Aussie interest rate debate enters Twilight Zone

Challenger chief economist Jonathan Kearns believes Australia will be the last advanced nation to cut interest rates because the Reserve Bank of Australia (RBA) didn’t lift them as high as other nations.

“Monetary policy was less tight in Australia than it was in other countries, and so therefore the disinflationary impetus coming from monetary policy has been less”, Kearns said.

“Inflation is largely services-driven now”.

“If you think about wage growth in Australia [4.2%] and productivity growth, based on that, inflation is not coming back down to 2.5% unless we get a fairly significant slowing in wages growth or increasing productivity growth.”

Economists also raised concern that stronger-than-expected US inflation figures could mean local prices continue to rise rapidly.

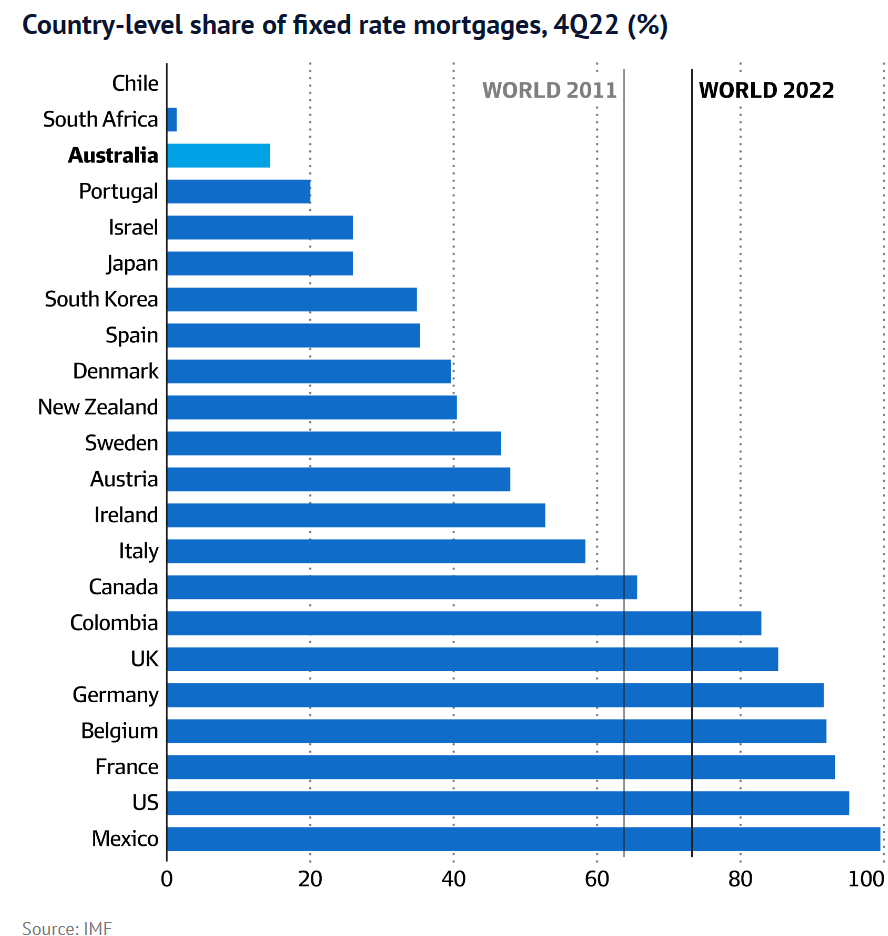

How can Kearns claim that Australia’s monetary policy is less tight when we have one of the highest shares of variable-rate mortgages in the world:

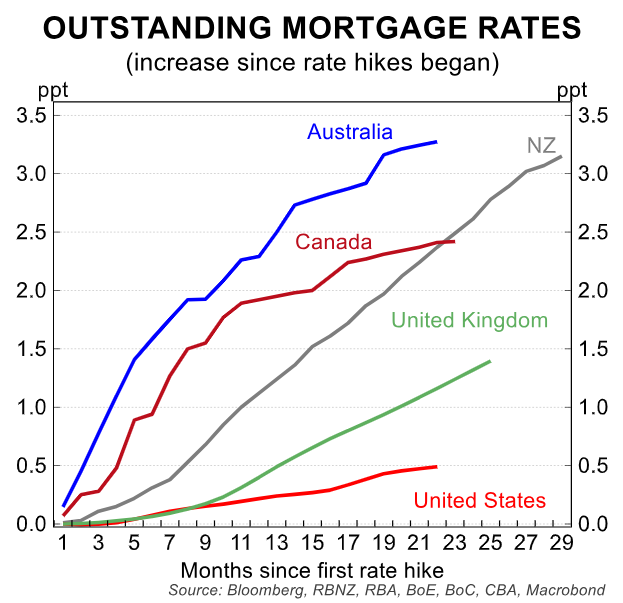

This high variable rate mortgage share has meant that outstanding mortgage rates have risen by more in Australia than elsewhere:

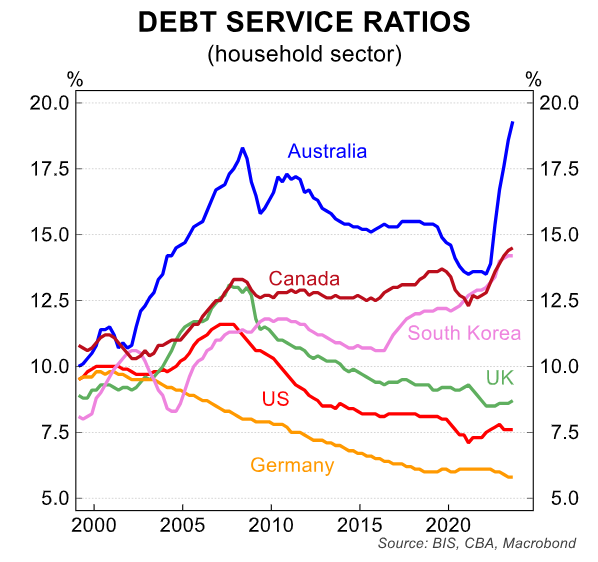

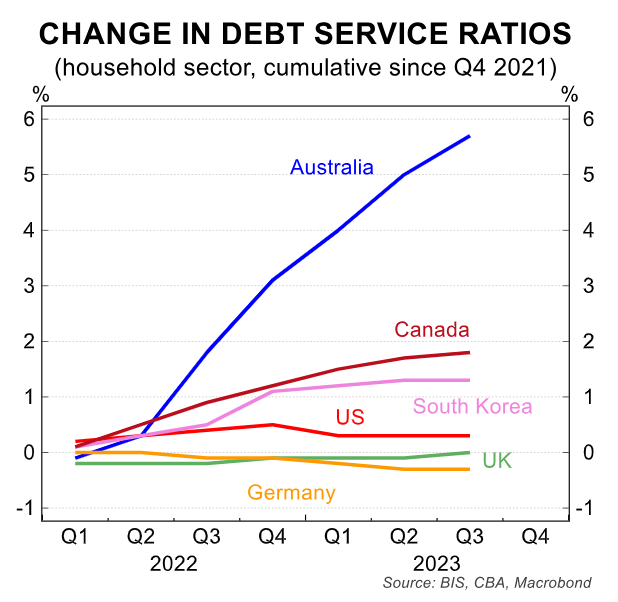

Debt servicing ratios are higher in Australia than elsewhere:

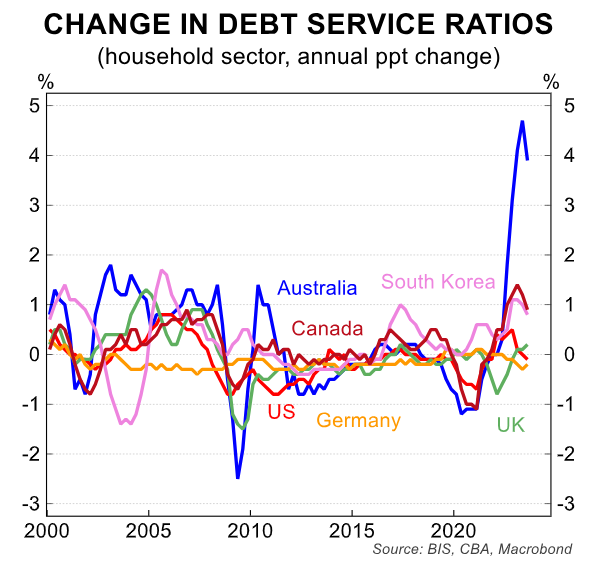

Debt servicing ratios have also risen by far more than in other nations:

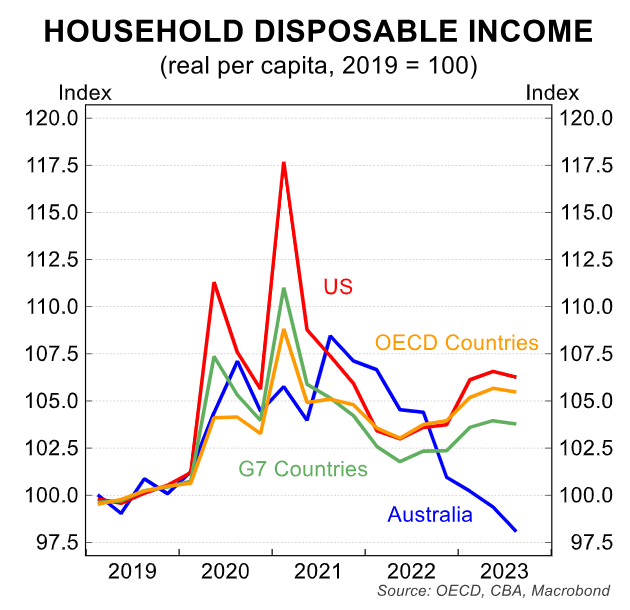

Australian household disposable income per capita has fallen by far more than other advanced nations:

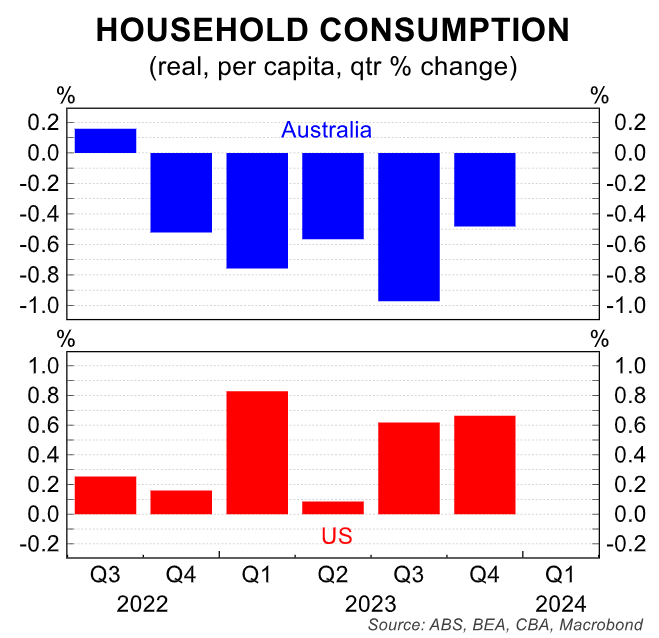

Household consumption per capita is also falling in Australia. In contrast, it is rising in the United States, where disposable incomes have surged, and there has been minimal pass-through of interest rates to borrowers:

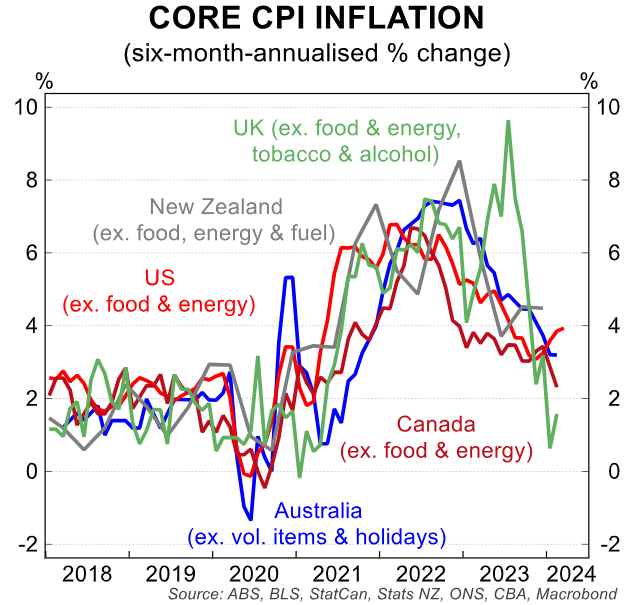

Finally, Australian core inflation is falling more or less in concert with other advanced nations:

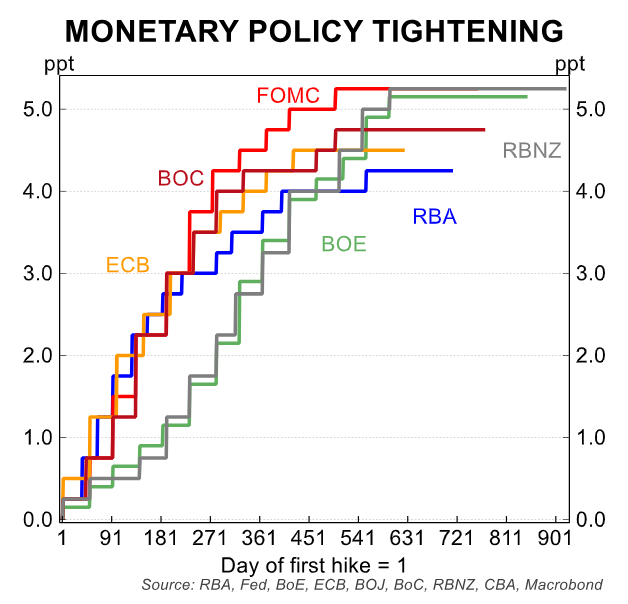

Australia’s monetary tightening is among the tightest in the world, owing to our high concentration of variable-rate mortgages and household debt.

Focusing solely on headline changes in official interest rates is asinine and misses the idiosyncratic differences between nations.