Westpac with the note.

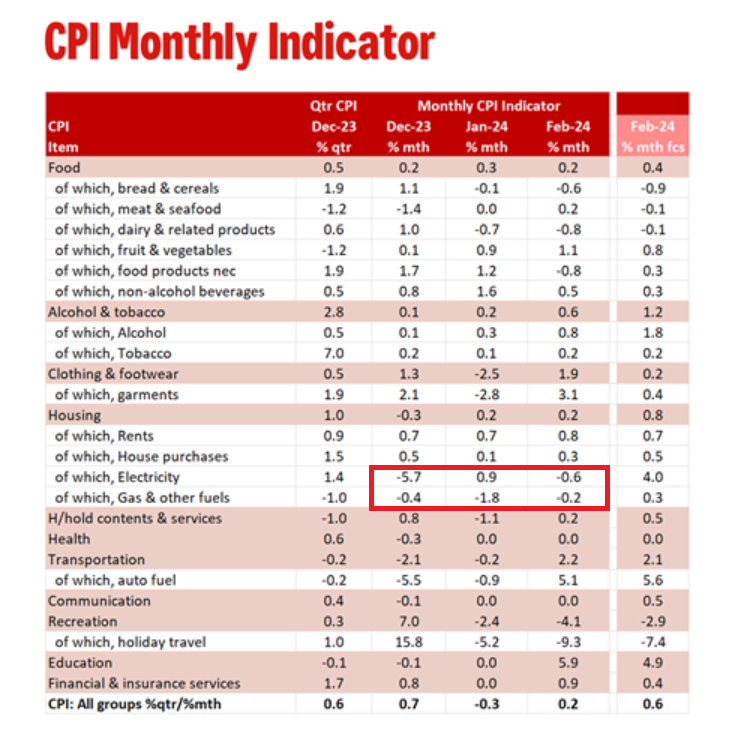

The Monthly CPI Indicator gained 3.4% in the year to February compared to 3.4%yr in both January and December.

The February print was a softer than Westpac’s forecast of 3.8% and the market median forecast of 3.5%yr. Taken at face value, the February Monthly CPI Indicator suggests that if there are any risks to our current March quarter CPI forecast of 0.7%qtr, it is to the downside.

However, the quarterly CPI is not a simple average of the Monthly CPI Indicator and history has taught us that a simple ‘face value’ estimate can be misleading.

Highlighting this are the core measures. The Trimmed Mean measure lifted to 3.9%yr from 3.8%yr while the services series jumped to 4.2%yr from 3.7%yr while goods prices continue to moderate down to 2.9%yr from 3.1%yr.

All groups excluding volatile items and holiday travel did ease back from 4.0%yr to 3.9%yr, but this is still much higher than the headline pace of 3.4%yr.

As noted in our preview, the mid-month of each quarter provides us with an important update on household services and so February sets the tone for much of this group for the quarter.

Overall, quarterly surveyed services came in stronger than expected exemplified by the 5.1%yr increase in education (forecast was 4.1%yr). This presents an upside risk to our current quarterly CPI forecast.

In the month of February, the Monthly CPI Indicator rose 0.2% compared to our forecast for 0.6% increase.

The most significant difference to our forecast was electricity, and while this series is a monthly estimate, we have now seen a run of softer than expected electricity prices due to the ongoing impact of government rebates.

February included a second round of energy rebates in Victoria. This does have a meaningful impact on our quarterly electricity forecast and presents a downside risk to our Q1 CPI forecast.

Weaker than expected electricity and holiday travel (both monthly series) are being offset by the stronger than expected services (which are quarterly surveys so now locked in for Q1).

While we have more work to do on our quarterly forecast, at this stage we find the risk to our Q1 estimate of 0.7% is balanced.

I don’t disagree with the ongoing energy bill subsidies (which are really profit boosters for the energy cartels) for the sole reason that the Australian people don’t deserve to pay for the Albanese Government’s failure to reform energy markets.

However, this is a form of public fraud because the public will eventually pay anyway via the tax system, given that the subsidies will eventually be recouped via higher taxes.

The subsidies should only be used short term while inflation comes down.

The subsidies should then be cut with energy market reforms to genuinely and permanently lower bills.

What odds do we put on Chicken Chalmers doing that?

The same applies to rental subsidies through the Commonwealth Rental Assistance Scheme (CRAS), which is designed to cover up Labor’s mass immigration policy.

CPI rents are 7.6% higher over the year (but a higher 9.3% when excluding rent assistance impact).