China’s excess production being pushed through the developed world,” he says.

Toohey notes that rents and imputed rents comprise a bit over 40 per cent of the core US CPI. But, he says, “more real-time measures of rents suggest that what we saw in the first quarter was likely an aberration rather than a new uptrend.”

At a more fundamental level, he says, “the really important driver of inflation in the services sector has been wages.” And, he adds, “while wages growth has clearly moderated, there’s a very noticeable lag before that translates into lower inflation.”

I share that view. Turning to Australia:

Toohey agrees that strong house price increases will influence the Reserve Bank’s decision-making.

“The Reserve Bank has a problem because the country needs more housing supply, but it won’t want to fuel another upswing in housing prices by cutting interest rates too sharply too soon. And I think that will continue to moderate their enthusiasm for rate cuts.”.

…Toohey argues that enormous backlogs in infrastructure and housing are continuing to power the Australian economy, blunting the impact of rate rises.

“There’s been a steep fall in approvals – which is consistent with higher interest rates – but if you look at activity in the housing sector, it’s bobbling around at a high level.”

…“There is still a case to be made for easing monetary policy as inflation falls, but I think we’ll only see two or three rate cuts from the Fed, and the Reserve Bank will only deliver one or two”, says Toohey. “It’s a very shallow interest rate cycle.”

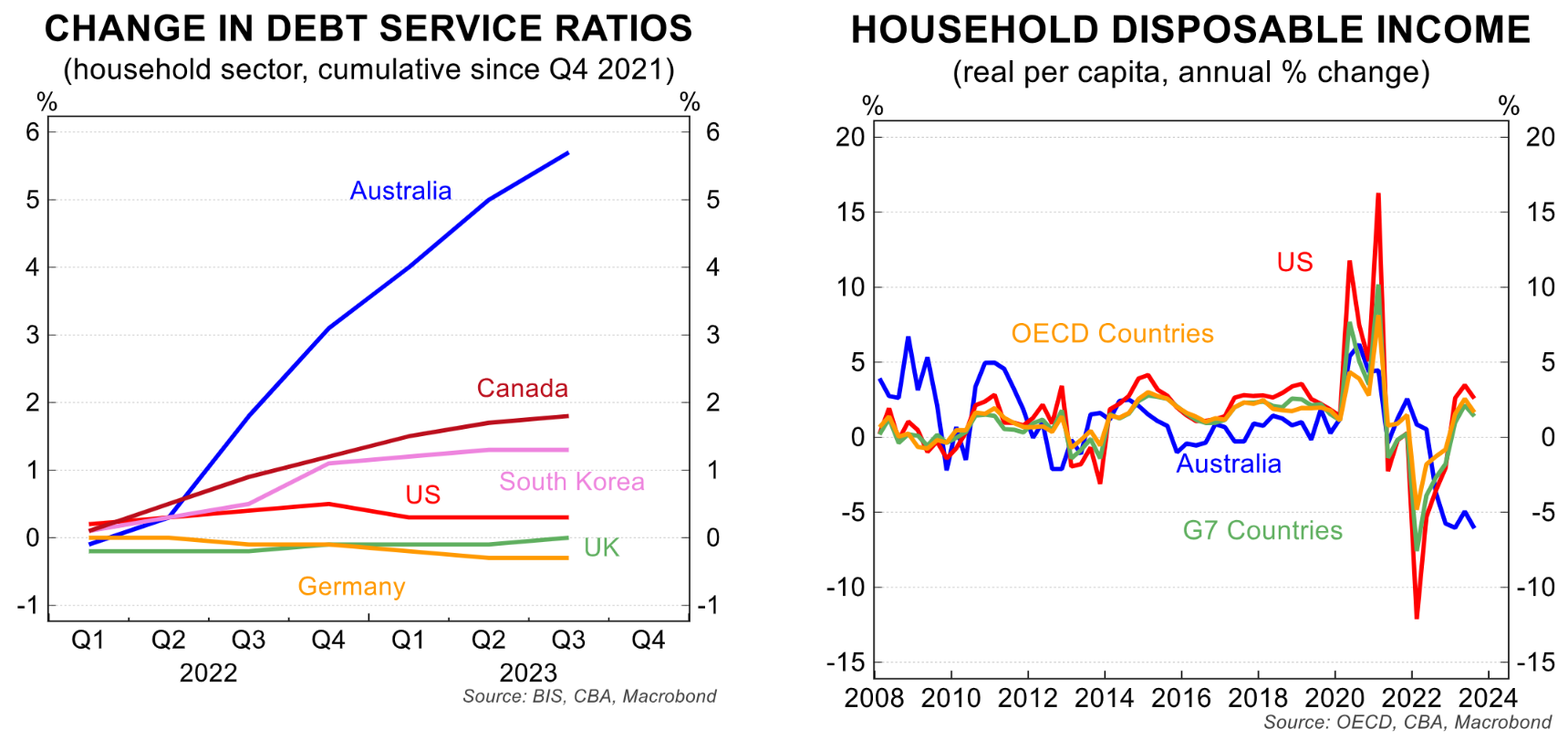

I don’t share that view. Aussie disinflation is still on track. If anything, we have moved ahead of the US because our real incomes never went anywhere near as high and are softening faster, crushing consumption:

Inflation is tumbling via household permarecession:

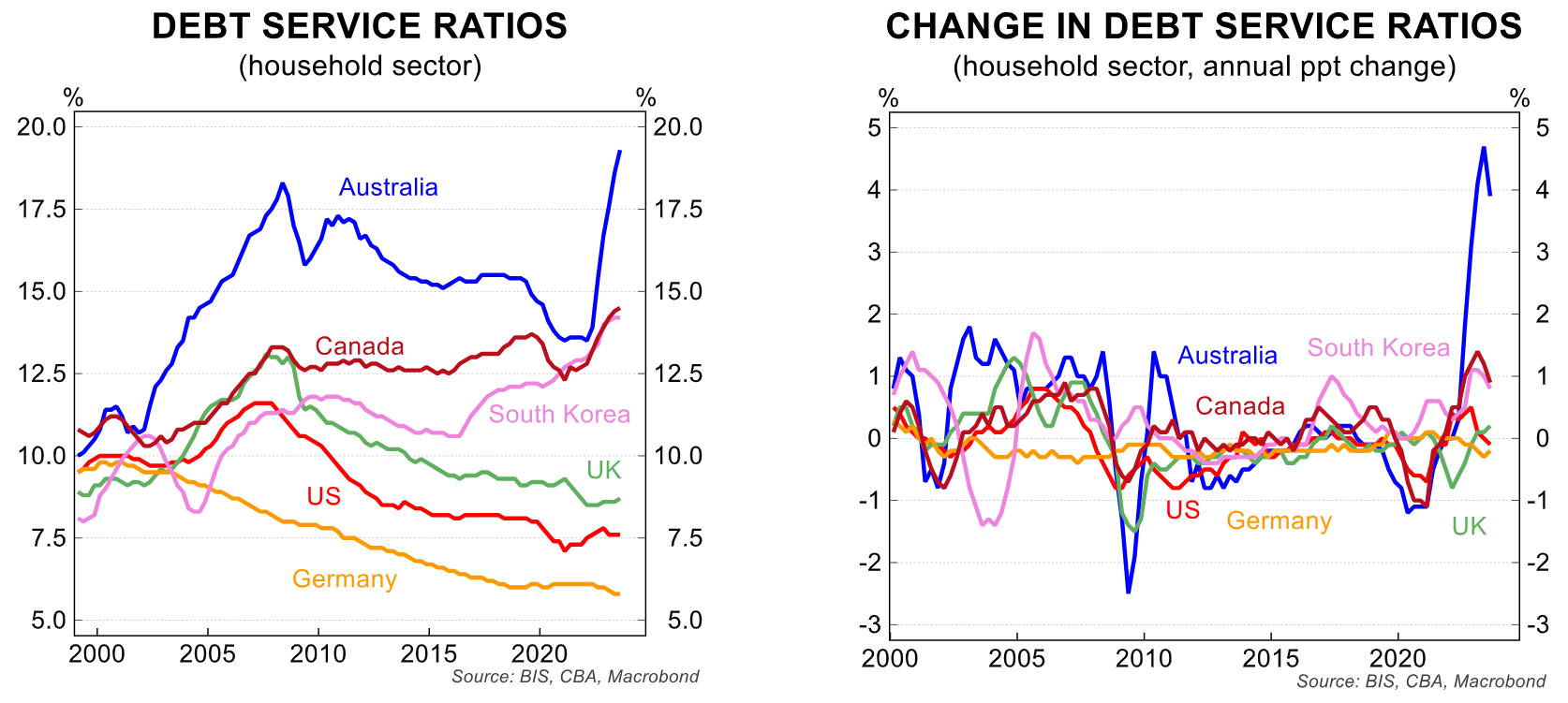

This is a combination of shocking fiscal mismanagement in energy and immigration, sending debt service ratios mad:

The last thing the RBA should be worried about is rising house prices. Except to the extent that they are not rising anywhere fast enough.

The only contribution the RBA can make to disinflating rents—its most persistent inflation problem—is to cut rates hard and skyrocket dwelling prices to reverse the builder bust.

Building approvals are not a problem, but a considerable backlog of starts is growing. The problem with dwelling construction is that the cost of building has increased by 30%, making it uneconomic to build.

Fixed price contracts made before the price spikes are making it worse as builders go bust.

There are only two answers.

Either building input costs come down. Or house prices go up. A lot.

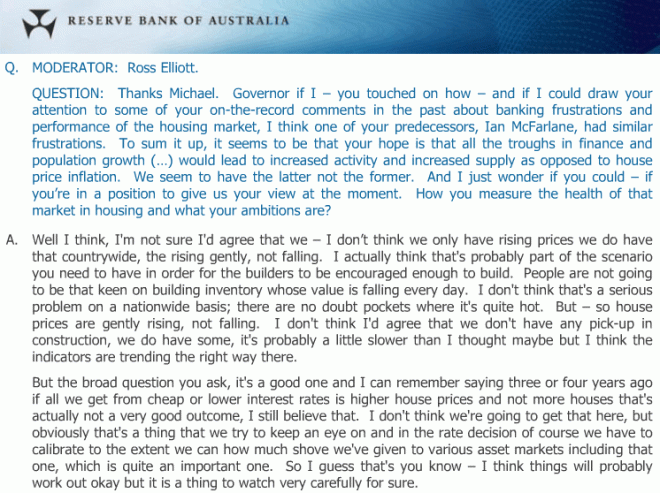

The RBA can only address the latter. As Glenn Stevens once said:

Albo’s profound fiscal mismanagement, most notably the collapsed border with India, will prevent any wage growth or broader service inflation rebound.

Households are so smashed that any consumption relief rally will be muted.