CBA economist, Harry Ottley, has published a terrific statistical report on Australia’s rental market, which unambiguously shows that the unprecedented surge in net overseas migration after the international border was reopened in late 2021 is behind the collapse in the rental vacancy rate and the hyperinflation in rents.

The surge in rents would have been even stronger without the Commonwealth Government increasing rent assistance in last year’s Budget.

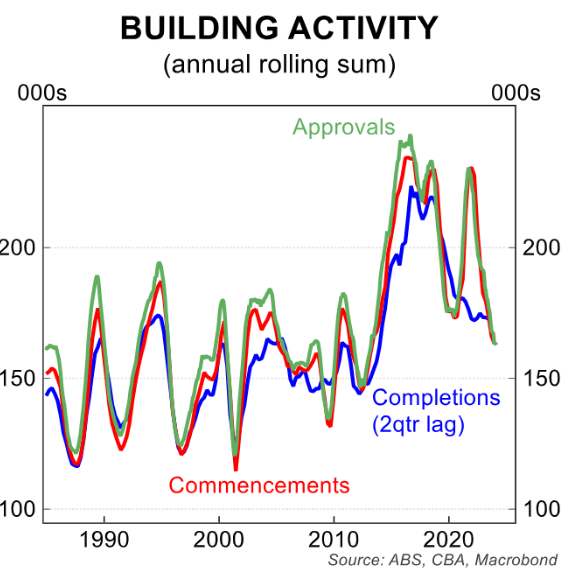

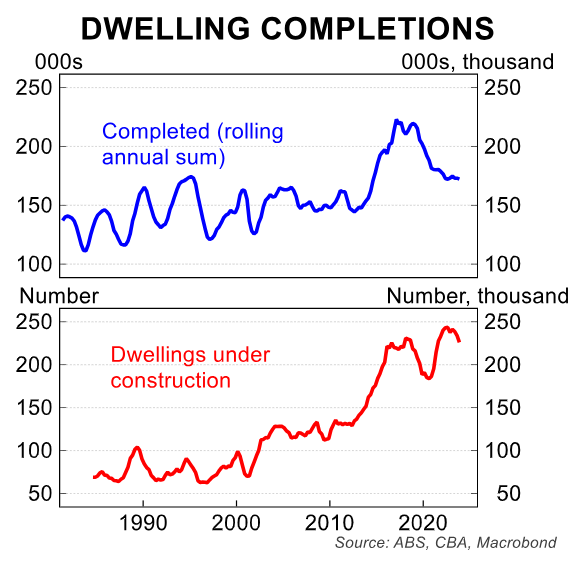

Meanwhile, housing construction in Australia is collapsing, which points to further pain ahead for renters.

Below are key extracts from Harry Ottley’s report on the rental market.

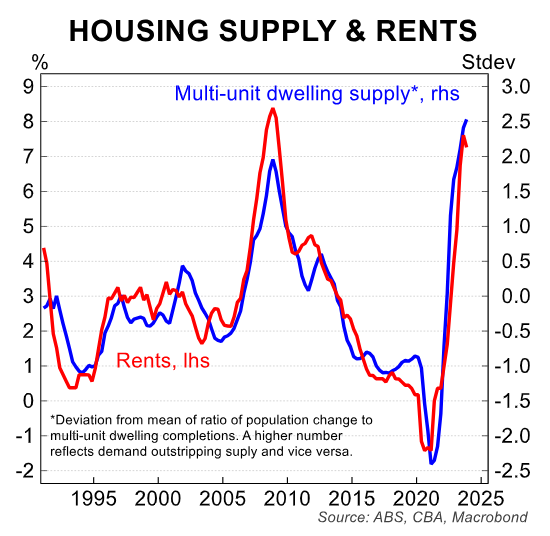

The imbalance between the supply of and demand of dwellings is what primarily drives rent inflation.

Multi-unit dwellings are especially important for the rental market as they house a greater proportion of tenants.

This chart shows the close correlation between the balance of supply (completions) and demand (population growth) in blue and rent inflation in red.

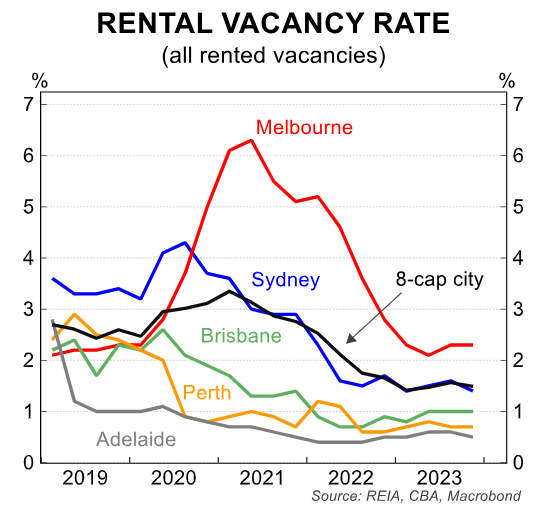

Another way of quantifying this mismatch is through the rental vacancy rate, which remains much lower than prior to the pandemic in most cities.

According to REIA data, rental markets in the smaller capital cities remain tighter than Sydney and Melbourne.

Melbourne and to a lesser extent Sydney saw a rise in vacancy rates during the worst of the pandemic but have since fallen.

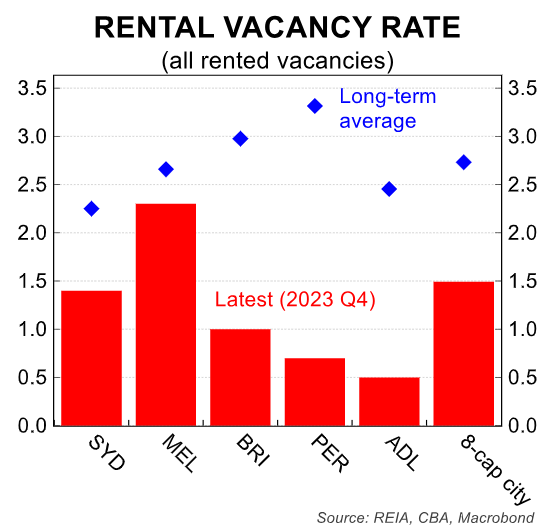

Vacancy rates across the country are much tighter than historical averages.

Adelaide has the lowest capital city vacancy rate in the country at 0.6%, much lower than the long-term average of 2.5%.

Vacancy rates in Sydney (1.4%) and Melbourne (2.3%) remain above the smaller capitals, likely as legacy of interstate emigration out of our largest cities during COVID.

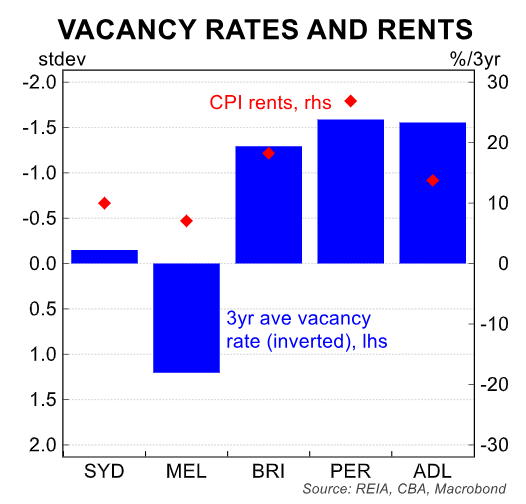

Looking at the relationship between vacancy rates and rents since Q4 20, tight rental markets have been associated with stronger rent price growth.

The tight rental market in Adelaide has not created as much price pressure as in Brisbane and Perth despite advertised rents growth having been very strong.

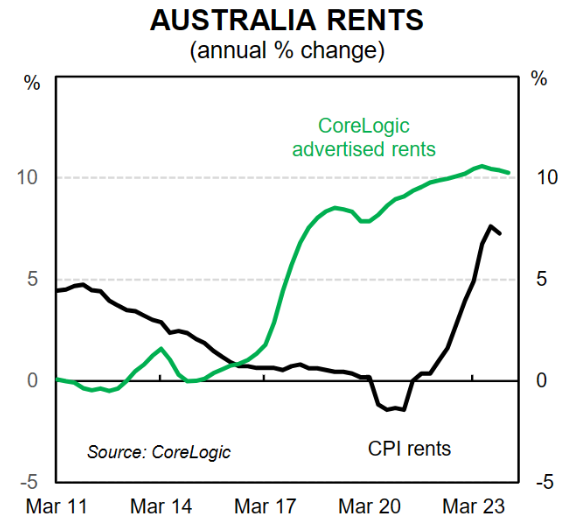

While not a perfect relationship, advertised rents are typically a leading indicator of rents inflation…

Australia wide, advertised rents are broadly tracking sideways indicating rents inflation is likely to remain elevated in the near term.

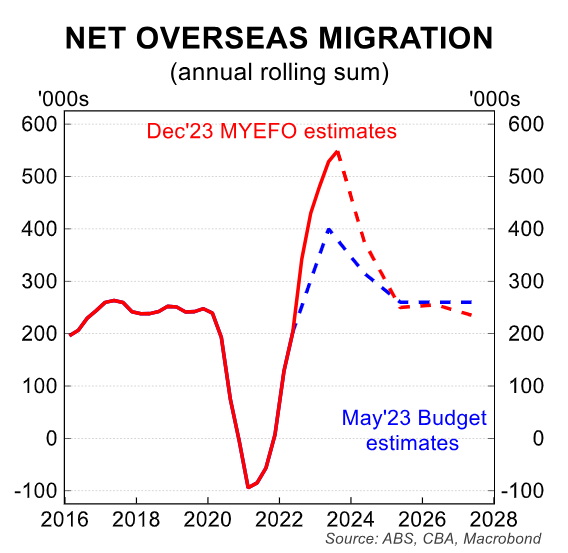

However, population growth is expected to ease in 2024 owing to lower net overseas migration.

This should see the rental market cool and price gains easing. A forecast monetary policy easing cycle should also stimulate dwelling supply.

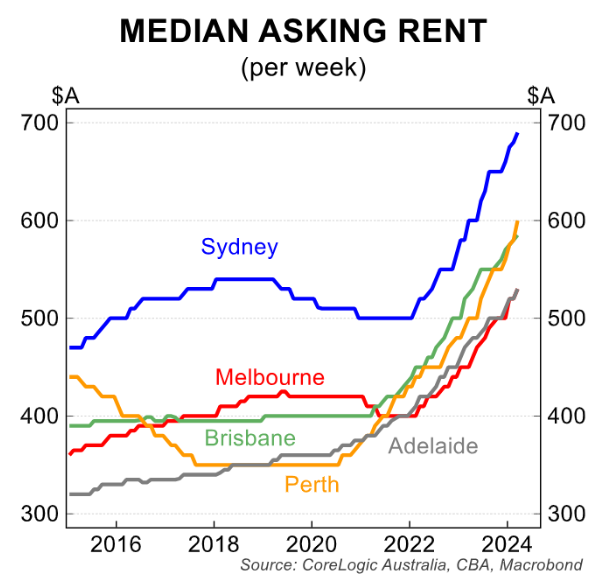

Median asking rents remain highest in Sydney according to CoreLogic.

The median rental in the harbour city will cost you $690/pw.

Next most expensive is Perth at $600 following exceptional growth in recent years.

Brisbane ($585) is next most expensive while Melbourne is now equal lowest with Adelaide (both $530) of the five major cities.

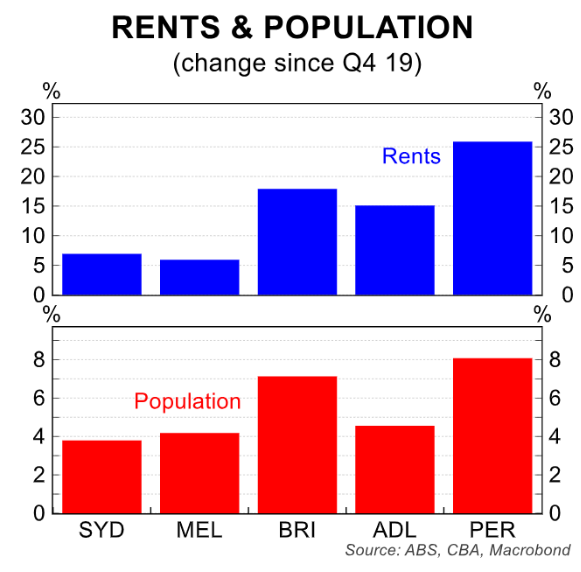

Since the beginning of the pandemic, rents inflation has been much stronger in the smaller capitals.

This has been primarily due to stronger population growth, especially in Perth and Brisbane.

There were large outflows from Sydney and Melbourne during COVID.

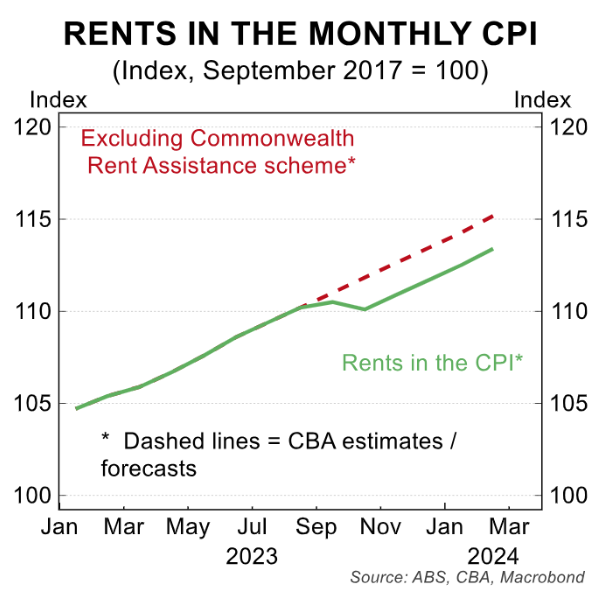

Rents inflation would have been ever stronger without the Commonwealth Government increasing rent assistance in last year’s Budget.

The increased CRA payment reduced measured inflation and is the reason many cities saw a reduction in annual growth rates in Q4 23.

Strong population growth has driven strong demand, but the supply of housing has not kept up, which has also contributed to the tight market.

The most recent spike in starts has not translated to a rise in completions due to constraints in the construction sector.

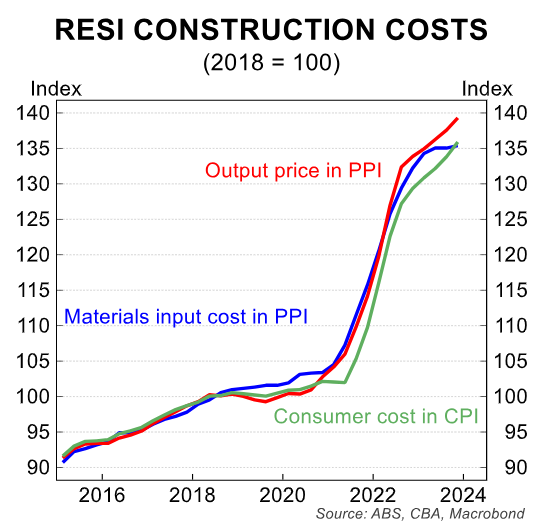

Capacity constraints around labour and materials have delayed projects and driven construction costs higher.

PPI and CPI measurements have risen ~40% over the past three years.

While builders are passing on costs, many suffered profitability challenges due to the sudden spike in input costs.

Not enough already commenced dwellings are being completed due to these constraints in the sector.

These factors are also combining with restrictive monetary policy to stifle near term activity.

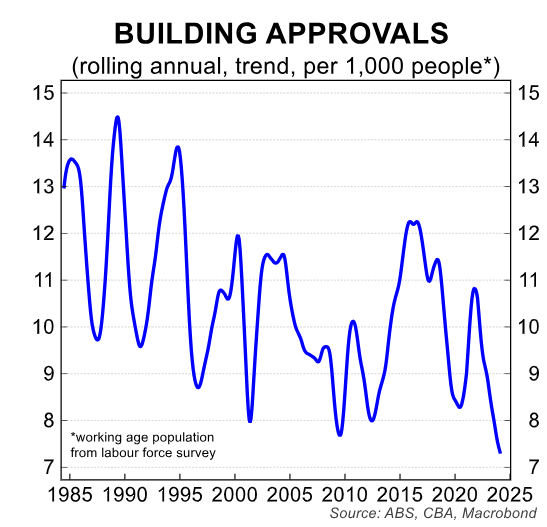

Building approvals are around decade lows on aggregate and at record lows per-capita.

Looking ahead, the outlook for population growth and building activity is key.

On the supply side, the federal government forecast an easing in net overseas migration from 530,000 in FY23 to 375,000 in FY24 and 250,000 in FY25. This will reduce demand growth for rentals as most international migrants enter the rental market on arrival.

There is risk that the population will not come down as quickly as government forecasts suggest with Q3 2023 NOM a large ~145,000.

On the supply side, we would expect completions to remain around current levels as the large pipeline of dwellings under construction is worked through.

In terms of commencements, we expect commencements to rise marginally from 164,000 in 2023 to 170,000 in 2024 though there is downside risk to this forecast given the recent weak approvals numbers.

Given this expected robust fall in demand and more stable supply, rents inflation is likely to ease from very high levels though progress will likely be slow.