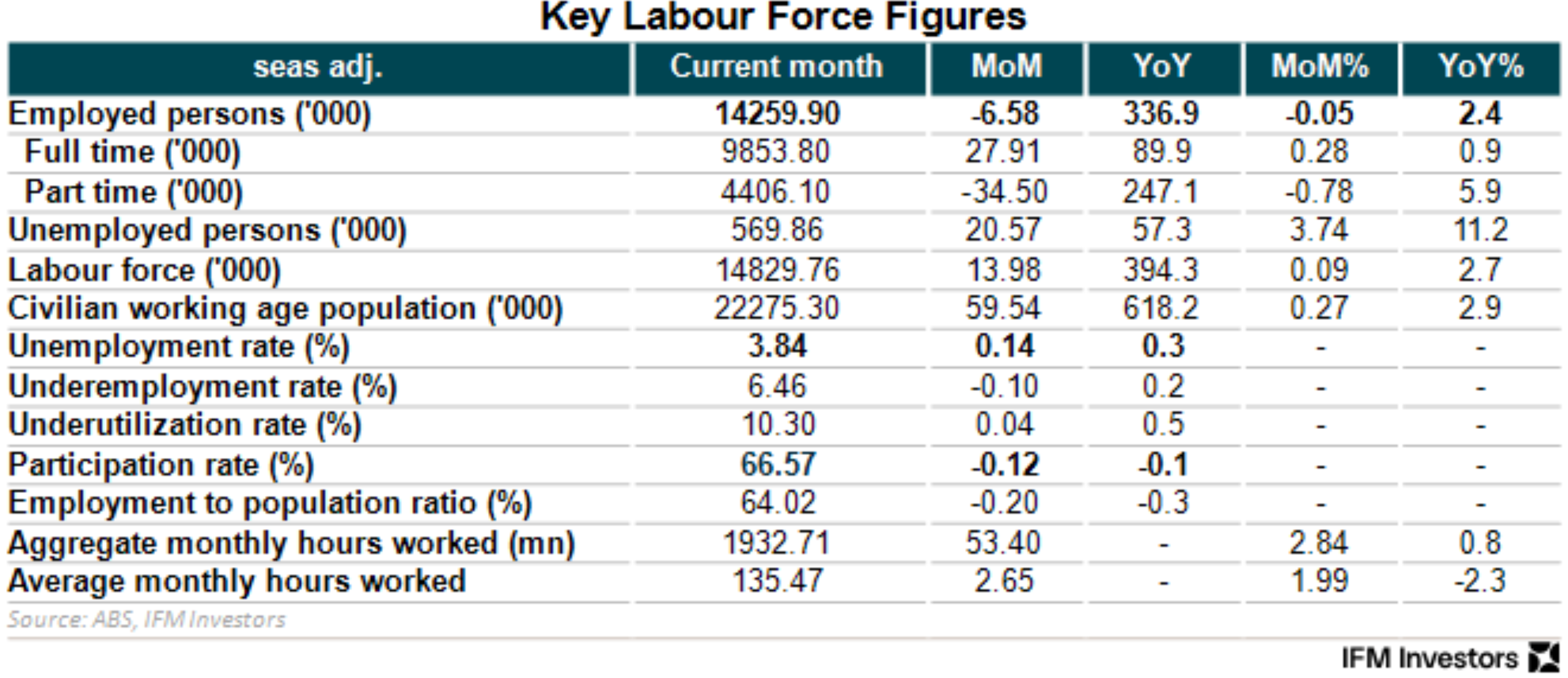

The Australian Bureau of Statistics (ABS) has released labour market data for March, which shows that the nation’s unemployment rate rose by 0.1% to 3.8% following a 6.,600 contraction in the number of jobs:

Source: Alex Joiner

The result beat analysts’ expectations of a 3.9% rate.

The underemployment rate also fell by 0.1% over the month to 6.5%, whereas hours worked also rose.

Source: Alex Joiner

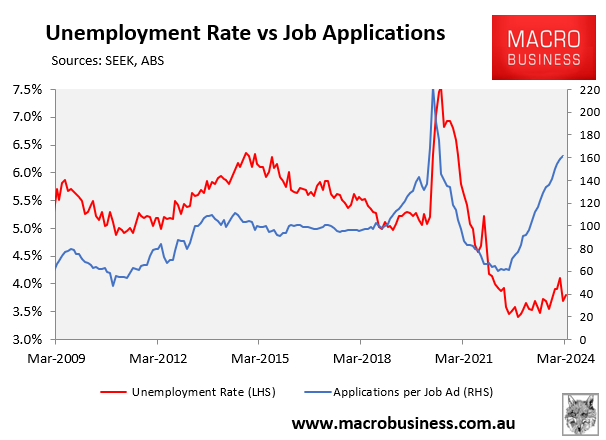

The official ABS data continues to fly in the face of other labour market data and the broader economy, which is mired in a per capita recession.

The number of applicants per job ad has soared, which would typically correspond with higher unemployment:

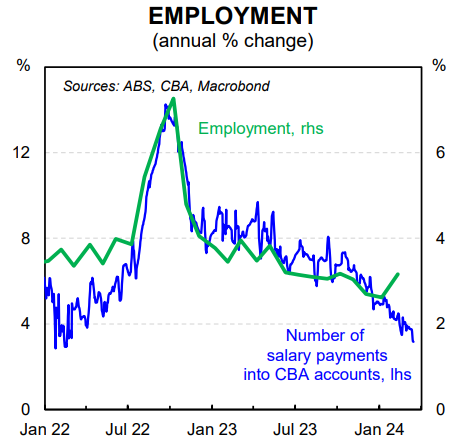

The number of salary payments into CBA bank accounts also suggests that job growth should have fallen sharply, not risen as reported by the ABS:

As noted by the Financial Times earlier this month, official data produced by government statistical agencies are likely understating the weakness of labour markets and giving false signals to central banks.

“Employment figures are being closely watched by central bankers around the world as they try to work out when to cut interest rates this year. There is just one problem: the data might be dodgy”, the article reads.

“Swings in immigration, rapid changes to working conditions in the wake of the pandemic and lower participation in polls are combining to create a big problem for labour market statisticians”.

“Economists are increasingly questioning whether official reports can be relied upon for an accurate read of the labour market”…

“Economists and policymakers in the UK and US are doing their best to patch together a coherent view of their labour markets by looking at a broader range of surveys and alternative data”, the article says.

Maybe the ABS survey is unable to accurately track the record numbers of migrants landing in Australia and is thereby producing false figures.

Hopefully, the Reserve Bank of Australia (RBA) has discounted the official ABS data in favour of broader and alternative measures. Because they simply do not seem realistic.