This Goldman analysis does not cover Australia, but its point does:

Global labor markets remain healthy, and low unemployment rates are one reason why DM central banks have remained patient on rate cuts.

We forecast that unemployment rates will not meaningfully rise in 2024, and that most major DM central banks will remain on hold until June, at which point inflation progress will justify the start of rate cut cycles.

But with labor markets largely rebalanced, even a modest increase in the unemployment rate would likely to prompt a monetary policy response.

After all, an unexpected rise in the unemployment rate has historically been the single strongest predictor of policy easing.

To quantify the risk that unexpected unemployment rate increases prompt earlier rate cuts, we estimate how much of an increase in unemployment would shift the market to fully price consecutive 25bp cuts at each meeting for the rest of 2024 (assuming cutting cycles start in June and other relevant indicators evolve as expected).

Across the DM central banks, we estimate that an incremental increase in the unemployment rate of 0.2-0.3pp would be sufficient to justify fully pricing three consecutive cuts, and an incremental increase of 0.3-0.6pp would justify pricing five consecutive cuts through year-end.

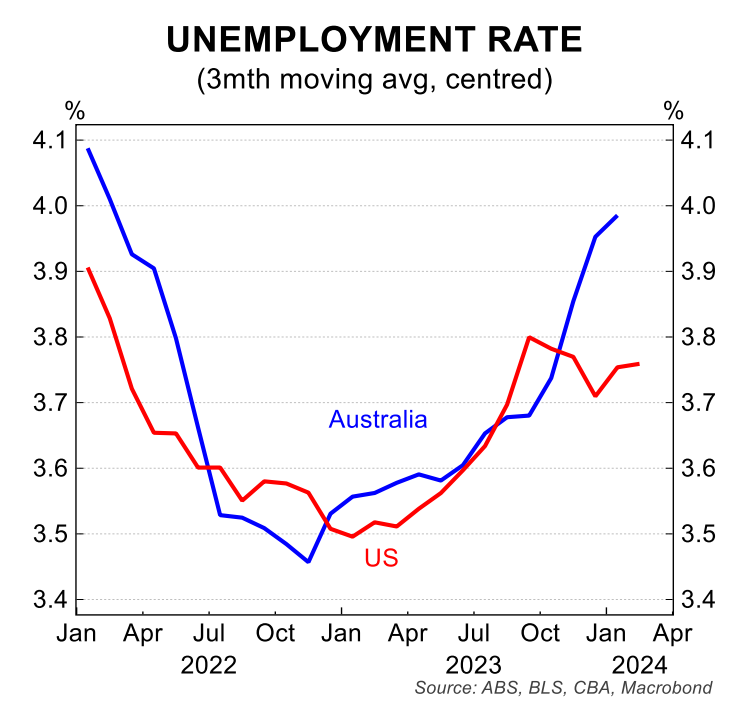

The Australian unemployment rate is already surging ahead of other DMs:

And the outlook is worse by the day:

The UE rate is already well ahead of the RBA outlook. It is going to get very far ahead in short order.

The longer it waits, the harder the pivot will be.