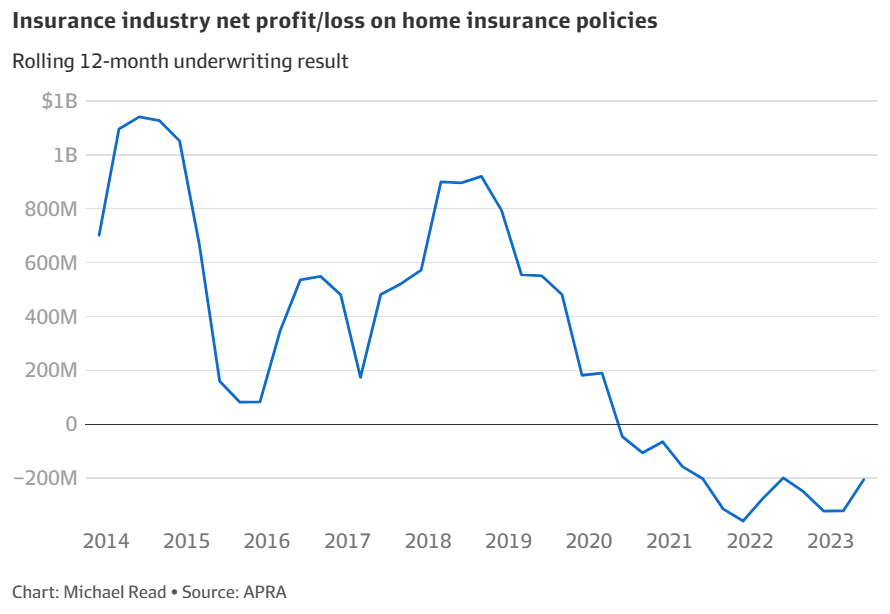

The AFR’s Michael Read reported that Australian insurers lost more than $650 million on home insurance policies over the past four years despite soaring premiums.

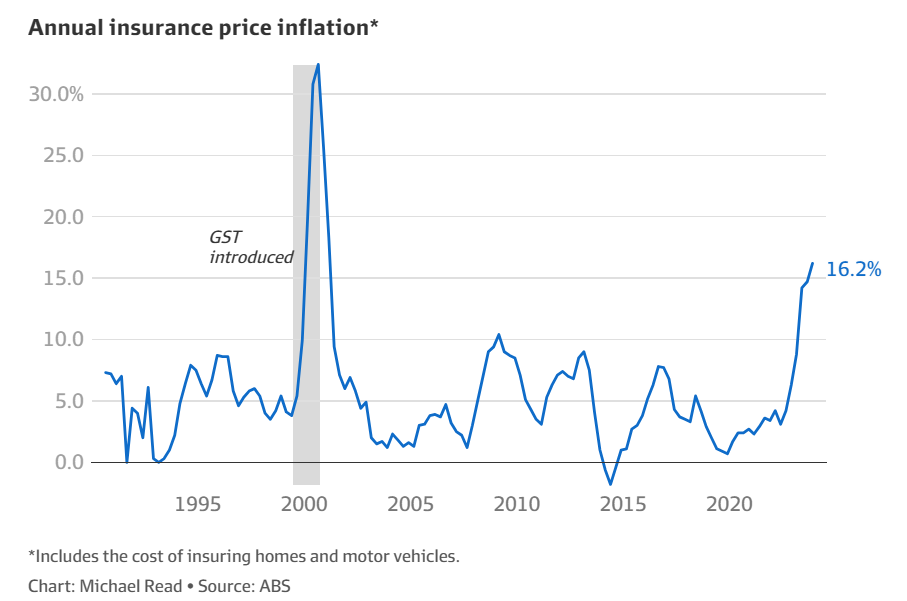

As illustrated in the next chart, insurance premiums soared by 16.2% last year—the fastest rate of growth since HIH Insurance collapsed in 2000:

The Australian Bureau of Statistics (ABS) explained that “higher reinsurance, natural disaster and claims costs contributed to higher premiums for house, home contents and motor vehicle insurance”.

Allianz told a parliamentary economics committee that it had increased average premiums across its household portfolio by a cumulative 56% between 2020 and 2023.

This surge in premiums “meant 12% of Australian households were now “affordability stressed”, meaning 1.24 million spent more than four weeks of income on home insurance premiums, the Actuaries Institute estimates”.

Experts believe that climate change is increasing the frequency of costly natural disasters such as floods and cyclones, putting upward pressure on insurance premiums.

These rising premiums are impacting poorer households that are least able to afford insurance.

“This phenomenon is already occurring in parts of northern Australia where, on average, home insurance premiums are almost double that of the rest of Australia”, Philip Kewin, chief executive of the National Insurance Brokers Association of Australia, told the parliamentary committee.

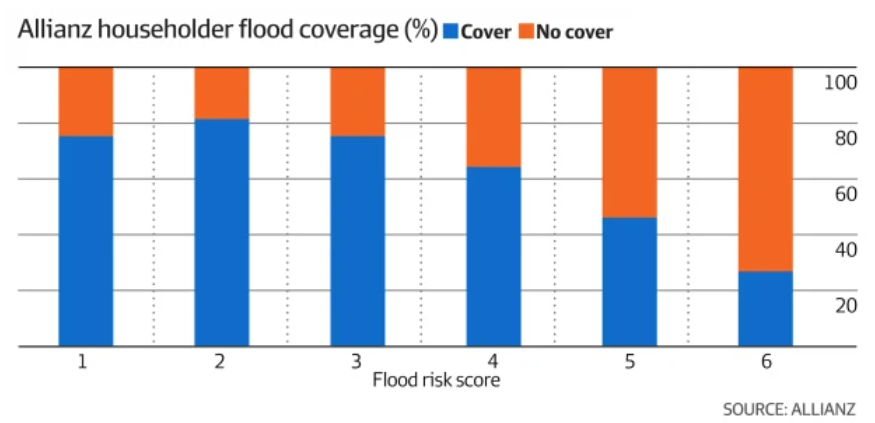

Allianz likewise told the committee via a submission that three-quarters of its policyholders that were most susceptible to flooding did not purchase flood cover.

“For some highly exposed communities, such as in the northern NSW region impacted by [2022 NSW and South-East Queensland floods], around 90% of customers do not purchase flood cover”, Allianz said.

“These figures indicate that the vast majority of homeowners exposed to material flood risk are non-insured or underinsured and, in most cases, the reason is because they cannot afford the flood premium”.

Soaring insurance premiums are also putting upward pressure on CPI inflation, making it harder for the RBA to bring inflation back to target.

Former Australian Competition & Consumer Commission (ACCC) chair Allan Fels last month called for the ACCC to investigate the insurance sector over its recent hike in premiums.

“There is massive public discontent with the rise in insurance premiums and a deep concern they greatly exceed inflation”, Fels said.

“The price rises seem excessive in comparison with increases in costs and risks and seem exploitative of consumers and small businesses in particular”.

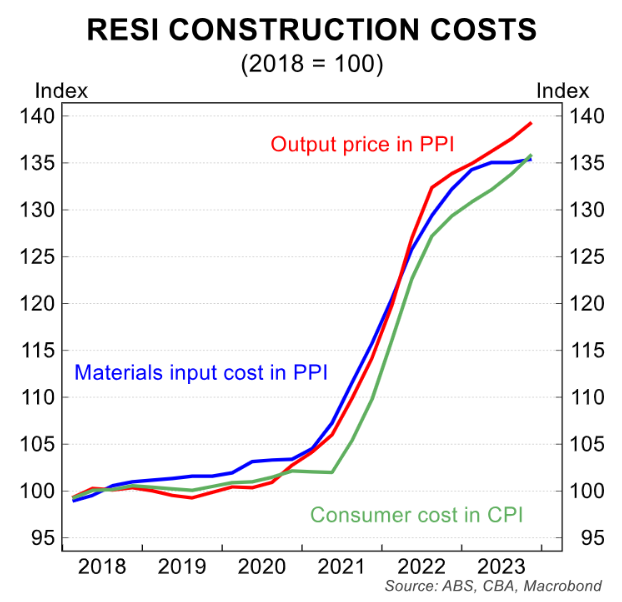

Building insurance costs have also surged, increasing the industry’s woes and threatening to reduce the supply of new homes.

For example, the Herald-Sun reported that “Victorians will be slugged with a 43% increase to Domestic Building Insurance as the home building industry continues to feel the strain of surging cost and company collapses”.

This is on top of the recent hyperinflation of broader residential construction costs:

Rising insurance costs have, therefore, become a fresh thorn in the RBA’s side, putting upward pressure on inflation.

They are also adding fuel to the cost-of-living crisis and posing another impediment to the Albanese government’s housing construction targets.