Economists have raised concern that stronger-than-expected US inflation figures could mean local prices continue to rise, delaying the path to interest rate cuts.

HSBC’s chief economist for Australia, Paul Bloxham, also warned that Australia was lagging behind the US on productivity, which would keep inflation elevated and delay rate cuts until early 2025.

“There’s another overlay and that’s the budget, we’re already getting tax cuts but the more spending there is, the more that risks supporting the economy and inflation”, he told AAP.

AMP deputy chief economist Diana Mousina has penned two reports (here and here) highlighting the key differences between Australia and the US in terms of the economy and monetary policy.

These differences mean that the RBA is likely to cut interest rates before the US Federal Reserve.

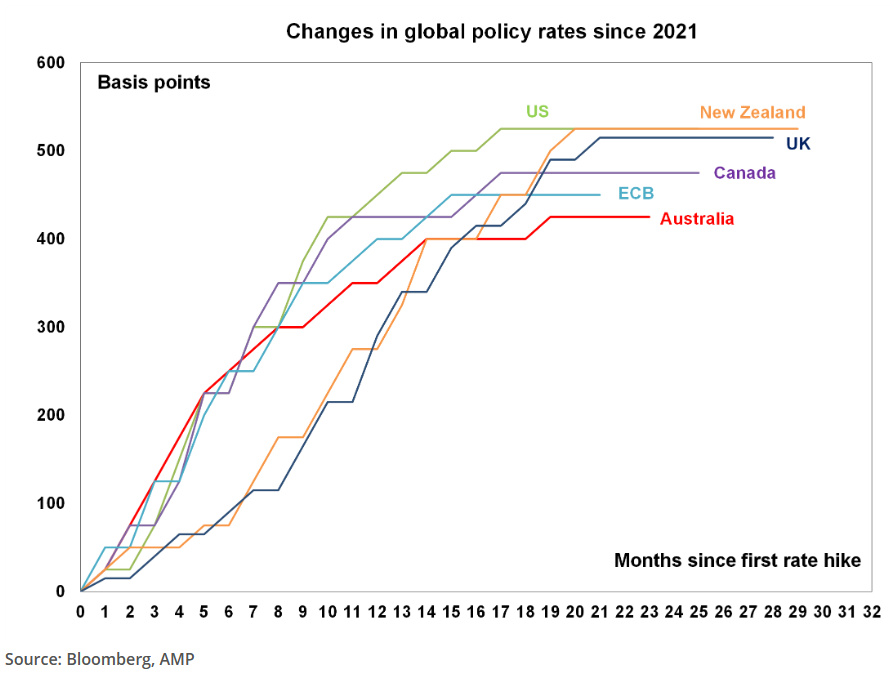

Although Australia has lagged other developed nations in lifting rates:

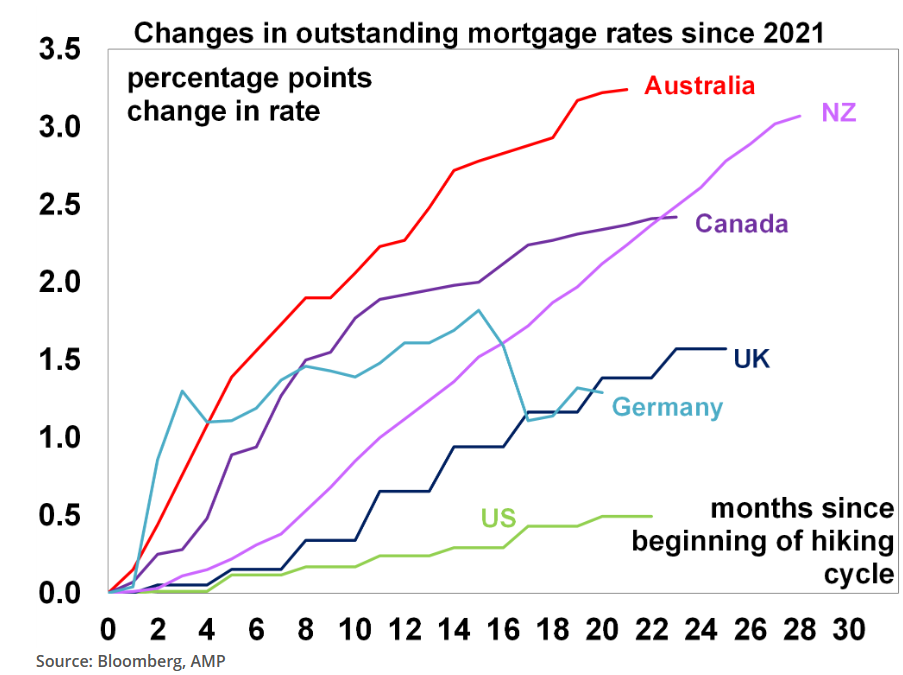

The pass through of rate rises to borrowers has been more aggressive in Australia owing to our predominance of variable rate mortgages:

“US outstanding mortgage rates have risen by 0.5 percentage points, compared to 3.2 percentage points in Australia”, notes Mousina. “This is despite Australia increasing interest rates by 1% less than the US”.

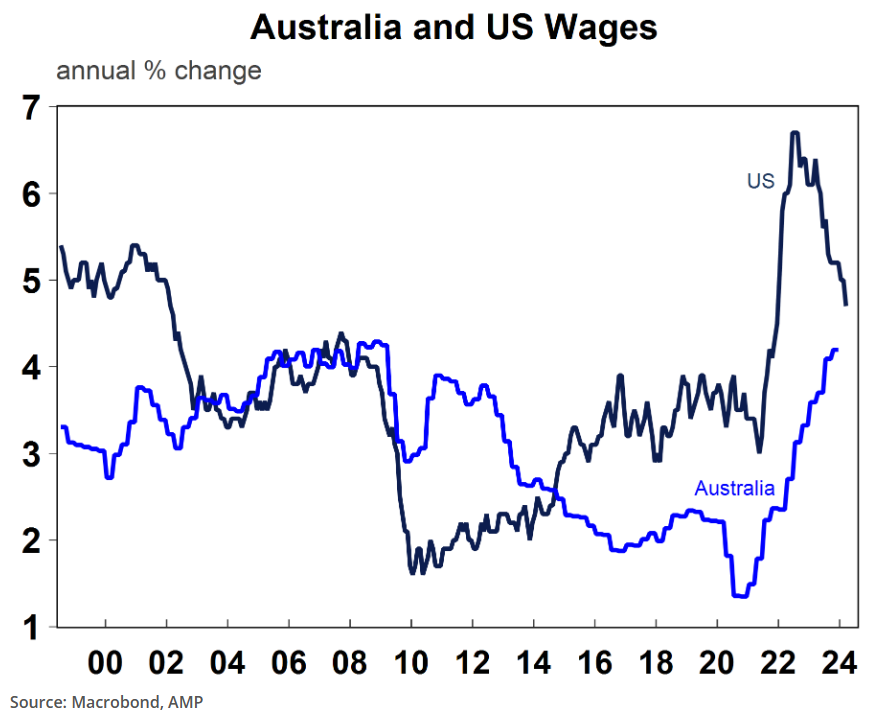

Wage growth in Australia has also lagged well behind the US:

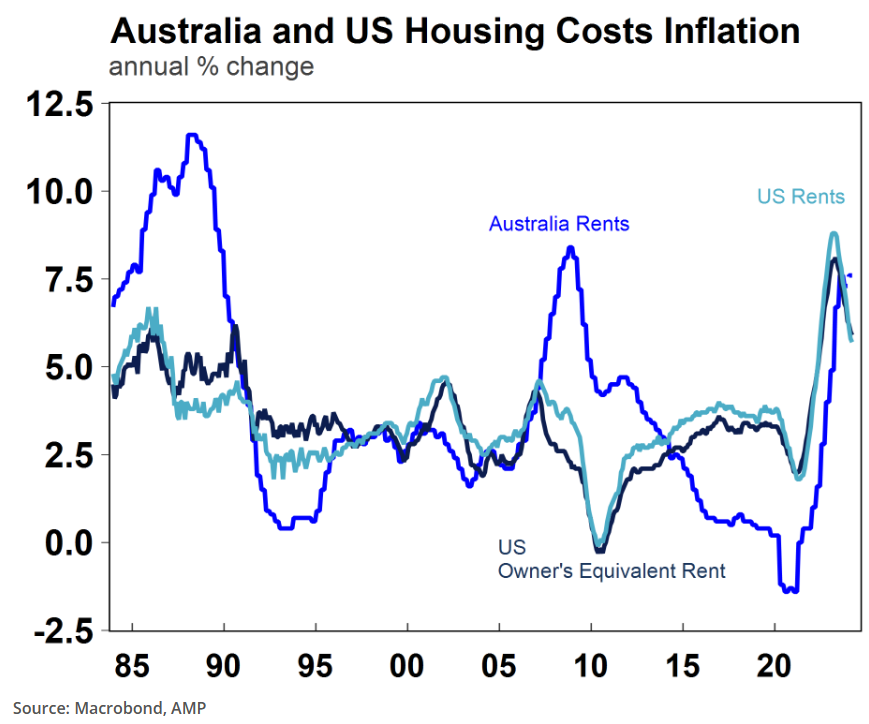

US inflation is also been driven up by shelter (rents), which comprises 33% of the US CPI basket against only 5.8% in Australia:

“Both rents and owner’s equivalent rent have had high inflation in the US (as per the previous chart)”, Mousina notes.

“If Australia had a higher weighting to rents, then services inflation would remain higher for longer, as very elevated Australian population growth is keeping rental inflation high”.

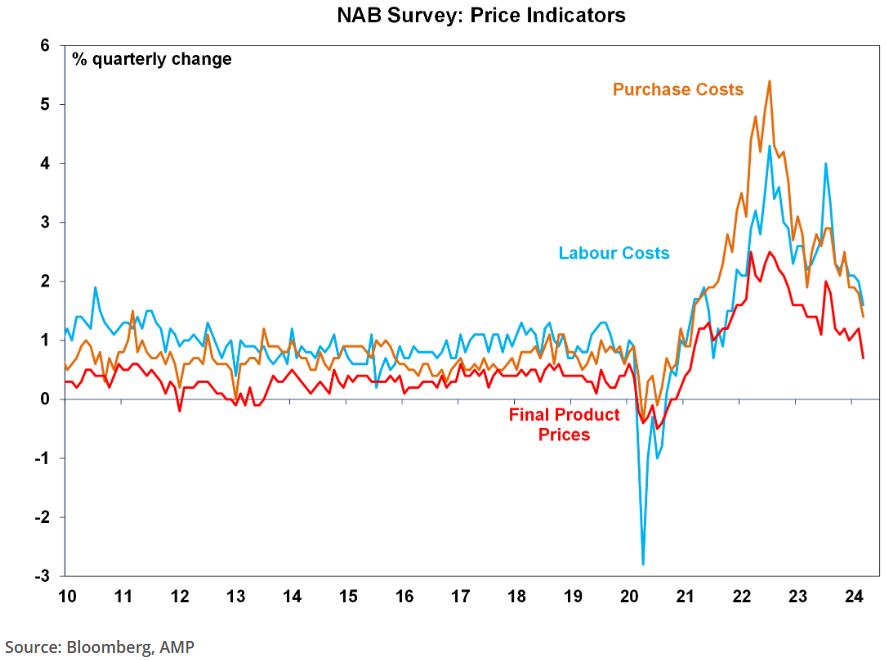

Mousina adds that US price surveys have turned up recently, whereas Australia’s have turned down:

Mousina concludes by stating “that domestic growth conditions are the primary factor behind a central bank’s decision on monetary policy”, with AMP tipping that the RBA will commence its easing cycle in Q3 this year.

CBA head of Australian economics, Gareth Aird, made similar arguments in last week’s report.

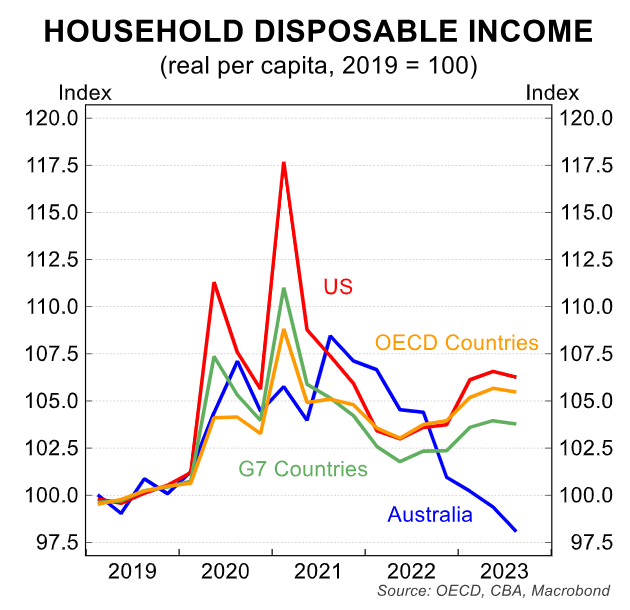

Aird added that household disposable income has fallen far more sharply in Australia than the US:

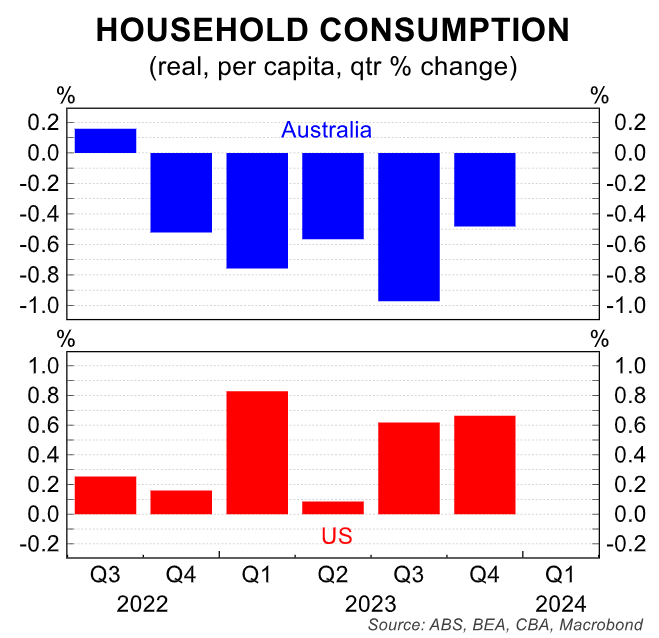

Australian households have also cut back hard on consumption, whereas US households are increasing theirs:

The above data shows that Australia has tightened monetary policy far more than most other nations, owing to our very high concentration of variable-rate mortgages and household debt.

It also shows why US inflation has very little bearing on what is happening in Australia.