Independent economist Tony Alexander believes that the Reserve Bank of New Zealand definitely will not hike into a recession.

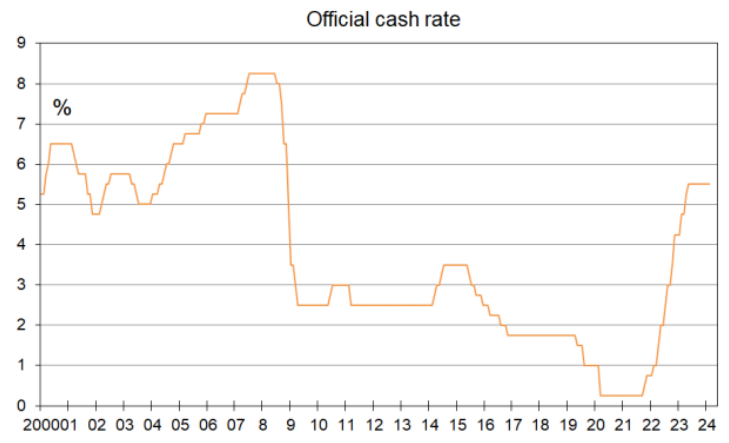

As a result, New Zealand’s official cash rate (OCR) will not rise from its current level of 5.50%.

The key event needing to be commented on this week was yesterday’s review of the economy, inflation, and monetary policy by the Reserve Bank.

About three weeks ago after the ever-so slightly stronger than expected out of date employment data, one forecasting group changed their view to predicting further interest rate rises.

No other forecasters adopted their bearish stance for a variety of reasons. Here are a few of them.

Although inflation is too high at 4.7% and business pricing plans nowhere near where they need to be, monetary policy acts with a lag commonly accepted as being around 18-24 months.

That is, from the time monetary policy gets tightened it takes up to two years for the strongest part of the impact on inflation to be felt. So, when did monetary policy get tightened?

The first cash rate increase came in October 2021. But it was only a 0.25% rise and the more hefty 0.5% rises did not commence until less than two years ago in April 2022.

The peak period of tightening was late in 2022 when the cash rate was pushed up 0.75% in October and the Reserve Bank warned of recession.

So, counting that time as when the monetary policy tightening really hit the fan, we are not even a year and a half into the period when the greatest downward pressure on inflation can reasonably be expected to manifest itself.

Calling for extra monetary policy tightening now reflects an impatience akin to the kids screaming “Are we there yet” in the back of the family car on a road trip.

Our central bank eased monetary policy far too much over 2020 and generated the strong inflation above 7% which we saw.

They then tightened too slowly over 2021 and 2022 in a manner which we saw previously over 2004-07.

The last thing they’ll want to do now is aggravate their earlier failings by tightening too much.

The second reason for people like myself doubting that policy needs tightening again this late in the cycle has been that the economy is already being shattered by rate rises to date.

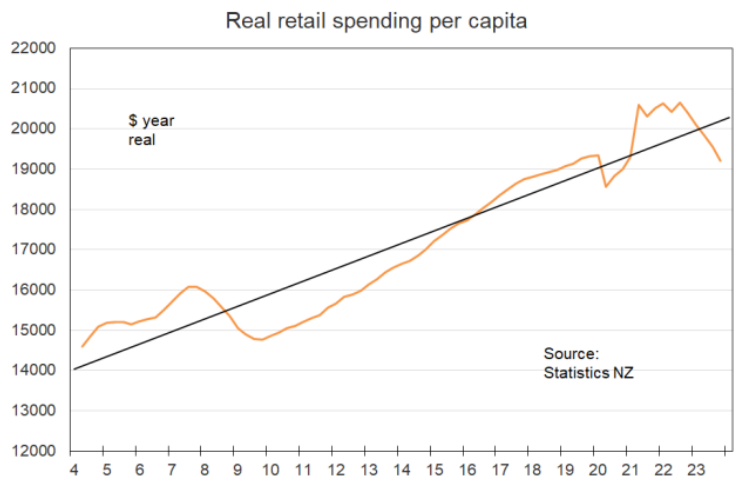

Retail spending volumes per capita at the end of last year were 7% down from the end of 2022 and 11% down from the end of 2021.

That is the very definition of a household spending crunch traditionally sought by a central bank when applying disinflationary pressure to an economy.

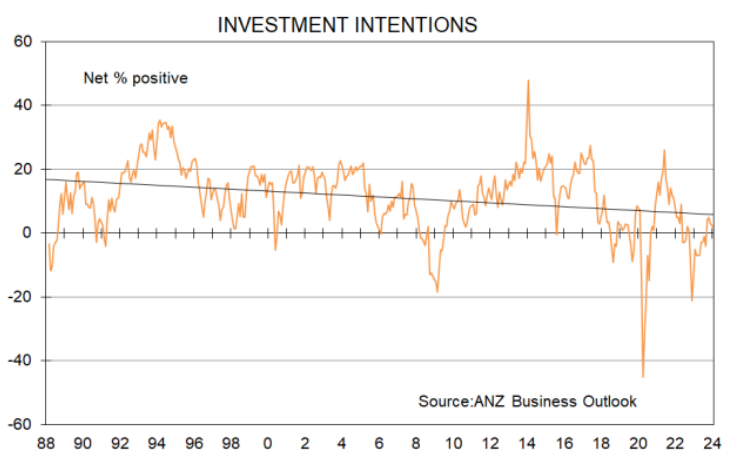

Business capital expenditure plans are running at well below average levels.

Exports are running 7% down from a year ago and the outlook for growth in our biggest goods buyer – China – is not good.

On top of that fiscal policy is being tightened by the new government having to address what every modern government has had to do when Labour are voted out – get the fiscal accounts back into order.

Ultimately the previous Finance Minister did exactly what we warned he would do from 2017 – leave a fiscal mess.

Furthermore, house building is falling sharply, property developers are becoming increasingly desperate to drum up business (you should see the developer speaking request I just received and turned down and the media they wanted to run with it to drum up business).

The chances are firm that the number of consents being issued for new dwellings to be constructed will this year fall below the 32,000 recently predicted by MBIE and which I thought at the time looked like a reasonable number.

The recent new worries about interest rates and failure of the residential real estate market to continue with its June quarter surge have put the kybosh on hopes for a cyclical recovery in house building come early-2025. Late in the year is now more likely.

Add in the fact discussed here that the quarterly employment numbers in New Zealand have a history of looking weird (meaning monthly numbers aren’t worth paying any attention to), and the case for extra tightening of monetary policy now was never strong.

And so it has turned out to be – though the Reserve Bank has rightly warned that there is still a lot of water to go under the bridge with regard to cementing inflation and inflation expectations solidly back in the 1% – 3% range.

At their review on Wednesday, the Reserve Bank left the official cash rate unchanged at 5.5%. They warned of inflation risk from geopolitical and shipping problems offshore and said that for now there is no scope to ease policy.

But they also made other comments which indicate that they are marginally less worried about inflation than at their last review in November.

First, in the material discussing what the policy committee talked about there was no mention that they discussed raising the cash rate.

Second, the projected a less strong growth profile for the NZ economy over the first half of this year while keeping most other forecasts little changed for time periods further out.

Third, they reduced the numbers pencilled in for where the cash rate peaks from 5.7% to 5.6%. The change is probably a technical rounding thing. But the important point which they would have been aware of is the signalling effect.

Fourth, they explicitly discussed growth risks facing China. This is important because China accounts for about one-third of New Zealand’s export earnings and those earnings are falling already.

Fifth, they repeated that they are still using old numbers from Treasury regarding fiscal policy and have yet to factor in the new government’s policies. Those policies look like a tightening even allowing for mid-year tax cuts therefore there is some extra disinflationary pressure which they will factor in after the Budget due on May 30.

Sixth, they noted this in their commentary:

“Members noted that overall, risks to the outlook for inflation were more balanced than at the time of the November 2023 Statement”.

As a result of their slightly more dovish than expected review, we have seen wholesale interest rates fall away. So far, they have given up near half of the rises which occurred three weeks ago when one forecasting group said that a tightening was on the way.

Is the change great enough to alter the outlook for our economy, mortgage rates, and the housing market in the near future? No.

The level of uncertainty about everything is just as bad now as it was a month ago and all that has happened is that more extreme bearish views have been stripped away.