Westpac chief economist, Luci Ellis, told The AFR that Australia’s economy may have contracted in the December quarter despite historically high net overseas migration.

While Westpac expects that the economy grew by 0.2% in the three months to December, Ellis said that she “couldn’t rule out the initial [GDP growth] print being negative”.

A negative GDP print would represent the Australian economy’s first quarterly contraction since the September quarter of 2021, and the fourth consecutive decline in the pace of quarterly growth.

“Everything we’ve seen – hours worked is soft, trade is soft, the indications on investment are a bit soft, and now today’s dwelling investment numbers are a bit soft”, Ellis said on Wednesday.

The RBA Statement of Monetary Policy forecast real GDP growth of 1.5% in the 2023 calendar year, which implies a quarterly outcome of 0.3%.

Therefore, a negative or flat GDP print would represent a significant downgrade from the RBA’s expectations and strengthen the case for rate cuts.

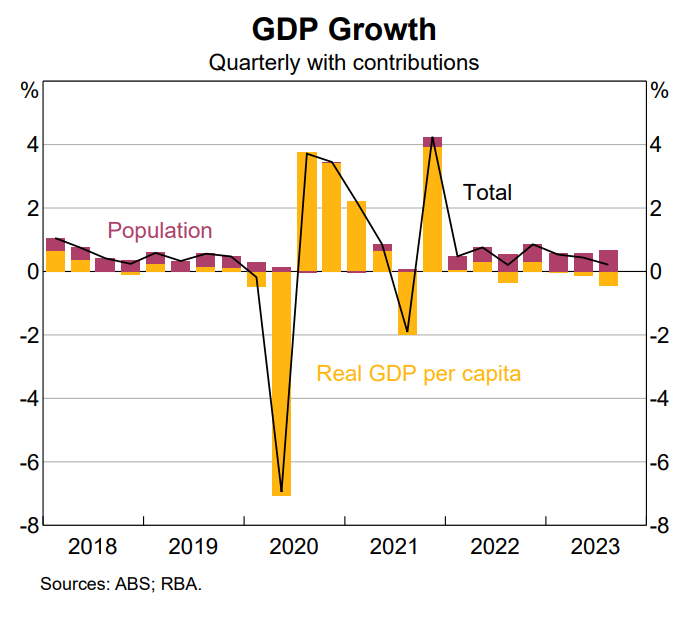

Irrespective, Australia’s population is likely to have grown by 0.5-0.6% in Q4. This means that a continuation of the per capita recession, which has already run for three consecutive quarters, is guaranteed.

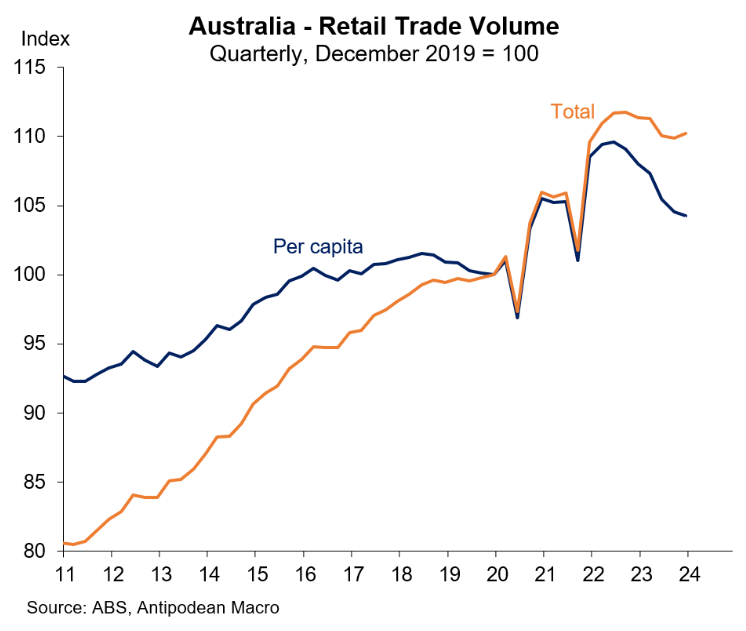

This aligns with the sharp fall in per capita retail sales volumes in 2023, as well as a range of other indicators:

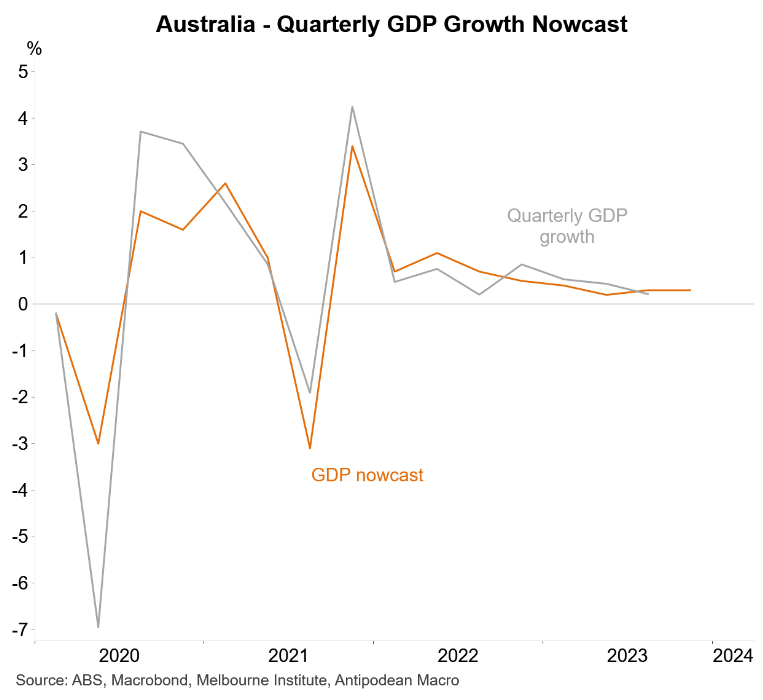

Interestingly, the Melbourne Institute’s latest nowcast of Q4 GDP growth remained at +0.3% q/q, according to Justin Fabo at Antipodean Macro, which is dead in line with the RBA’s forecast:

The bottom line is that next week’s ABS national accounts are likely to record anaemic aggregate GDP growth for Q4 and a continuation of Australia’s per capita recession.

Australia’s economic pie will continue to grow due to rapid population growth, but everyone’s share of the economic pie will continue to shrink, alongside living standards.