Aussie mortgage rates will continue rising

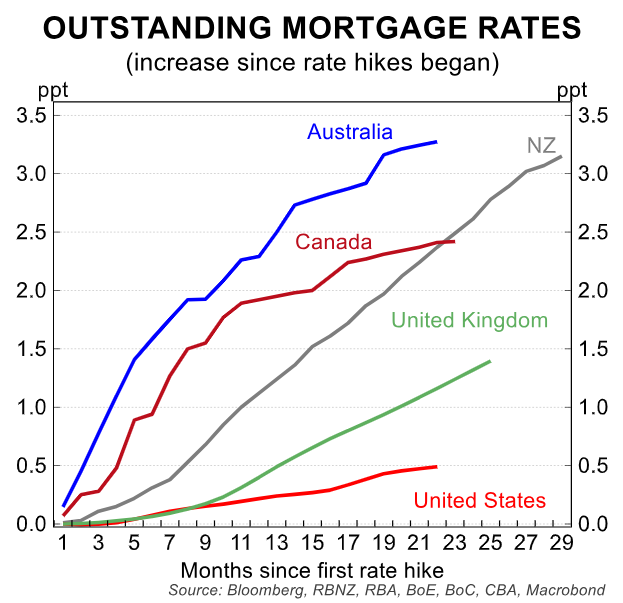

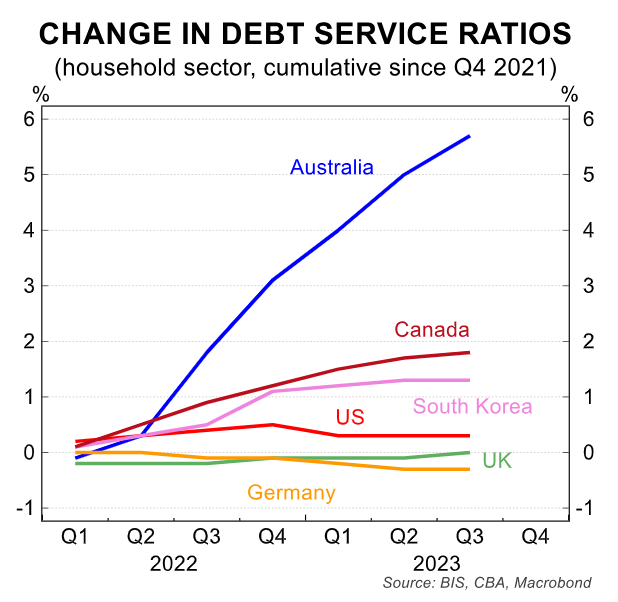

Australian households have already been hit harder than almost anywhere else by rising mortgage rates:

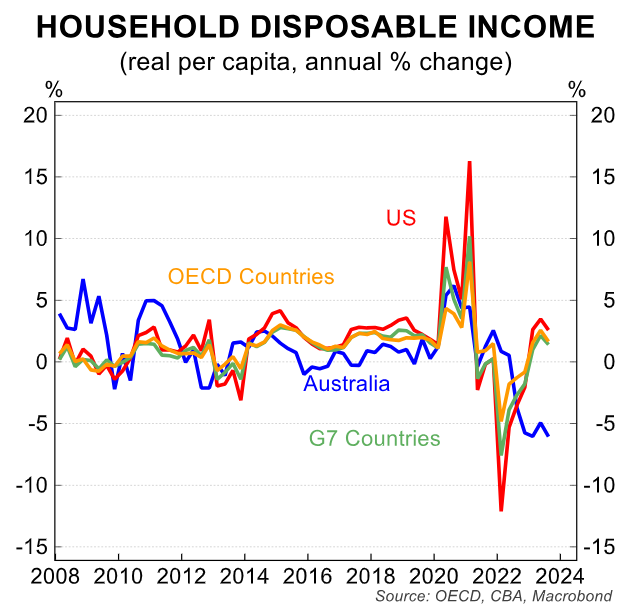

This surge in debt servicing costs has helped drive a record decline in Australian household disposable income:

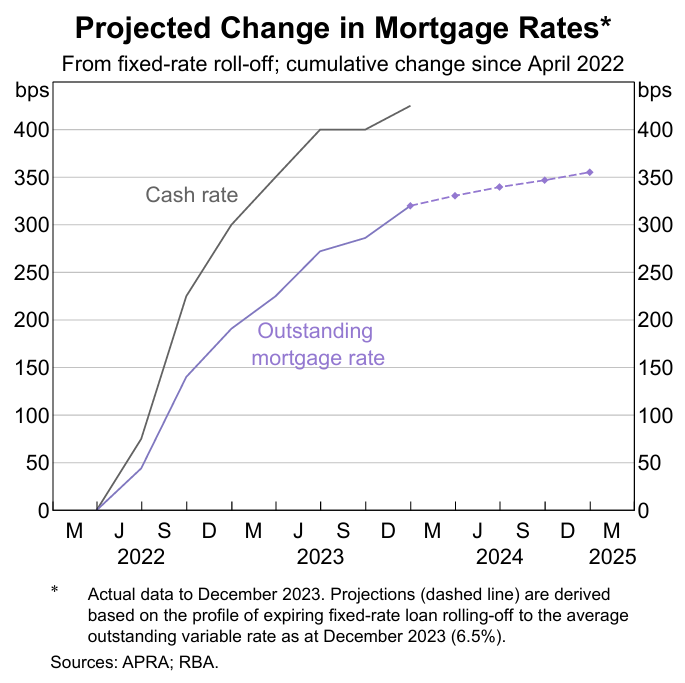

Analysis by Reserve Bank of Australia (RBA) economist Benjamin Ung notes that the proportion of home loans with fixed interest rates peaked at nearly 40% in early 2022, as home-buyers capitalised on historically low rates. This compares with about 20% prior to the pandemic.

The bulk of these loans have now been rolled over to variable interest rates, although about 250,000 are slated to do so by the end of 2024.

Ung’s analysis suggests that the ongoing shift to variable rates will result in the average mortgage rate rising by an additional 0.35 percentage points in 2024, regardless of whether official interest rates are increased again.

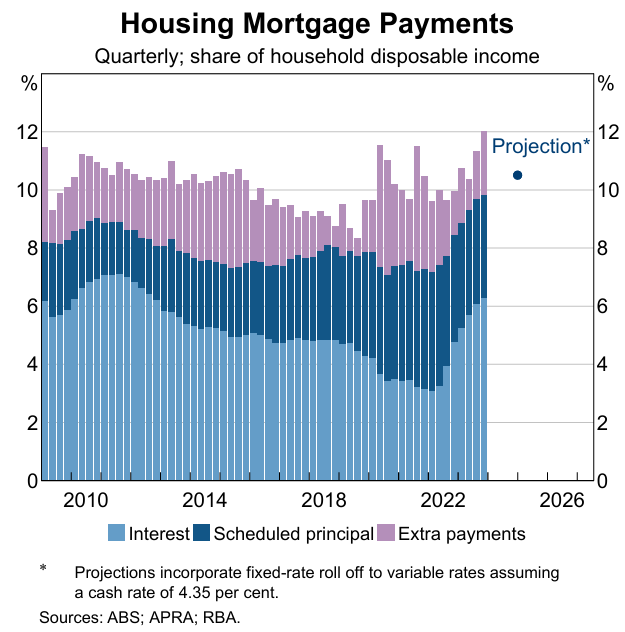

Ung also notes that mortgage repayments will rise to a new record high share of household disposable income in 2024:

“Total scheduled household mortgage payments (comprising both interest and scheduled principal payments) have increased to around 10% of household disposable income as of December 2023, exceeding the estimated previous historical peak in 2008”.

“These scheduled mortgage payments are expected to increase further to reach around 10.5% of household disposable income by end-2024 as more fixed-rate loans expire and reprice at higher interest rates”.

Therefore, Australian monetary policy will continue to tighten without further rate hikes from the RBA.

If you want to save thousands of dollars in mortgage repayments, try the MB Compare n Save mortgage comparison tool. It takes less than a minute.

And if you choose to refinance, Compare n Save will handle the process.