Independent economist Tony Alexander has released his latest survey of real estate agents, which shows that New Zealand’s nascent housing rebound has well and truly stalled.

This should comfort the Reserve Bank and, alongside the stalling economy, provide further indication that the official cash rate could be cut later this year.

Housing upturn stalls for now

The upturn in the market has for now petered out and here are numbers showing it.

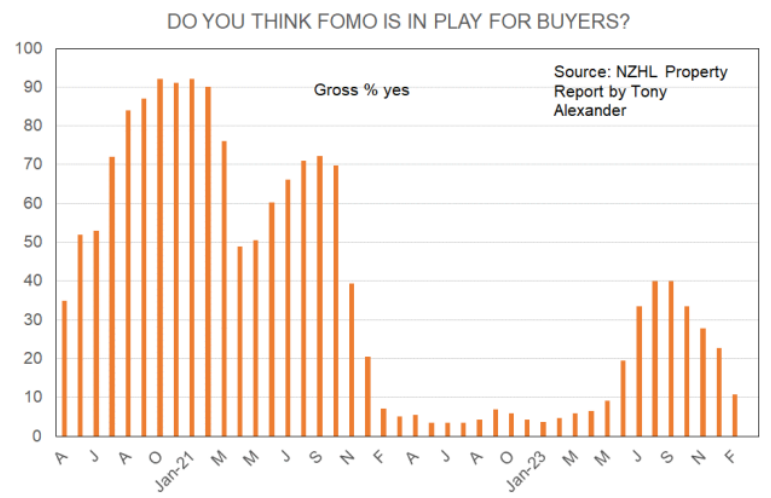

Let’s start with FOMO. During the pandemic frenzy from August 2020 to February 2021 the gross proportion of real estate agents saying that buyers were displaying FOMO averaged 89% with a peak of 92% in October and January.

The reading fell to 51% in May 2021 after the investor tax changes and return of LVRs, recovered to 72% in September 2021 as listings fell to record lows, then oscillated between only 4% and 9% from February 2022 through to May 2023.

FOMO then lifted to a reasonably healthy 40% over August and September last year before falling to 23% at the end of January. It has now decreased to 11%.

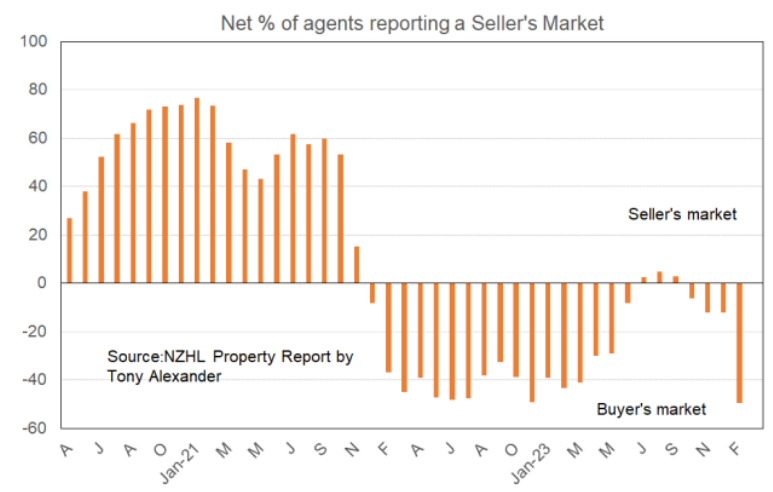

Buyers no longer feel that they need to pull finger and get a deal done and this has resulted in my measure of the extent to which a buyer’s market is in place (meaning sellers are seen as most motivated to get a deal done) going back to November 2022 levels.

We are solidly in a buyer’s market again and the graph is fairly stark.

I can see this backing away of buyers in other measures including a large decline in the net proportion of agents seeing more investors, presence of people at open homes, and presence of people at auctions. I will show those results and graphs in the release with NZHL in a few days time.

Suffice to say, the graphs show changes akin to the one above for seller’s market.

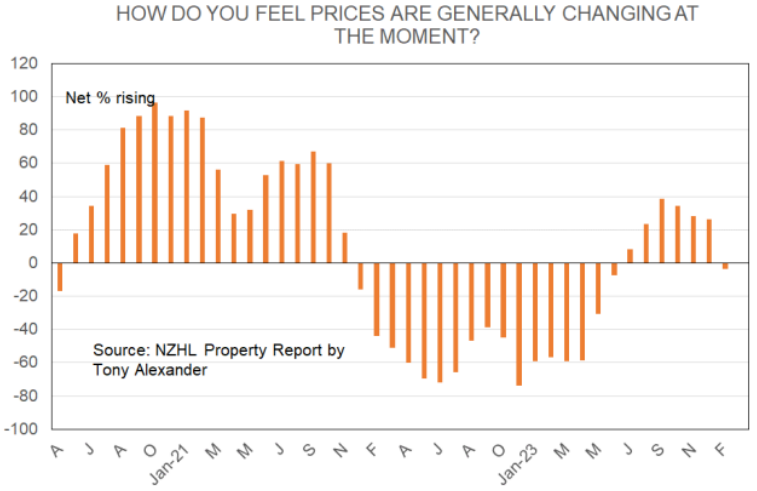

Price momentum for now has stalled with a net 3% of agents now saying that prices are falling in their location. This measure recently peaked at a net 38% seeing prices rising back in September.

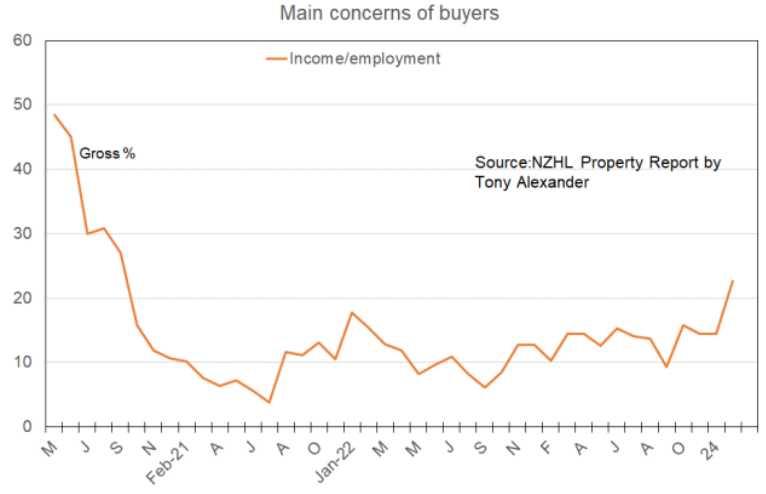

I ask the agents about the things buyers are most concerned about. I can see from their responses that there is a new lift in worries about employment. As an economist what I want to say here is this – it’s about time.

The labour market is a lagging indicator of what the economy is doing – going up after the pace of growth in the economy has lifted, and going down some time after the pace of GDP growth has slowed.

A key source of inflation in New Zealand has been the very high pace of wages growth in recent years. The Reserve Bank needs this growth to slow down a lot in order to be comfortable that the inflation genie is back in the bottle.

But the latest reading is of private sector wages growth above 6.5% compared with the three decade average consistent with near 2% inflation of 3.3%.

The fact that people are now getting concerned about their employment is a negative for the housing market which I always expected to act as a minor counter-balance to other stimulatory house price factors through 2024.

But it is positive for interest rates easing and when we get better data showing the labour market easing off the interest rates response will be interesting.

Speaking of which, this is the second area where buyers have become newly concerned about things and I think the recent errant prediction by one forecasting group of additional monetary policy tightening has played a role in scaring the bejeebers out of people already feeling so much financial strain they have cut their per capita spending volume 11% from two years ago.

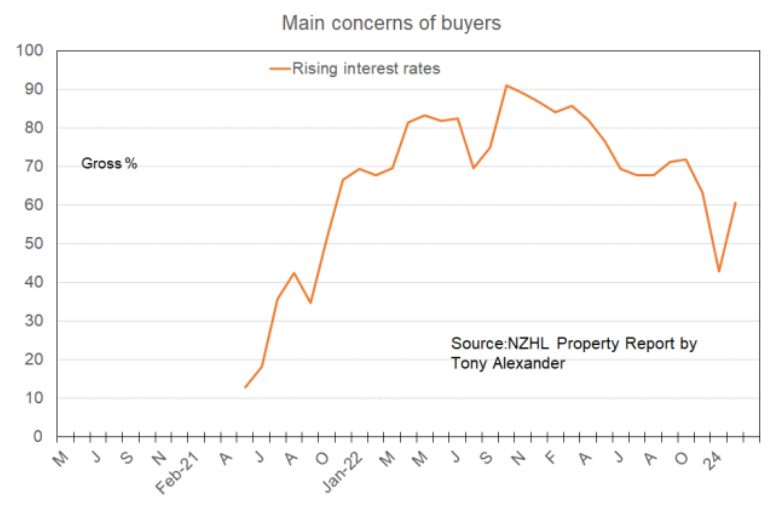

The gross proportion of agents saying that buyers are worried about interest rates has just gone up to 61% from 43% in January. The trend is still done but the optimism of people has been dealt an unnecessary blow.

As I said to a journalist last week and was written at the end of his Sunday article about economists – with great power comes great responsibility. And spiders.

The third factor in play is perhaps the biggest one accounting for buyers stepping back with a feeling that time is still on their side and there is no need to hurry. A listings surge.

A key point I started making over a year ago was that the upturn in the housing market would be assisted by the activation of a queue of buyers sitting on their hands from late-2021. That queue I believe was getting activated in the middle of last year.

But what has also happened is that the queue of sellers building up since back then has also become activated and they have decided to take advantage of the upturn in the housing market to place their property on the market.

I have two sets of data showing this. First, we have the numbers from realestate.co.nz showing that at the end of February the number of properties listed with them was at an eight year high of 28,800.

This was well up from 24,700 at the end of July last year and above the previous recent peak of 28,500 at the end of 2022. In mid-2021, the number was 13,500.

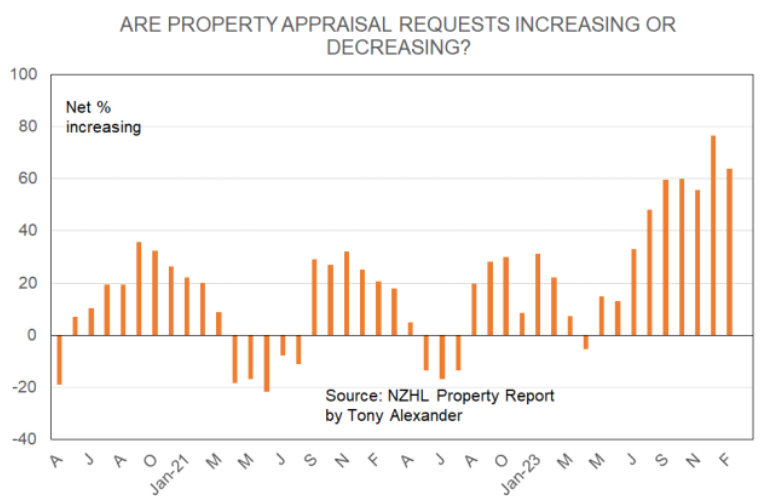

In seasonally adjusted terms the number of fresh property listings they received rose by over 20% in both January and February. Reflecting this the net proportion of real estate agents in my survey saying that they are receiving more requests for property appraisals has climbed over recent months to sit at 64% this month and a record 76% last month from a net 5% in April last year receiving fewer appraisal requests.

In a nutshell, the activation of the queue of frustrated sellers built up since the end of 2021 has been stronger than the activation of the queue of buyers.

And so, when will this situation reverse? I feel not until we get much greater certainty about interest rates going down. The Reserve Bank last week did not validate the incorrect forecast that they would tighten again, and their comments were slightly softer than anticipated.

They still say they don’t plan cutting the official cash rate from 5.5% until the middle of next year. But the markets are pricing in cuts starting in October and I think that is reasonable.

After the first cut I see a good chance of some rapid rate declines because of my view that just as the Reserve Bank over-stimulated our economy during the pandemic they have now over-restrained it during the post-pandemic inflation fight.

They have unfortunately become a source of instability in our economy as their focus has shifted from pure economic analysis to touchy-feely drivel.

Many of us have developed a view over the past couple of months that the upturn in the market has been softened and shifted out 6-9 months.

Firm interest rate declines over 2025 and perhaps even by the very end of this year will then act in concert with other developments such as strong population growth, tax changes, relaxed LVRs, CCCFA tweaking, and construction falling to firmly accelerate the pace of house price growth through 2025-26.

It is on house construction that I want to finish this week. Prospects for builders have just worsened and the shortage of property when it comes will be greater. Why? Because the need which buyers feel to buy something not yet built has been dealt a blow by new uncertainty about what interest rates are going to do courtesy of the errant forecasters, and because listings of houses already in existence have surged.

The number of consents issued for the construction of new dwellings has fallen from the record 51,000 in the year to May 2022 to 36,500.

This is still 29% above the 20 year average of 28,300. But there is now a growing chance we sink back to that average rather than having the decline this year be only to the near 32,000 predicted by MBIE in their post-election minister briefing.

More failures of construction-related businesses will occur this year and unfortunately the reporting of these failures will make buyers even more cautious about buying off the plan.

Things are likely to feed downward on themselves through to the second half of 2025 when cyclical recovery in residential construction looks likely on the basis of (by then) rapidly rising prices for houses, falling listings, much higher FOMO, and still firm population growth.