Alex Joiner, chief economist at IFM Investors, has published an excellent research note on Australia’s “per capita malaise”.

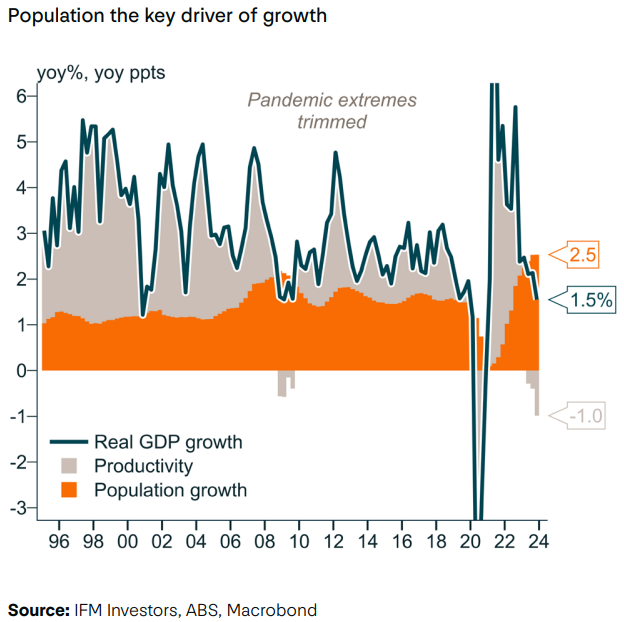

Joiner noted that “population growth is the key driver of growth and without it the economy would be in recession”.

This is evidenced by a “fourth consecutive reversal in per capita growth GDP (1.0%yoy lower)”, which is “an unusual occurrence outside a traditional headline technical recession” and “has not happened since 1982-83”.

Joiner shares our long-held view that the Reserve Bank of Australia (RBA) will commence an easing cycle in the second half. A sharper-than-anticipated increase in Australia’s unemployment rate will most likely be the driving force behind this switch to rate cuts.

Below are key extracts relating to Australia’s labour market and their implication for interest rates.

Our call on rates is being underpinned by the labour market, still very low unemployment rate and high levels of participation and employment to population that have supported the household sector through cost-of-living and interest rate pressures.

We remain watchful in this space as it is clear the labour market has loosened in the past six months, but it has not yet buckled.

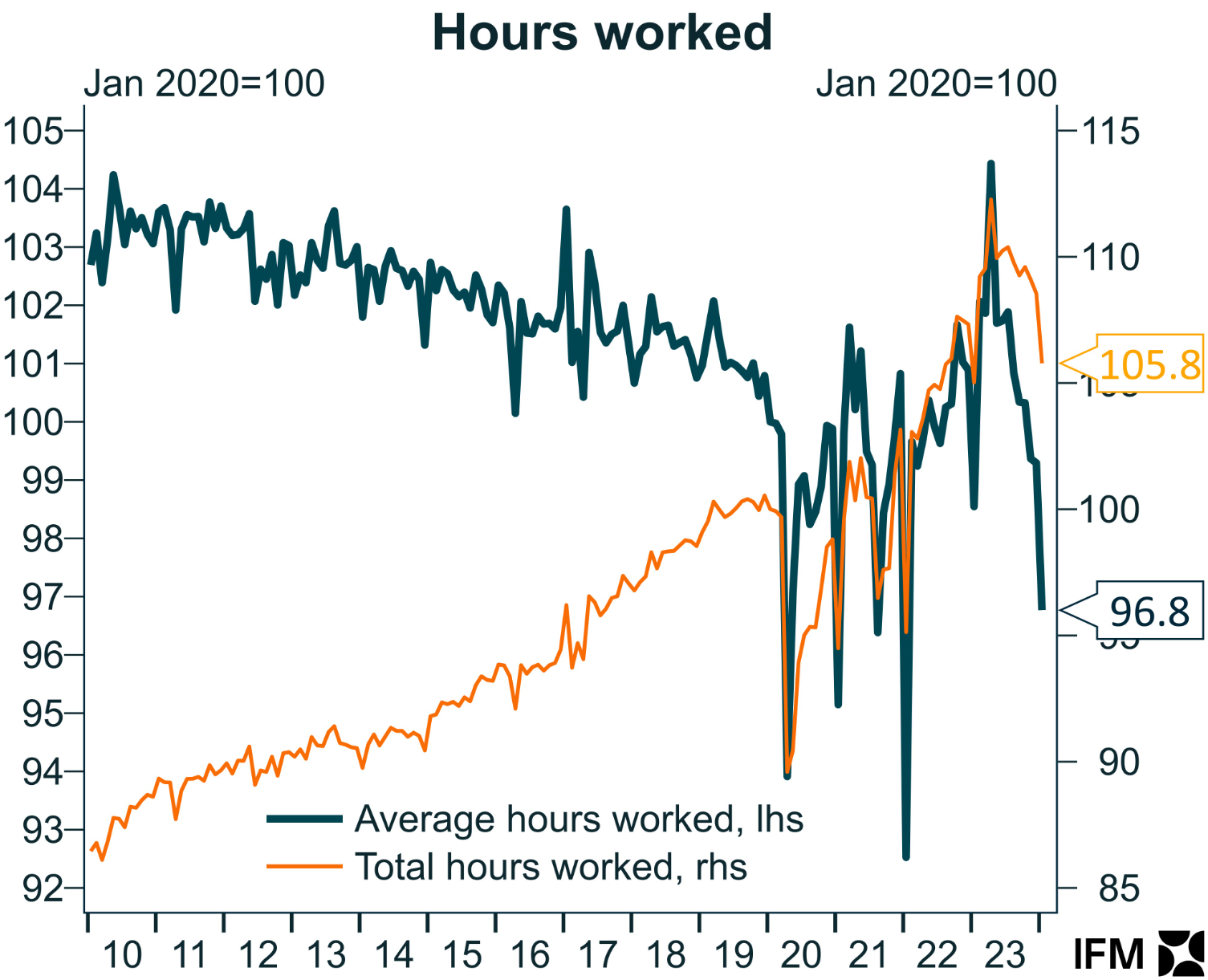

That said, the unemployment rate has ticked up to 4.1%, and hours worked have declined sharply, pushing the underutilisation rate higher to 6.6%.

A more pronounced increase in unemployment in recent months has been avoided due to a simultaneous retracement of a recent spike in the participation rate.

Of further concern is the slowdown in employment growth that sits at around 7,300 per month in trend terms while the labour force is expanding by 32,700 people (assuming constant participation).

A continuation of this trend would see a strong labour supply overwhelming weakening labour demand – pushing unemployment materially higher.

We do not have to necessarily see large outright job losses to have unemployment rise.

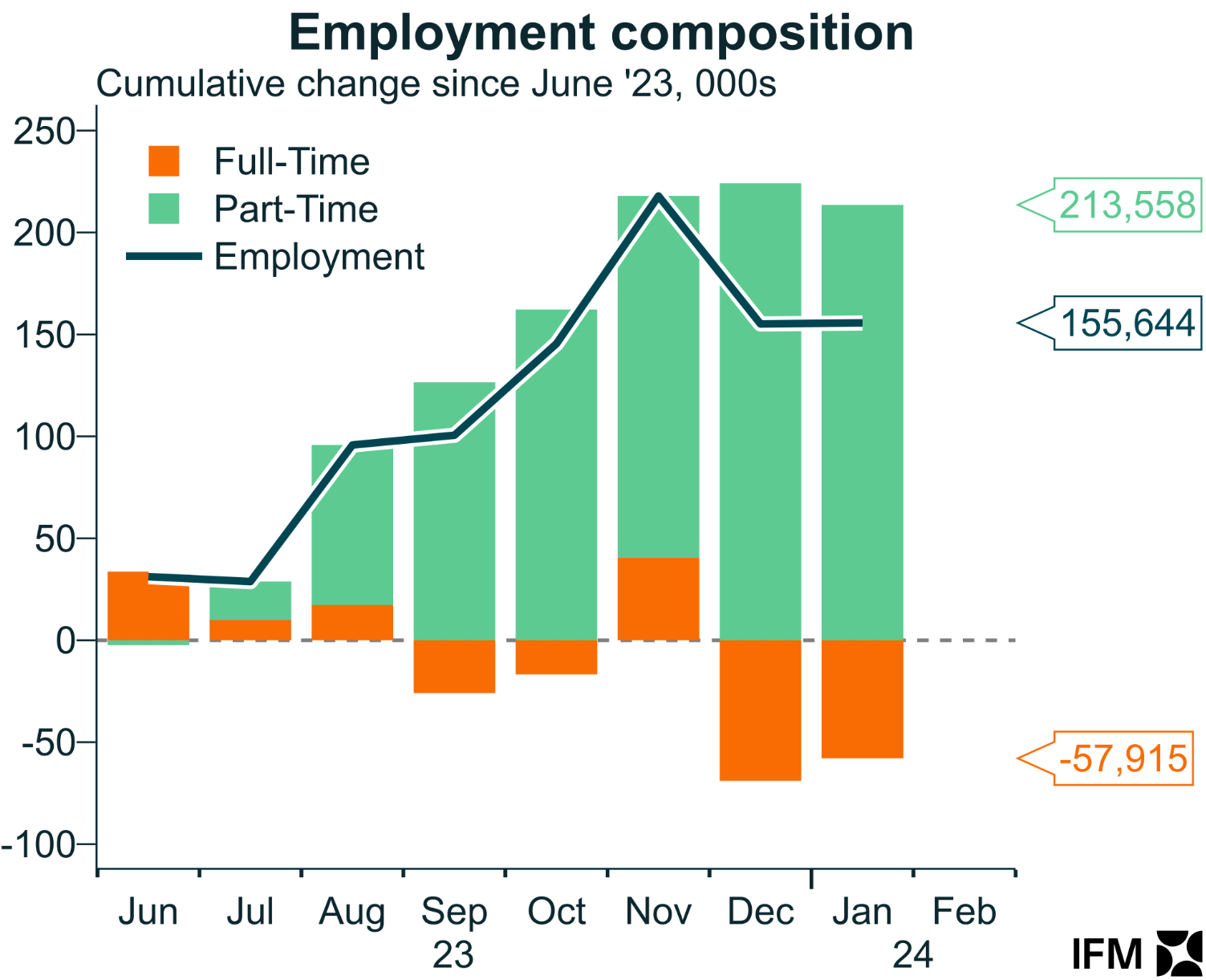

Further, the composition of this employment growth has also shifted, demonstrating business caution.

Since June 2023, 58,000 full-time job losses and 214,000 jobs have been gained – the latter being more loosely attached to the workforce.

The Statistician noted that the weakness in employment in January was due to seasonal factors delaying New Year job starts and that more people would be commencing work in February – meaning this upcoming print will be a big test.

The unemployment rate rising beyond the RBA’s expectations would be of concern, as this would likely prompt consumers to act on woeful levels of sentiment and a further pullback from retail spending.

It would be desirable to keep the labour market tight to facilitate ongoing wages growth, that was 4.2%yoy in Q4 2023.

There is clearly no threat of any wage-price spiral dynamics, and some sustained real wages growth will be needed to repair the purchasing power damaged by the inflation shock.