I never trade on unemployment reports. They are a craps shoot. Trend is what matters.

Westpac with the update.

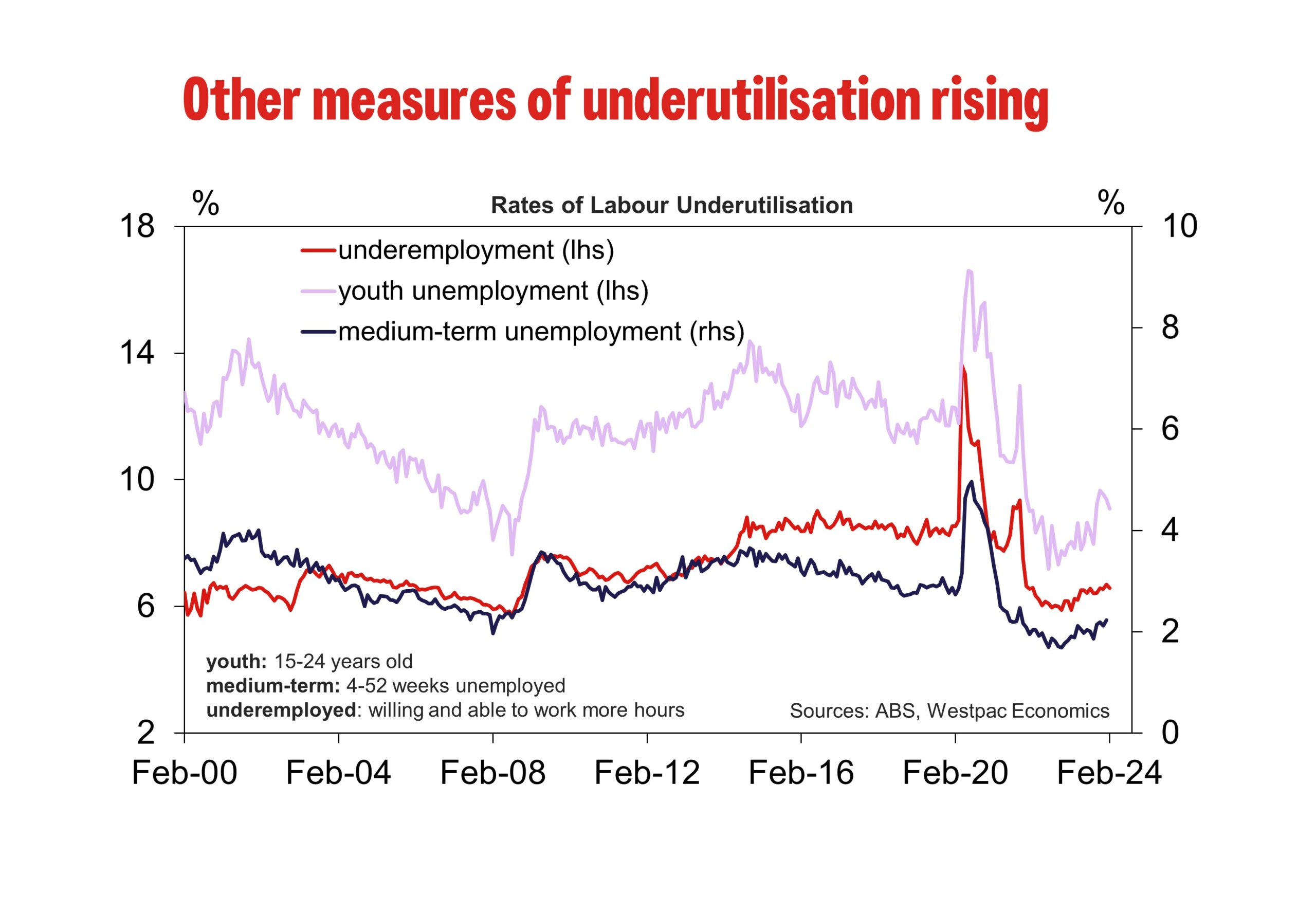

Overall, the February survey presented another murky read on the state of the labour market. Shifting seasonal dynamics continue to have a significant influence, making it difficult to gain a clear read on underlying conditions in the labour market.

On balance, the latest update does not materially shift our view.

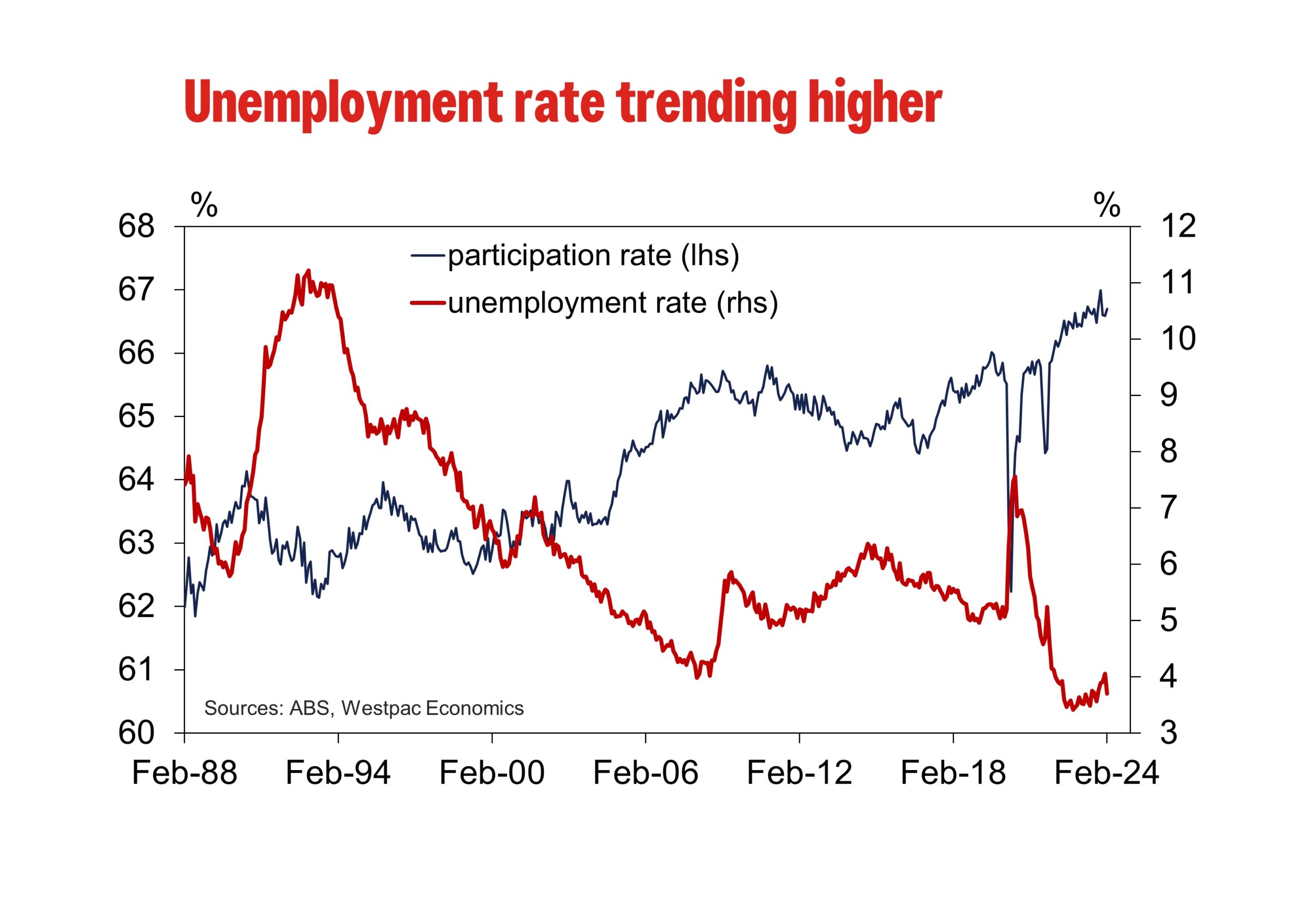

As the slowdown in activity perseveres and broadens across the domestic economy, conditions in the labour market are softening.

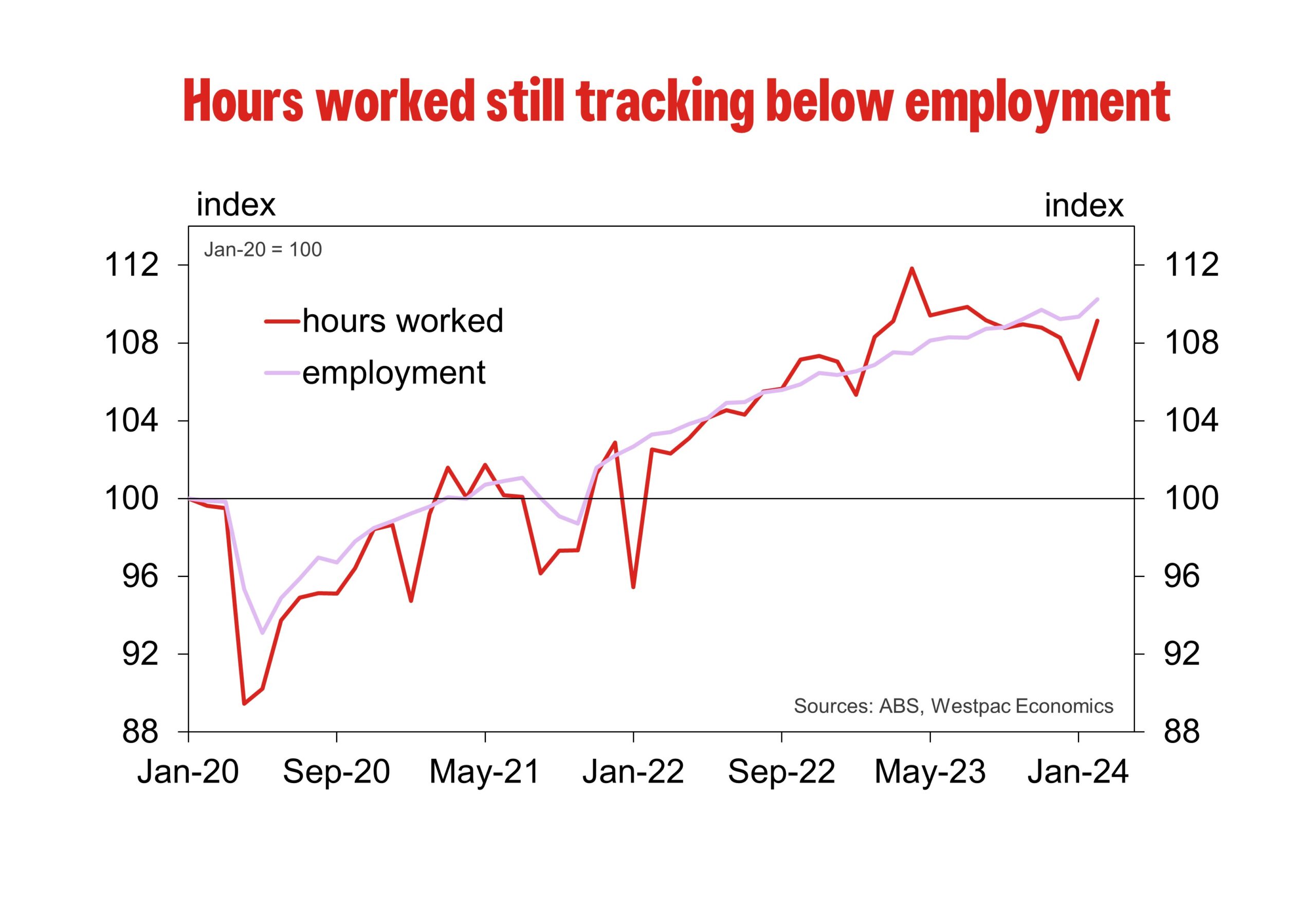

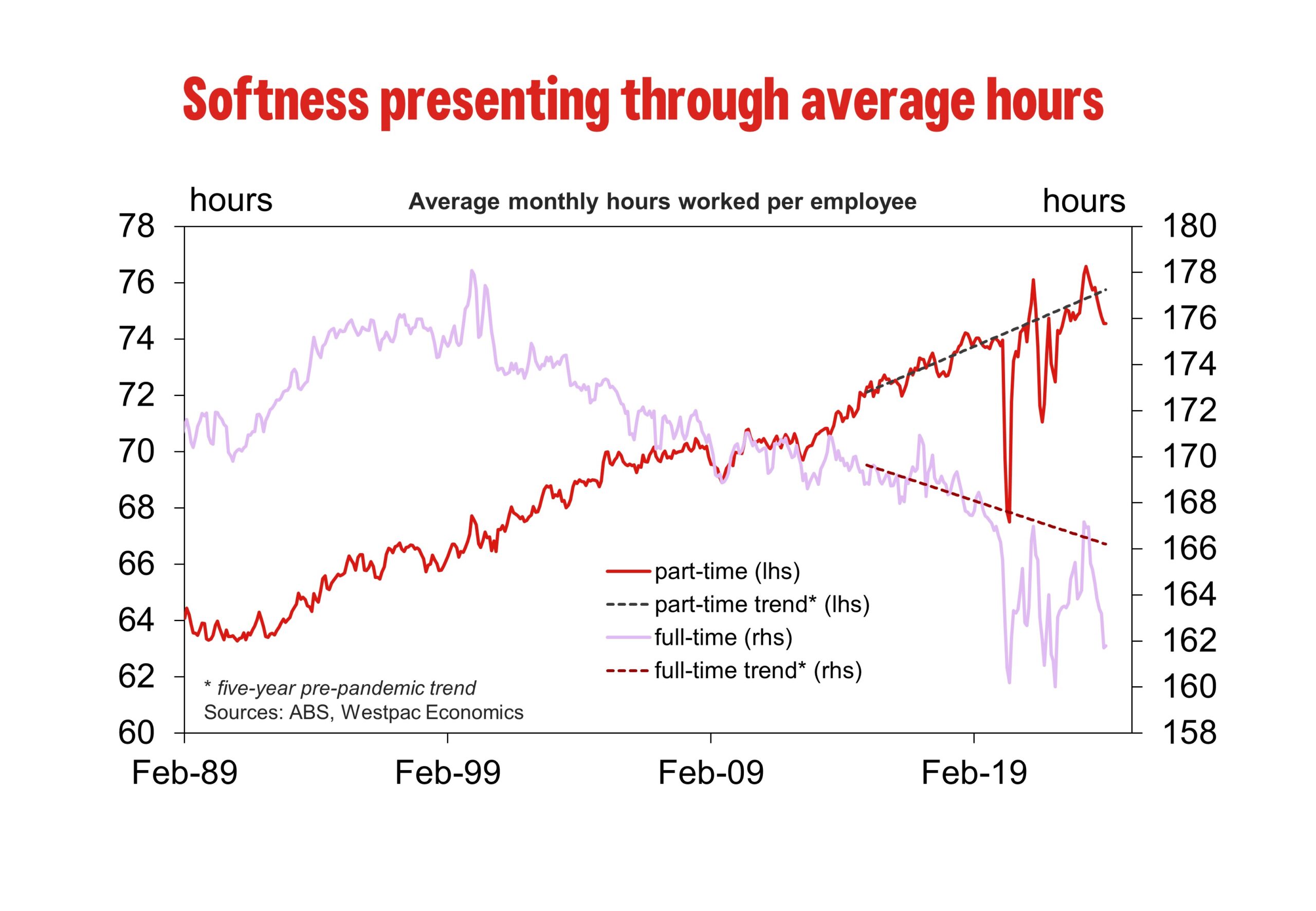

Demand for labour is moderating and is not expected to keep up with growth in labour supply, seeing the unemployment rate over the course of this year. Employers that are seeking to adjust labour usage are predominately doing so by reducing average hours worked.

At this stage, it looks as though there is further scope for this to run into mid-year.

Growth in employment will continue to slow within this context, but a transition into material economy-wide declines in employment seems unlikely at this stage.

The RBA continues to assess labour market conditions as “tighter than is consistent with sustained full employment and inflation at target”.

More updates on the state of the labour market will be necessary before any material adjustment to that assessment occurs, especially given the extreme volatility within these figures over recent months.

Murky, indeed. But this is typical of the labour force expansion growth model.

It creates oodles of jobs, mostly slave labour and low-level bullshit, as the economy is disautomated and capital shallows.

What is rarely mentioned is that Albo’s Indian army steps off the plane and into an Uber, so it is both difficult to survey and not, strictly speaking, unemployed.

Even so, the number of applicants for better positions skyrockets:

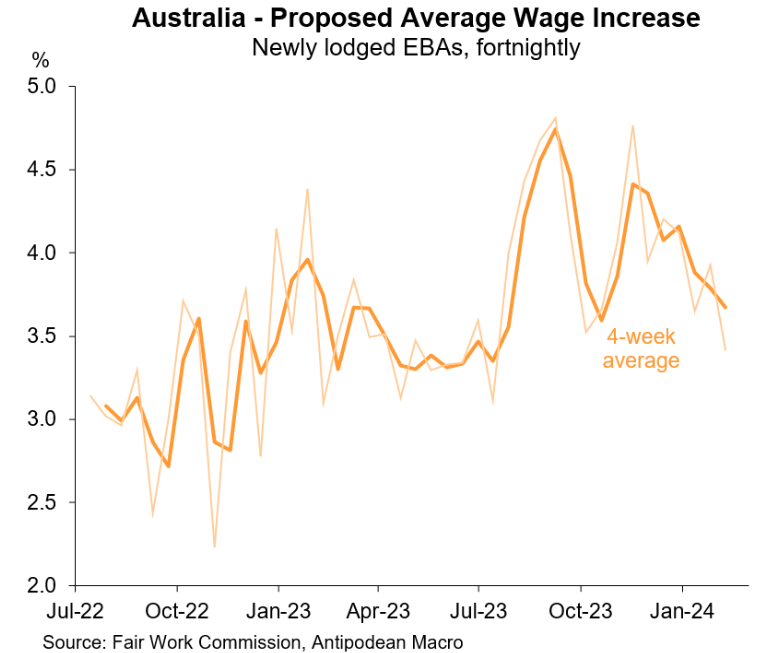

And wages are belted:

In the last business cycle, the RBA refused to see these new dynamics and kept monetary policy too tight.

There is little to suggest that they have seen the light, and ABS numberwang does not help.