Another mixed trading session across stock markets in Asia today with the fallout of Fitch’s re-rating of China’s outlook to negative impacting domestic shares while local markets are putting in mild upticks despite the flat result on Wall Street overnight. Risk sentiment is fragile going into tonight’s US CPI print which follows on from Friday’s US jobs report, which came in hotter than expected. The USD is continuing to slip further and becoming weaker against most of the majors as the Australian dollar pushes further above the 66 cent level.

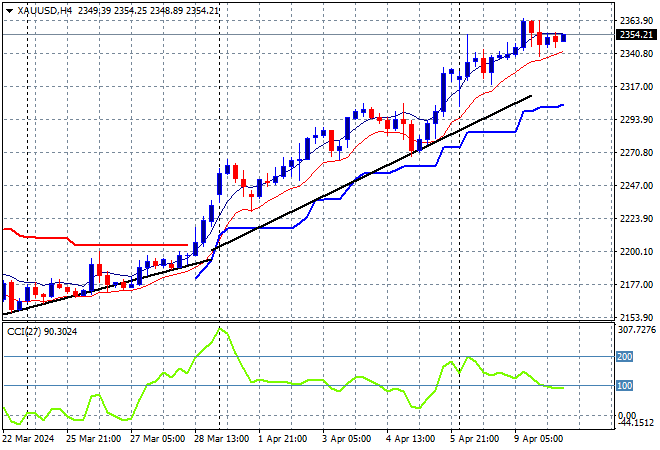

Oil prices have pulled back from their pre-weekend exuberance that took Brent crude well above previous weekly resistance at the $91USD per barrel level but are holding at the $89 level while gold is having a very minor slowdown, currently at the $2354USD per ounce level:

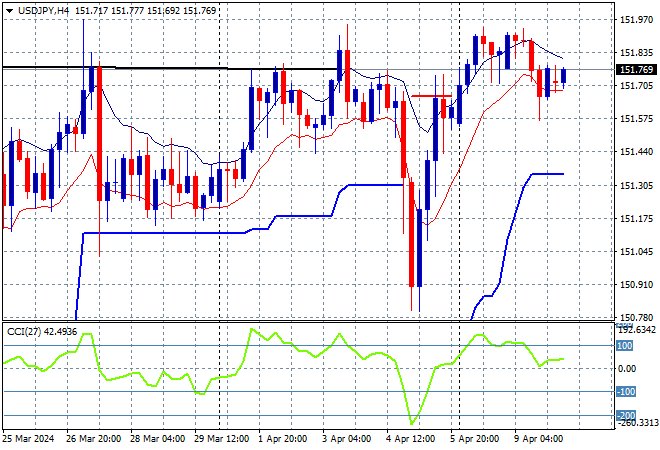

Mainland and offshore Chinese share markets are again diverging with the Shanghai Composite down more than 0.3% while the Hang Seng Index is rebounding even further, currently up more than 1.8% to 17144 points. Japanese stock markets however failed to continue its previous rebound with the Nikkei 225 down 0.3% at 39626 points with the USDJPY pair getting back on track but not yet exceeding the recent weekly highs:

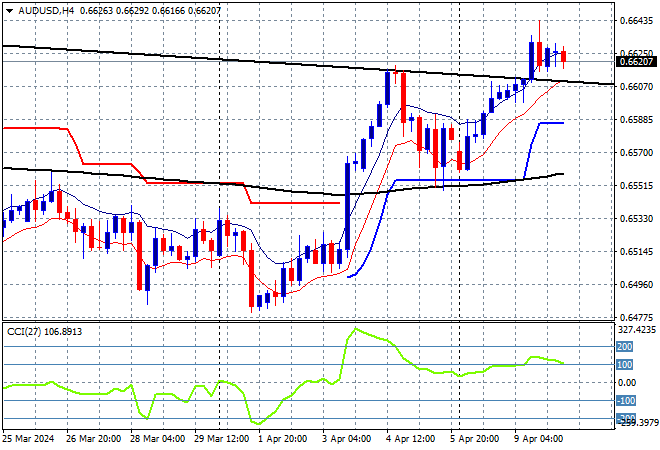

Australian stocks had another fairly solid session with the ASX200 about to close 0.3% higher to 7847 points while the Australian dollar is trying to match its recent weekly high as it again tries to breakout out above the 66 cent level:

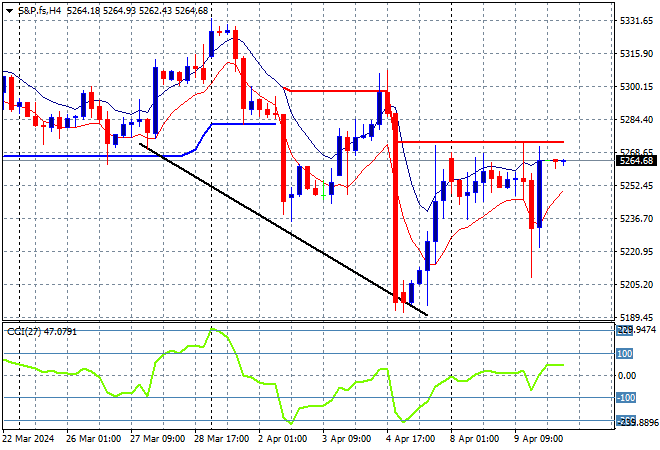

S&P and Eurostoxx futures are fairly flat as we head into the London session with European shares not likely to rise on the open while the S&P500 four hourly chart shows price action still in a technical downtrend as it stalls out:

The economic calendar ramps up tonight with the latest US core inflation figures, followed by the BOC interest rate meeting and Fed minutes released.