Goldman with the note.

USD: Still living in a Dollar world. As we wrote in our 202 3Outlook, the key risk to our baseline forecast of more balanced growth and gradual, modest Dollar depreciation is that continued US outperformance complicates the Fed policy path and, more importantly, Dollar assets could continue to offer superior total returns that would boost demand for the currency.

As we move into the second quarter, that risk has moved into sharper relief with ongoing upgrades to our already-robust US growth forecasts that give the FOMC the luxury of a later and more gradual policy adjustment.

While our global policy forecasts have also shifted somewhat since the start of the year, our economists still expect that policymakers in most other developed market economies will begin the cycle sooner with sequential rate cuts.

This opens some policy divergence in our baseline outlook, which leans in the direction of a “stronger for longer” US Dollar.

Importantly for FX, the rate cuts we anticipate are unlikely to be significantly negative for the Dollar because they are unlikely to erode the Dollar’s position as a relatively high carry, safe-haven currency with strong capital return prospects.

The upcoming US election should also start to impact currencymarkets more directly, at least by limiting portfolio flows to other jurisdictions when both candidates have proposed more fiscal support and trade restrictions.

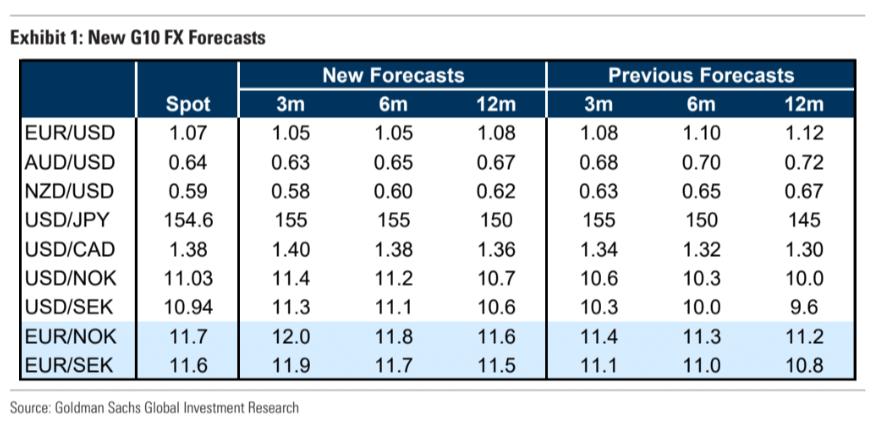

As a result, we are making a number of adjustments to our FX forecasts.