By Stephen Wu, Economist at CBA:

- We expect headline CPI increased by 0.7%/qtr and 3.4%/yr in Q1 24.

- Our forecast sees the trimmed mean CPI rise by 0.8%/qtr and the annual rate step down to 3.7%.

- An outcome in line with our forecasts would imply a slight undershoot relative to the RBA’s expectations.

The upcoming Q1 24 CPI will be key ahead of next month’s May RBA Board meeting (6-7/5).

These inflation figures will feed into the RBA’s new cut of their economic forecasts (alongside the March labour force report, due 18/4), which will be shown to the RBA Board ahead of their deliberations and published in the May Statement on Monetary Policy.

We expect price rises in Q1 24 slightly undershot relative to the RBA’s forecasts from February.

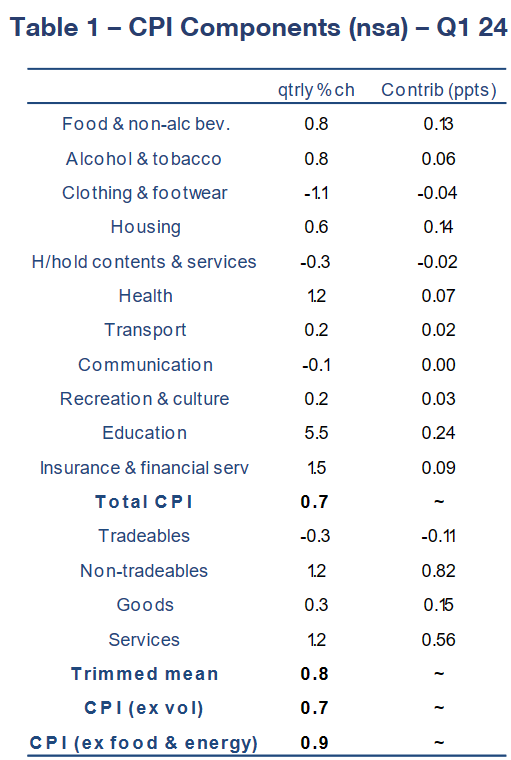

For context, the RBA’s implied profile is a headline annual rate of 3.5% and a trimmed mean rate of 3.8%.We forecast headline CPI rose by 0.7%/qtr and 3.4%/yr while the trimmed mean CPI increased by 0.8%/qtr and 3.7%/yr in the March quarter.

These numbers are little changed relative to our earlier forecasts; we have nudged down our quarterly headline CPI forecast after February’s CPI indicator downside surprise.

Our forecast for core inflation over the March quarter is unchanged.

It’s worth calling out a few key components of the CPI basket driving outcomes in Q1 24.

Education (4.3% weight in the basket): Large price increases have already been telegraphed in the February CPI indicator, particularly for secondary and tertiary education, which were up by more than 6%/qtr. Strong wage gains for teachers are a factor.

Rents (6.0% weight in basket): We expect quarterly growth accelerated to 2.3% as the impact of the increase in rent assistance washes through. We anticipate the current monthly run rate of 0.7-0.8% to slow, albeit gradually, over 2024 as the imbalance between rental demand and supply improves a little and vacancy rates lift modestly from near-record lows.

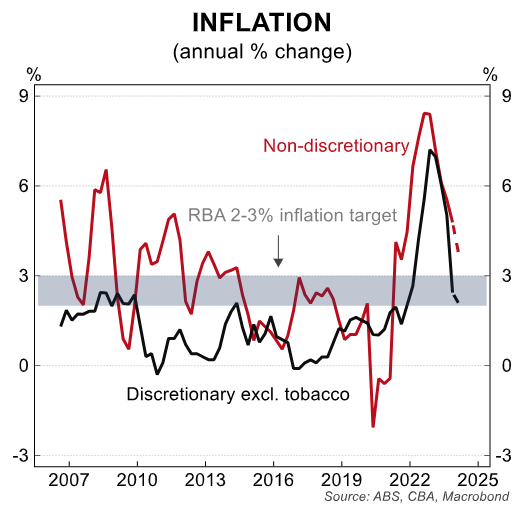

While some recent discussion has focussed on the goods and services split, we view the more relevant theme is the distinction between discretionary and non-discretionary inflation.

We expect discretionary (excluding tobacco) inflation moderated further to 2.2%/yr as demand has continued to weaken.

Our forecasts do imply an increase in the quarterly pace of headline CPI inflation.

In the December quarter last year, the CPI rose by 0.6%/qtr. But the softer-than-expected Q4 23 inflation print in part reflected the temporary impact of the increase in rent assistance, lowering overall inflation by ~0.1ppts. And the Q1 24 figure will be boosted by~0.2ppts from the annual increase in education.

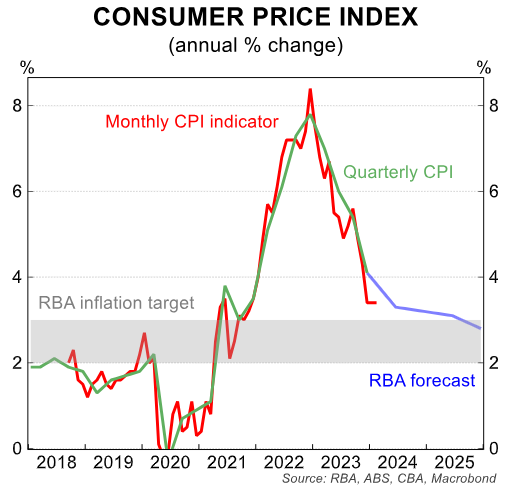

It’s worth nothing that on our forecasts, the six-month annualised rate for headline CPI (not seasonally adjusted) will have moderated to 2.7%, i.e. within the RBA’s inflation target.

A recap of recent inflation data:

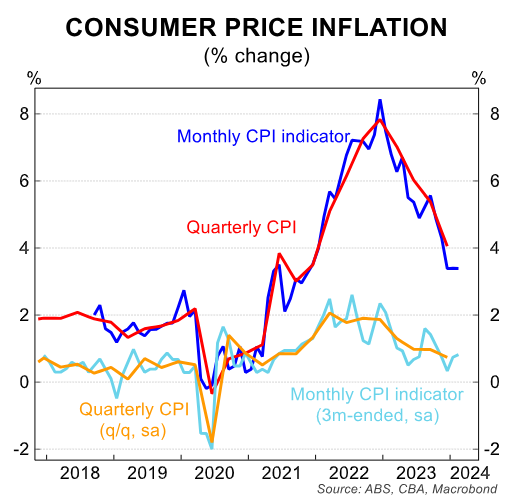

In Q4 23, the headline CPI increased by 0.6%/qtr (0.7%/qtr in seasonally adjusted terms for an annualised rate of 3.0%).

The trimmed mean CPI rose by 0.8%/qtr, or a 3.1% annualised pace. That was a clear downside surprise relative to market and the RBA’s expectations. And since then, the monthly CPI indicator figures for both January and February have also surprised to the downside.

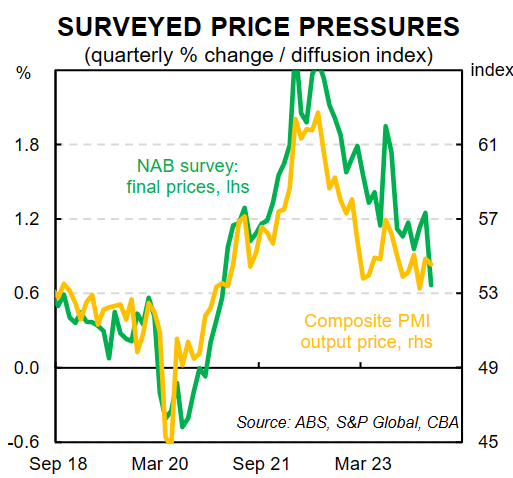

The monthly indicator has remained steady at 3.4%/yr since December last year. Surveyed measures of inflation also point to more modest price pressures than before. Output prices in the Judo Bank / S&P Global Australia PMIs and final price growth in the NAB Business Survey have both moderated over the first three months of 2024.

These surveyed indicators of inflation suggest underlying inflation continued to moderate and lowers the chance for an upside surprise for Q1 24.

However, administered prices and health care price inflation present some upside risk (these are typically only measured in the last month of the quarter and there are few partial indicators from other sources available).

We expect inflation in Australia will not follow the recent path of the US because monetary policy is much more direct and potent here.

The details:

We expect to see the annual rate of inflation decline across both goods and services.

We expect goods inflation to be just below 3%/yr (from 3.8%) but services inflation to be around 4.1%/yr (from 4.6%).

Tradeable inflation on our estimate fell in the quarter to be around 0.9%/yr. And non-tradable inflation we forecast eased to 4.8%/yr from 5.4%/yr.

As we’ve noted above and previously, however, we think that the best way to capture the current inflation themes is through the split between discretionary and non-discretionary inflation.

On that front, we anticipate discretionary inflation fell further in Q1 24, to near the bottom of the RBA’s inflation band.

In contrast, non-discretionary inflation, while declining, is still much higher than desired.

Housing, education, and insurance & financial services are the key drivers.

Our detailed forecasts for the Q1 24 CPI are shown in the facing table:

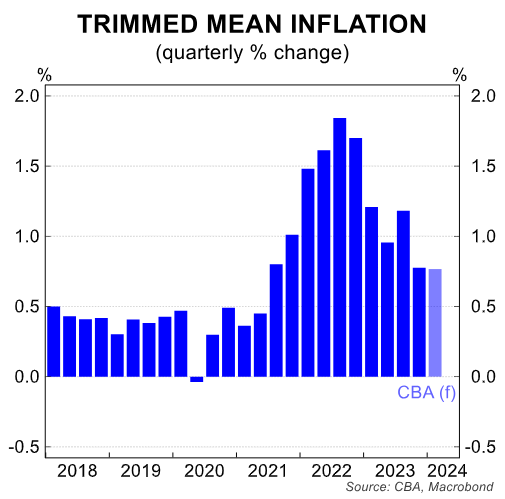

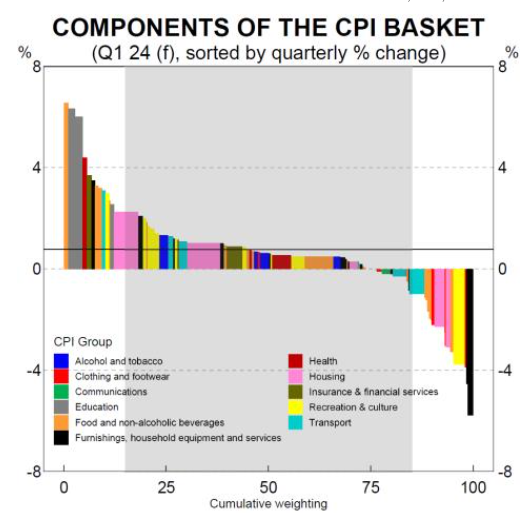

Our bottom-up forecast indicates trimmed mean CPI increased by 0.8%/qtr (see below chart).

Large price rises for some food items, education, pharmaceuticals, insurance, childcare and rents make up the top 15% of the basket and will be trimmed out.

Forecast price declines for household goods, utilities, fuel, and international travel should also be trimmed out.